The Morning Tom Realized He’d Been Playing Someone Else’s Game

Tom Martinez — 29, software developer in Denver — sat at his kitchen table last September, laptop open, staring at his bank statement. The numbers told the same story they’d been telling for three years: $4,200 in, $4,100 out. Every month.

His rent check had cleared that morning. $1,850 to his landlord. Then came the parade of other payments: car loan, student loans, utilities, groceries, Netflix, Spotify, gym membership. Each one a direct deposit into someone else’s account.

Tom made decent money. Six figures, actually. But somehow he always ended up with crumbs while everyone else got the meal.

He’d been following the conventional investment philosophy his whole adult life: save what’s left after expenses, put it in index funds, wait 30 years. The problem? There was never anything left.

I Know Exactly How Tom Felt

Look, I used to have the same backwards investment philosophy.

When I was 26, I made $68,000 at a tech startup in Austin. I thought I was doing everything right. I read all the personal finance blogs. I had my budget spreadsheets. I even maxed out my 401k match.

But every month felt like financial quicksand. I’d get my paycheck, and by the time I paid rent ($1,200), student loans ($340), car payment ($280), and everything else, I had maybe $200 left for “investing.” Some months, nothing at all.

Here’s the thing I didn’t understand then: my entire investment philosophy was designed by the people who were already getting my money.

The financial advice industry tells you to pay all your bills first, then invest what’s left. That sounds responsible, right? It’s actually a trap.

Your Monthly Bills Are Invoices From Capital Owners

Every dollar Tom sent out that morning went to someone who owned something he needed.

His landlord owned the apartment. The bank owned his car loan. Sallie Mae owned his student debt. Spotify owned the music platform. Amazon owned his shopping habits.

Each payment was a dividend to a capital owner.

Tom was following the classic investment philosophy: work hard, pay everyone else first, save what’s left. The system works perfectly — for the capital owners collecting his checks.

Think about your own monthly outflow. How much goes to rent or mortgage? Car payments? Subscriptions? Loan payments? Add it up. That’s your monthly dividend payment to other people’s investment portfolios.

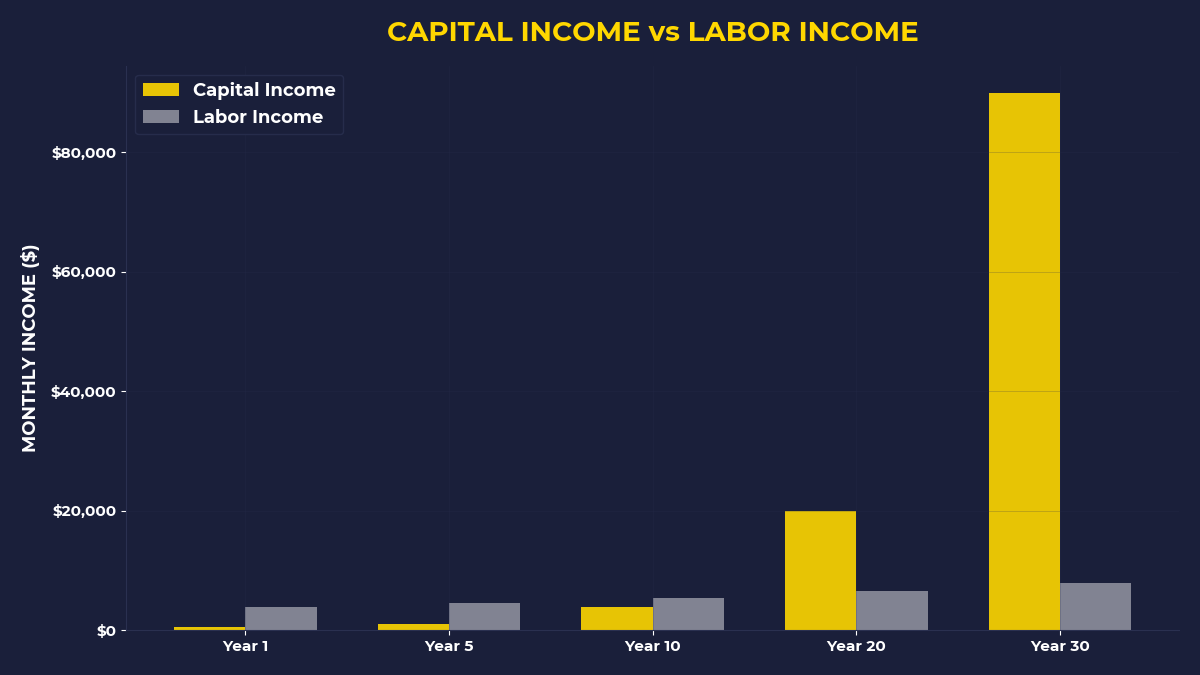

The brutal truth? Most people spend their entire lives paying dividends to capital owners while never becoming one themselves.

The Investment Philosophy Nobody Teaches You

Six months after that kitchen table moment, Tom did something that sounded completely irresponsible.

When his next paycheck hit, he immediately transferred $500 to his brokerage account. Before rent. Before groceries. Before anything.

His friends thought he was crazy. “How are you going to pay your bills?”

Tom figured it out. He picked up freelance work on weekends. He sold some stuff. He ate ramen for two weeks. But he kept that $500 invested.

The next month, he did it again. Then again.

By month six, something interesting happened. Tom wasn’t scrambling anymore. The pressure of having skin in the game — actual capital at risk — made him more resourceful, not more broke.

He started asking different questions. Instead of “How do I pay all these bills?” he asked “How do I own something that pays me?”

Why This Investment Philosophy Actually Works

When you pay yourself first — literally first — you flip the entire wealth-building equation.

Here’s what conventional wisdom gets wrong: it assumes your expenses are fixed and your investment capacity is variable. That’s backwards.

Your investment capacity should be fixed. Your expenses should be variable.

Robert Kiyosaki tells a story about living in a friend’s garage after his business failed. He was drowning in bills. But instead of using every dollar to pay creditors, he used his first dollars to buy assets. Then he worked nights and weekends — mowing lawns, odd jobs — to cover the bills.

People thought he was financially reckless. But here’s what happened: the pressure forced him to generate more income rather than just manage existing income better.

That’s the difference between a wealth-building investment philosophy and a wealth-maintenance investment philosophy.

Are You Building Wealth or Just Managing Poverty?

Most investment advice is really poverty management disguised as wealth building.

“Make a budget.” “Cut unnecessary expenses.” “Save what’s left.” These are all about managing scarcity better, not creating abundance.

A real investment philosophy for building wealth starts with one question: What can I buy this month that will pay me back?

Not what can I afford after paying everyone else. What can I buy first, then figure out the rest?

This isn’t about being irresponsible with money. It’s about being responsible to your future self instead of just your current creditors.

The Golf Ball Principle Applied to Investment Philosophy

Warren Buffett used to collect lost golf balls as a kid and sell them back to golfers. But here’s the key part nobody talks about: he didn’t spend that money on candy or toys.

He used every dollar to buy more income-producing assets. First more golf ball inventory. Then eventually rental properties, then stocks in businesses.

The pattern was always the same: earn money, immediately reinvest in something that produces more money, use surplus from that to cover living expenses.

Most people do this backwards. They cover living expenses first, then invest leftovers. That’s why most people never accumulate meaningful capital.

The investment philosophy that actually builds wealth is simple: buy assets first, figure out expenses second.

If You’re Someone Who Always Runs Out of Money to Invest

This post is for you if you make decent money but somehow never have any left for building wealth.

If you’ve been following conventional investment philosophy — pay bills first, save what’s left — and getting nowhere.

If you’re tired of sending your paycheck to other people’s investment portfolios while your own stays empty.

This isn’t for you if you’re already disciplined about investing a fixed percentage every month. You’ve figured it out.

This also isn’t for you if you’re in true survival mode — genuinely struggling to cover basic needs. Get stable first. Then flip the script.

The One Thing To Remember

Your investment philosophy reveals who you’re really working for. If you pay everyone else first and invest what’s left, you’re working for your landlord, your bank, and your creditors. If you invest first and figure out expenses second, you’re working for yourself. The difference isn’t about the amount you invest — it’s about who gets priority access to your income.

Start this month:

• Move 10% of your next paycheck to investments before paying any bills — even if it feels scary

• When bills pressure mounts, ask “How do I generate more income?” not “How do I cut more expenses?”

• Every month, buy something that has the potential to pay you back — stocks, skills, or systems

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.