The Birthday Realization That Changes Everything

Marcus — 37, software architect in Denver — called me last September, three days after his birthday. His voice had that hollow quality people get when they’ve done math they don’t like.

“I make $140,000 a year,” he said. “I’ve been maxing out my 401k, saving 20%, doing everything right. But I just calculated how much I’ve sent to other people this year, and it’s insane.”

He rattled off the numbers: $2,100 monthly rent to his landlord. $850 car payment to Ford Credit. $320 student loan to Sallie Mae. $180 phone bill to Verizon. $89 internet to Comcast. $47 Netflix, Spotify, and subscriptions. $1,200 monthly groceries to Kroger shareholders.

“That’s $4,786 a month flowing to capital owners,” Marcus said. “Almost $58,000 a year. More than most people make.”

He paused. “And you know what I realized? Every single one of those companies has shareholders getting rich off my monthly payments. While I’m following some investment philosophy I learned from a book.”

I Built My Wealth On Someone Else’s Blueprint

I know exactly how Marcus felt because I spent my twenties doing the same thing.

I had this elaborate investment philosophy. Dollar-cost averaging into index funds. Diversification across asset classes. Rebalancing quarterly. I read Bogle and Buffett and felt sophisticated about my “long-term approach.”

Meanwhile, my landlord was collecting $1,850 every month from me and probably twelve other tenants. $22,200 annually from my unit alone. While I was proud of contributing $500 monthly to my investment accounts.

The math was right there, but I couldn’t see it.

My investment philosophy was designed by and for people who already owned capital. It assumed I had decades to let compound growth work its magic. It assumed my job would exist that long. It assumed gradual wealth accumulation through markets was my best path.

But here’s what those philosophies don’t tell you: while you’re slowly building wealth through approved investment channels, you’re rapidly building someone else’s wealth through your monthly bills.

Why Every Investment Philosophy Misses The Point

Most investment philosophies answer the wrong question.

They tell you what to do with money after you have it. Buy this asset class. Rebalance quarterly. Hold for twenty years. Diversify internationally.

But they skip the fundamental question: what should you buy before you pay anyone else?

Think about Warren Buffett as a kid, collecting golf balls from water hazards around Omaha country clubs. He’d clean them up and sell them for 6 cents each. But here’s the part most people miss: he didn’t just work harder to find more golf balls.

He asked a different question.

Instead of “how do I find more golf balls?” he asked “what should I buy with this golf ball money?”

The answer was a pinball machine. He placed it in a barber shop, split the profits with the owner, and used those profits to buy another machine. Within months, he had a small fleet of pinball machines across town, generating income while he slept.

That’s not an investment philosophy. That’s capital acquisition.

The Question That Separates Owners From Everyone Else

What if Marcus had asked himself a different question six months ago?

Instead of “how should I invest my extra $500 this month?” what if he’d asked “what should I buy that people need?”

Maybe he discovers his apartment building is for sale. The owner wants $1.2 million. Marcus can’t buy it alone, but he could organize five friends to split the ownership. They each put in $50,000 down and finance the rest.

Suddenly, Marcus isn’t sending $2,100 to a landlord every month. He’s collecting rent from eleven other tenants while living essentially free.

The building generates $23,100 monthly in gross rent. After mortgage, taxes, and maintenance, it nets maybe $8,000 monthly. Marcus’s share: $1,600 per month in passive income.

More importantly, he owns an asset that people need. Demand for housing isn’t going away. Every month, that building stores and converts demand into cash flow.

What Your Monthly Bills Actually Reveal

Do you know what your monthly bills really are?

They’re invoices from capital owners.

Your rent check goes to someone who owns real estate. Your car payment goes to someone who owns automotive capital. Your grocery bill goes to shareholders of Kroger, Walmart, or whoever owns your local chain.

Every subscription, every utility payment, every loan payment — it’s your cash flowing to people who own things that other people need.

The tragic part isn’t that you’re paying these bills. You have to live somewhere, eat something, get around somehow.

The tragic part is that you’re not asking the follow-up question: how do I get on the other side of this equation?

I spent years optimizing my investment portfolio while completely ignoring the fact that I was someone else’s optimal cash flow.

Why Capital Is Stored Demand, Not Money

Here’s what changed my entire approach to building wealth: understanding that capital isn’t money sitting in an account.

Capital is stored demand.

When Warren Buffett bought See’s Candies in 1972, he wasn’t buying a candy company. He was buying stored demand for chocolate during holidays, gifts, and celebrations. That demand converts to cash flow year after year.

When someone buys apartment buildings, they’re not buying buildings. They’re buying stored demand for housing. That demand converts to monthly rent checks.

When someone builds a SaaS business, they’re not building software. They’re building stored demand for a solution to a recurring problem.

The investment philosophy I was following treated capital like it was about picking the right stocks or funds. But capital is about owning things that other people need, want, or use repeatedly.

Your monthly bills are proof that this demand exists. Every payment you make is evidence of stored demand converting to someone else’s cash flow.

The Compound Interest Story Nobody Tells You

There’s a story about a guy named Harry from the 1930s that illustrates compound interest better than any textbook.

Harry was in a drugstore when someone asked him how much he weighed. He looked around, spotted a coin-operated scale, put in a penny, and got his answer. Over the next few minutes, he watched seven more people use that scale.

Curious, he asked the store owner about it. Turns out the owner rented the scale and kept 25% of the take — about $20 per month from that one machine.

Harry went home, withdrew $175 from his savings, and rented three scales for different locations. Within weeks, he was earning $98 monthly from machines that ran themselves.

But here’s the part that matters: Harry used profits from the first three scales to buy 67 more scales. Eventually he had 70 coin-operated scales across town, generating over $1,700 monthly in 1930s dollars.

That’s compound interest. But notice what compounded: ownership of assets that people used repeatedly.

Harry didn’t compound by reinvesting dividends in diversified portfolios. He compounded by buying more things that stored and converted demand into cash flow.

Your Emergency Fund Is Training You To Stay Poor

If you’re following conventional investment philosophy, you probably have an emergency fund sitting in a savings account earning 0.5% annually.

That emergency fund is training you to be poor.

Not because emergency funds are bad, but because they teach you that safety comes from hoarding cash rather than owning assets.

Robert Kiyosaki tells a story about living in a friend’s garage after his business failed. He and his wife were broke, facing mounting bills and creditor calls. But every time money came in, he paid himself first — meaning he bought investments before paying bills.

When there wasn’t enough left to cover expenses, he took side jobs. He mowed lawns and did odd jobs to make up the difference. The pressure to earn additional income motivated him more than the comfort of a cash cushion ever could.

Within a few years, the assets he’d bought while broke generated enough passive income to cover all his bills permanently.

That’s a completely different philosophy than “build up six months of expenses in savings, then invest what’s left.”

Stop Asking What You Should Do. Start Asking What You Should Buy.

Every success story about building wealth comes down to the same shift in thinking.

Instead of “what should I do to make more money?” the question becomes “what should I buy that other people need?”

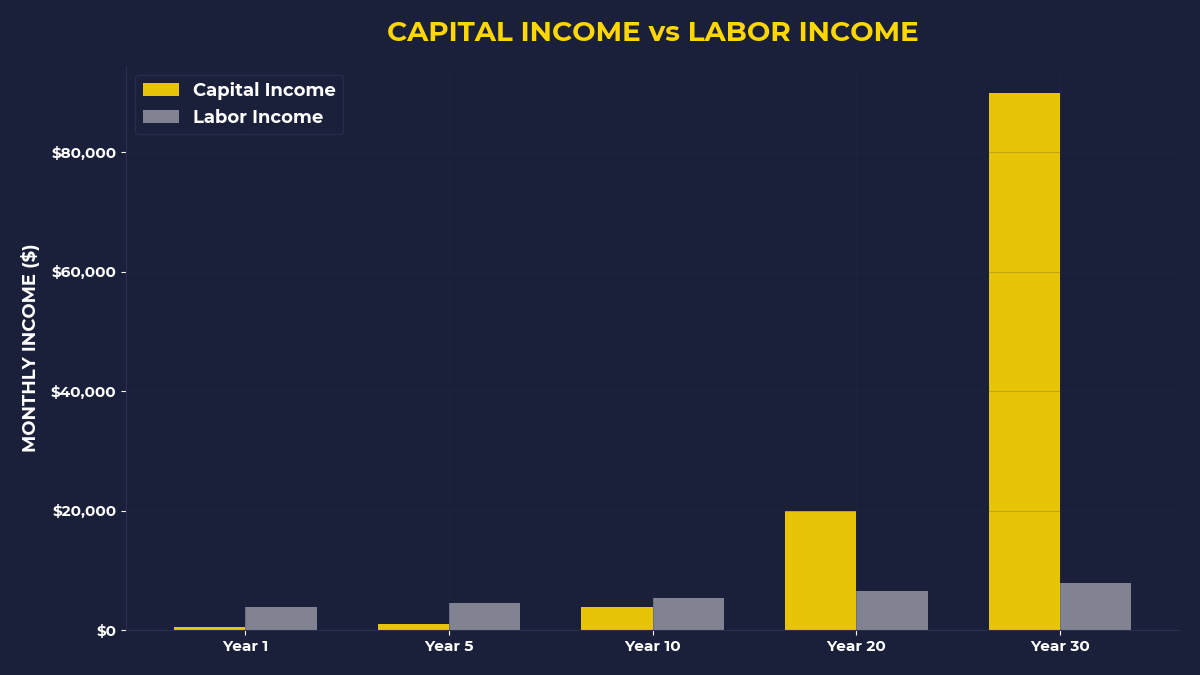

Marcus could keep following his investment philosophy, contributing $500 monthly to diversified index funds. In twenty years, he might have $300,000. That’s not nothing.

But what if he spent the next six months organizing that apartment building purchase? What if he used his next $3,000 bonus as a down payment on a small rental property? What if he bought a laundromat, or a vending machine route, or shares in a storage facility business?

The difference isn’t the amount of money. The difference is asking “what should I buy?” instead of “what should I do?”

People who ask what they should do become very good employees, consultants, and professionals.

People who ask what they should buy become capital owners.

The One Thing To Remember

Your investment philosophy isn’t your own if it doesn’t start with this question: what should you buy before you pay anyone else? Every month, thousands of dollars flow from your account to people who own things you need. That money is proof that demand exists and that ownership works. The goal isn’t to optimize how you invest your leftover money — it’s to flip the script so other people’s monthly payments become your monthly income.

- Before paying this month’s bills, identify one thing you pay for monthly that you could potentially own a piece of instead

- Calculate how much you send to capital owners annually (rent, car payments, subscriptions, utilities) — that number represents existing demand you could capture

- Ask “what should I buy with my next $1,000?” rather than “what should I do to earn more money?”

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.