Sarah’s $4,200 Monthly Invoice

Sarah Martinez — 29, marketing coordinator in Denver — opened her laptop on a Tuesday morning and did something most people avoid. She added up every monthly payment that left her bank account.

Rent: $1,650. Car payment: $420. Student loans: $340. Phone: $85. Utilities: $160. Netflix, Spotify, gym membership: $67. Groceries and daily coffee runs: another $480.

The number hit her like cold water: $4,200.

Every single month, Sarah sent $4,200 to other people. People who owned things. Her landlord owned the apartment building. The bank owned her car loan. Sallie Mae owned her education debt. Verizon owned the cell towers. Even her $6 daily latte went to someone who owned a coffee shop.

She stared at the screen. “I’m sending invoices to capital owners,” she whispered. “Every damn day.”

I Used to Be Sarah (And I Hated the Math)

I know exactly how Sarah felt because I was there too. When I was 27, working as a junior analyst in Chicago, I did the same calculation. My monthly outflow was $3,800 — and that was in 2016 dollars.

Here’s what made me sick to my stomach: I realized I was part of a machine. Every morning, millions of people wake up and send their paychecks to capital owners. Rent checks, mortgage payments, car notes, credit card minimums, subscription fees — it’s all cash flowing upward to people who own assets.

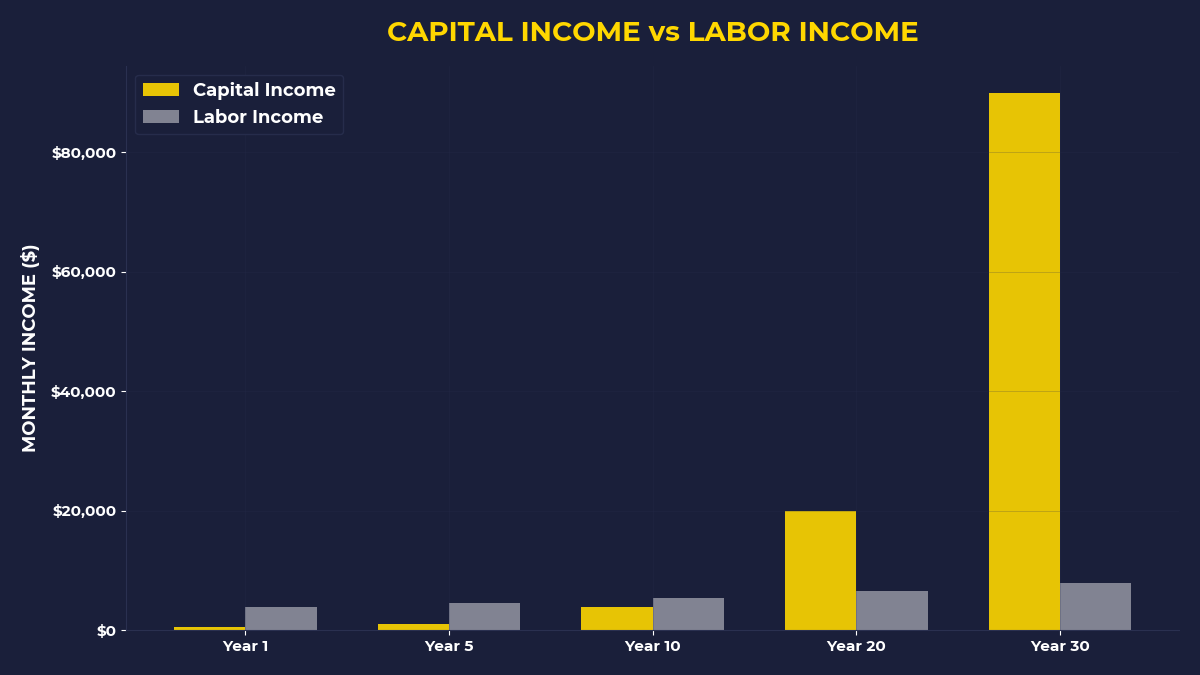

The average American household sends roughly $3,400 per month to asset owners, according to Bureau of Labor Statistics data. That’s $40,800 per year. Over a 30-year working career, that’s $1.2 million flowing from your checking account to someone else’s investment portfolio.

Think about that.

For three decades, you’ll write checks to people who own what you need. Meanwhile, you’ll own what — a depreciating car and some furniture?

What Capital Actually Is (Not What You Think)

Most people think capital is money sitting in a bank account. Wrong.

Capital is stored demand. It’s owning something people need, want, or can’t avoid paying for. When people need what you own, you have capital.

Sarah’s landlord owns capital — an apartment building in a city where people need housing. The bank that holds her car loan owns capital — a legal claim on her future income. Netflix owns capital — a platform people pay for entertainment.

Every bill you pay is proof that someone else owns capital and you don’t.

Let me tell you about my friend David — 34, UX designer in Austin — who figured this out the hard way. David was making $95,000 per year but felt broke every month. He came to me frustrated: “I’m good at my job, I work hard, but I never get ahead.”

I asked him one question: “What do you own that pays you back?”

Silence.

David owned a car (depreciating), furniture (depreciating), and had $8,000 in savings (earning 0.05% interest). He owned exactly zero assets that generated income. Meanwhile, he was sending $4,100 per month to people who owned his apartment building, his car loan, his phone service, his everything.

Why Famous People Get Rich (While You Get Bills)

Ever wonder why a singer can make millions from one hit song while a nurse — who literally saves lives — makes $65,000 per year?

It’s not about effort. It’s not about value to society. It’s about capital.

When a singer creates a hit song, they own capital — intellectual property that generates royalties every time someone streams it. Millions of people want to hear that song. The singer owns what people demand. That’s stored demand generating cash flow.

The nurse works harder, arguably provides more value, but owns no capital. She trades time for money, hour by hour, shift by shift. No stored demand. No leverage.

This isn’t fair, but it’s how capital works. People who own what others need collect rent on human existence.

The Day I Switched Sides

I remember the moment everything clicked for me. I was sitting in my Chicago apartment, looking at my brokerage app showing $347 in my account, when I got three bills in one day: rent ($1,450), car payment ($380), and student loans ($290).

I was tired of being the person who sends money. I wanted to be the person who receives it.

So I made a decision that felt insane at the time. Before I paid any of those bills, I moved $200 from my checking account into my brokerage and bought shares of an index fund. Even though I’d have to scramble to cover rent. Especially because of that.

My logic was simple: if I always pay everyone else first, I’ll never own anything. If I pay myself first — even $200 — at least I own something.

That $200 was my first piece of capital. Tiny, but real.

Within that fund were hundreds of companies that millions of people pay every day. Apple, Microsoft, Amazon — companies that collect money from people like me, but now I owned a microscopic slice of that collection system.

Are You Ready to Stop Being an ATM?

Here’s what most people miss about building wealth: it’s not about making more money. It’s about switching sides in the capital game.

Right now, you’re probably on the wrong side. You work for wages, then send those wages to capital owners. You’re feeding a system that doesn’t feed you back.

The goal isn’t to eliminate all bills — you need housing, transportation, and food. The goal is to own assets that generate the cash flow to pay those bills.

Think of it this way: Warren Buffett pays rent too. But his stock portfolio generates enough dividend income to cover his rent, his food, his everything. The capital works so he doesn’t have to.

That’s time freedom. The most underrated form of wealth.

The Capital Question That Changes Everything

Most people ask: “How can I make more money?” That’s a labor question. It leads to longer hours, side hustles, and trading more time for dollars.

Capital owners ask: “What should I buy?” That’s the leverage question. It leads to assets that work while you sleep.

When Warren Buffett was 11 years old, he found lost golf balls and sold them for 6 cents each. Normal kid story, right? Wrong. The insight came later: instead of looking for golf balls himself, he hired friends to find them. He paid them 2 cents per ball and kept 4 cents profit.

While his friends traded their time for money, Warren bought their time and kept the difference. He was asking “what should I buy?” while they were asking “what should I do?”

That question — “what should I buy?” — is the dividing line between capital owners and everyone else.

Your First $100 of Capital

You don’t need thousands of dollars to start owning capital. You need to change one habit.

Next time you get paid, before you pay rent, before you buy groceries, before you do anything — move some money into a brokerage account and buy index fund shares. Even if it’s just $50. Even if it makes money tight that week.

I know this sounds backwards. “How can I invest when I can barely pay my bills?”

That’s exactly why you need to invest. If you always pay bills first, you’ll never own assets. The bills will expand to consume every dollar you make.

Remember Sarah from the beginning? After our conversation, she started moving $150 per month into VTI — Vanguard’s total stock market index — before paying any bills. First week was stressful. But something shifted in her brain. She started seeing herself as someone who owns capital, not just someone who pays bills.

Eighteen months later, she owns $3,200 worth of capital. Still small, but growing. Those shares represent tiny ownership stakes in 4,000+ companies that millions of people pay every day. Sarah switched sides.

The One Thing to Remember

Every day, people choose between two games: the labor game and the capital game. In the labor game, you trade time for money, then send that money to capital owners. In the capital game, you own assets that collect money from people playing the labor game. The only way to win is to recognize which game you’re playing and deliberately switch sides.

If you’re someone who works hard but never seems to get ahead, who pays bills month after month but never builds wealth, who feels trapped trading time for money — this post is for you.

Three things you can do today:

• Calculate your monthly outflow to capital owners (rent, loans, subscriptions, everything)

• Open a brokerage account if you don’t have one

• Move $50-200 into index fund shares before paying your next bill

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.