Marcus — 38, software architect at Google, pulls down $180,000 a year — called me last Tuesday in a panic. His voice cracked when he told me his savings account had $847 in it.

This wasn’t some gambling addiction or medical emergency story. Marcus is methodical about everything. He reads financial blogs. He listens to podcasts. He even built a spreadsheet that tracks his expenses down to the penny.

Yet somehow, despite earning more than 92% of Americans, he was living paycheck to paycheck.

“I don’t understand it,” he said. “I make smart decisions. I research everything. But I keep ending up in the same place — broke.”

Here’s what Marcus didn’t realize: his brain was working against him every single day.

I Recognized the Pattern Because I Lived It

I know exactly how Marcus felt because I was that guy too. Smart, educated, convinced I was making rational financial decisions while my bank account stayed stubbornly empty.

I remember sitting in my apartment when I was 29, staring at my brokerage app. I had $12,000 invested across six different stocks I’d “researched.” Tesla, Apple, some biotech company I’d read about on Reddit. I felt sophisticated. Diversified.

Then the market dropped 15% in March 2020.

I sold everything. All of it. Within 48 hours.

Not because I needed the money. Not because my investment thesis changed. I sold because watching my account balance drop made my chest tight and my hands sweaty. I told myself I was “protecting my capital.” Really, I was letting my stone-age brain make a $180,000 decision.

Because that’s roughly what I missed when those same stocks recovered and doubled over the next two years.

Most people I talk to about behavioral finance get uncomfortable. They want to believe they’re rational actors making logical choices. The truth is messier.

Your Brain Is Running Code From 50,000 Years Ago

Here’s the thing about behavioral finance psychology and money decisions: your brain wasn’t designed for modern capitalism.

It was designed to keep you alive on the African savanna. When you see your investment portfolio drop 20%, the same neural pathways fire that would have fired if you’d heard a lion roar outside your cave.

Flight. Fight. Freeze.

None of these responses help you build wealth.

Marcus’s problem wasn’t that he was stupid. His problem was that he was human. Every month, he’d get paid and immediately start spending. Not because he was irresponsible — because his brain treated having money like having food during a famine.

Use it now, before it disappears.

This is loss aversion in action. Behavioral economists have proven we feel the pain of losing $100 about twice as strongly as we feel the pleasure of gaining $100. Your brain literally weights losses heavier than gains.

So when Marcus got a bonus, instead of investing it, he’d upgrade his car. Safer to turn cash into something tangible before the cash vanished. His caveman brain was protecting him from a threat that didn’t exist.

The Confirmation Bias Trap That Keeps Smart People Poor

Want to know why smart people make bad money decisions? They’re too good at justifying their choices.

Marcus would spend hours researching stocks. He’d read analyst reports, compare P/E ratios, study five-year growth charts. By the time he bought anything, he was convinced he’d found the next Amazon.

Then the stock would drop 30%.

Instead of admitting he might be wrong, Marcus would research more. He’d find articles that supported his original thesis. He’d discover reasons why the drop was temporary. Confirmation bias in personal finance doesn’t just make you wrong — it makes you expensively wrong for longer.

I watched him hold a biotech stock from $47 down to $8 because he kept finding reasons why he was right and the market was wrong.

The company went bankrupt six months later.

This is why 89% of day traders lose money over five-year periods. It’s not that they lack intelligence. It’s that their intelligence becomes a weapon their subconscious uses against them.

The Sunk Cost Fallacy Disguised as Discipline

Do you know what’s worse than behavioral economics traps?

When you mistake them for virtues.

Marcus told me he prided himself on never giving up on his investments. “I’m not a panic seller,” he’d say. “I stick to my convictions.”

Noble words. Expensive habit.

What he called “discipline” was actually sunk cost fallacy. He couldn’t sell his losing positions because he’d already lost so much money on them. Selling would mean admitting the initial decision was wrong. So he’d hold, and hold, and hold.

Meanwhile, his winners? He’d sell those the moment they went up 15%. “Lock in profits,” he’d tell himself. This is exactly backwards. Behavioral finance research shows most people cut their winners short and let their losers run long.

The result? Marcus’s portfolio looked like a graveyard of good companies he’d sold too early and bad companies he’d held too long.

Why Your Money Psychology Beats Your Strategy Every Time

Here’s what I learned after burning through $50,000 of my own money: your psychology is your strategy.

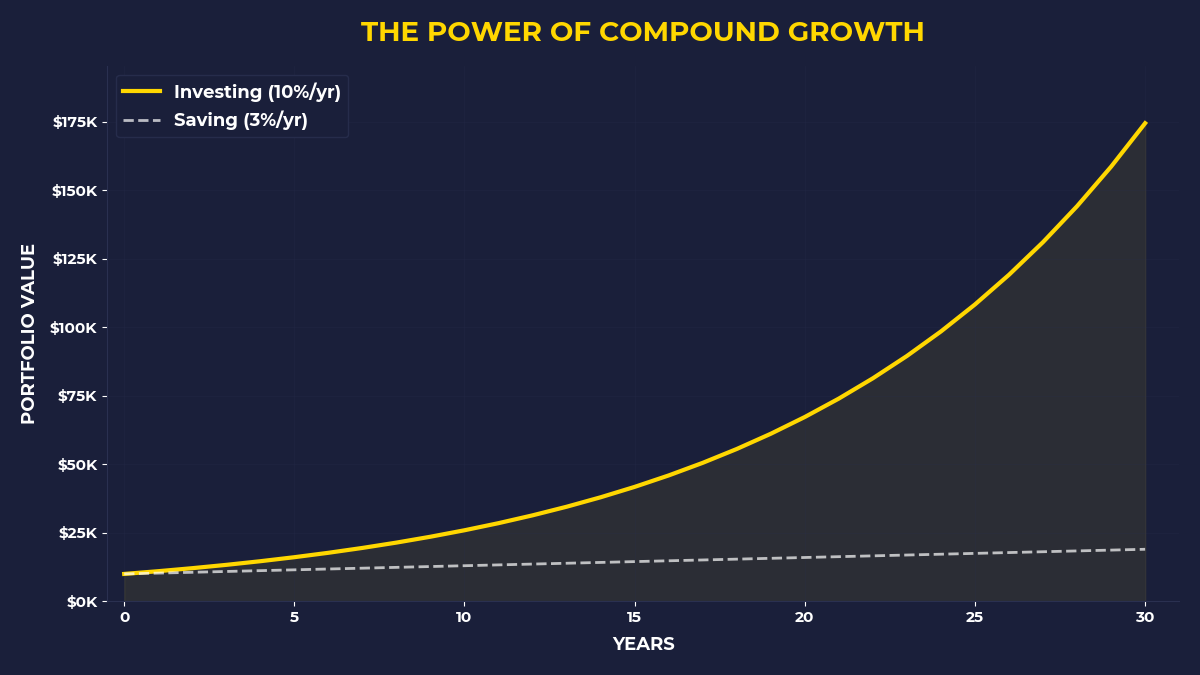

You can have the perfect investment plan on paper. You can understand compound interest. You can know that index funds beat 94% of active managers over 20-year periods.

None of that matters if your brain sabotages you every time the market gets scary.

I remember the exact moment this clicked for me. I was reading about Warren Buffett’s worst year — 1974-1975, when Berkshire Hathaway dropped 50%. Reporters asked him if he was worried.

“I felt like an oversexed guy in a harem,” Buffett said. “Everything was on sale.”

That’s not just a cute quote. That’s a completely different neural response to the same stimulus. While everyone else’s brains were screaming “DANGER! SELL EVERYTHING!”, Buffett’s brain was purring “opportunity.”

The difference wasn’t intelligence. It was programming.

How to Reprogram Your Money Brain

Look, I can’t give you Warren Buffett’s brain. But I can show you how to work with the brain you have.

First, automate everything you can. Marcus’s biggest breakthrough came when he set up automatic transfers. Every payday, $800 moved from checking to his brokerage account before he could think about it. His loss aversion couldn’t kick in because the money disappeared before his brain registered it as “his.”

Second, make selling harder than buying. Marcus deleted his brokerage app from his phone. If he wanted to panic-sell during a market crash, he’d have to log into his computer, remember his password, navigate to the trading page. Just enough friction to let his rational mind catch up to his emotional reaction.

Third, reframe volatility as opportunity. Every time Marcus saw his portfolio drop, instead of thinking “I’m losing money,” he trained himself to think “stocks are going on sale.” Same math, different emotional response.

The results spoke louder than any behavioral finance textbook. Over the next 18 months, Marcus’s net worth grew by $47,000. Not because he got smarter about picking stocks. Because he got smarter about managing his own psychology.

The One Realization That Changes Everything

If you’re someone who considers yourself rational, logical, immune to “behavioral biases” — this post is especially for you.

Because the smartest people are often the most dangerous to themselves. They trust their judgment completely. They believe their research makes them immune to psychological traps. They think behavioral finance applies to other people.

Marcus was losing money not despite his intelligence, but because of it. His brain was too good at convincing him his terrible decisions were actually brilliant strategies.

The One Thing To Remember

Your biggest enemy in building wealth isn’t the market, inflation, or economic uncertainty. It’s the three pounds of neural tissue between your ears, running code written 50,000 years ago. The moment you accept that your brain is actively working against your financial success, you can start designing systems to work with your psychology instead of against it. Smart people stay poor because they trust their brains to make good money decisions, when they should be trusting systems to make those decisions for them.

• Set up automatic investing before you can think your way out of it

• Delete trading apps from your phone to add friction to emotional decisions

• When markets crash, train yourself to think “sale” instead of “loss”

🎬 Prefer watching? Check out the video version on YouTube: