Marcus — 29, marketing coordinator in Denver — opened his laptop on a Tuesday morning and stared at something that would haunt him for months. His bank account showed $2,847. Not bad for mid-month. Then he opened his email and saw seventeen separate bills waiting for him. Rent: $1,650. Car payment: $389. Student loans: $247. Phone: $85. Netflix, Spotify, gym membership: another $67 combined. Insurance: $156. Utilities: $94.

He did the math twice.

After bills, he had $159 left for groceries, gas, and whatever passed for a social life in his late twenties. Marcus had been working for seven years since college. Good job, steady promotions, responsible with money. And yet somehow, he was sending $2,688 to other people every single month while keeping almost nothing for himself.

That’s when it hit him: his bills weren’t expenses. They were invoices from capital owners.

I Missed This Pattern for Years

I know exactly how Marcus felt because I lived it too. When I was 26, I made a spreadsheet of where my money went each month. Rent to my landlord. Car payment to the bank. Insurance premiums to the insurance company. Phone bill to Verizon. Groceries to whoever owned the supermarket chain.

Every single dollar I earned as salary was pre-assigned to someone who owned something I needed to use.

Look at your own checking account right now. How much of last month’s paycheck is still there? If you’re like 78% of Americans, the answer is almost nothing. Not because you’re irresponsible — because you’re systematically transferring your labor’s output to people who own the things you need to live.

The rent check alone proves the point. Marcus pays $1,650 monthly to live in a space someone else owns. Over a year, that’s $19,800 flowing from his labor to their asset. Over five years: $99,000. Over a typical lease lifetime: nearly $200,000 of his earned income converted into someone else’s equity.

What Capital Really Is

Here’s what took me years to understand: capital isn’t money sitting in your bank account. Capital is stored demand. It’s owning something that people need, want, or use repeatedly.

Marcus’s landlord owns stored demand — the demand for housing in Denver. Every month, Marcus and dozens of other tenants convert their labor into the landlord’s capital appreciation and cash flow. The landlord doesn’t work for that $1,650. The building works for it.

Think about that. The building — a physical asset — extracts value from Marcus’s marketing job without the owner lifting a finger.

The car loan works the same way. Marcus drives a 2019 Honda Civic that he doesn’t own. He pays $389 monthly to the bank that financed it, plus interest. The bank owns the title until Marcus finishes paying them $28,000 for an asset currently worth $16,000. They’ve structured demand — people need transportation — into a cash-generating machine.

Even Netflix owns stored demand. Marcus pays $15.49 monthly because they control content he wants to watch. Multiply that by 238 million global subscribers, and Netflix converts billions of people’s labor into their shareholders’ equity.

The Two-Sided Money Flow

Every bill reveals the same pattern: money flowing from people who work to people who own.

Your phone bill? It’s profit for telecom shareholders. Your insurance premium? Profit for insurance company owners. Your grocery bill? Profit for supermarket chain investors and food company shareholders. Your gas tank fill-up? Profit for oil company equity holders.

We’re trained to see these as normal expenses. But they’re actually wealth transfers. You create value through your job, then immediately send that value to capital owners through your bills.

The system is designed perfectly — for them.

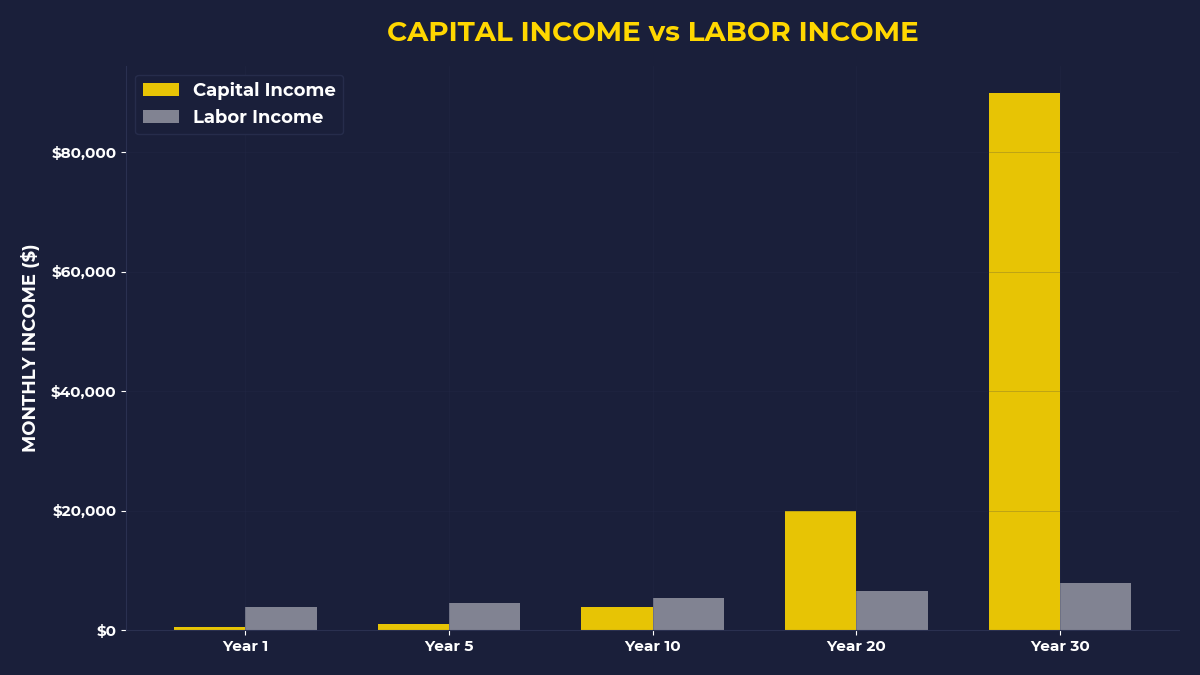

Why This Matters More Than Your 401k

Most financial advice focuses on the wrong end of the equation. Save more. Budget better. Invest in index funds. But if you’re sending 85% of your income to capital owners every month, optimizing the remaining 15% won’t fundamentally change your situation.

I learned this when I met Sarah, a 34-year-old nurse in Austin who had been maxing out her 401k for eight years. She was doing everything “right” financially — except she was still living paycheck to paycheck despite earning $73,000 annually. Why? Because her bills consumed $4,200 of her $4,600 monthly take-home pay.

Even with $180,000 in retirement savings, Sarah was structurally trapped. Her bills guaranteed that capital owners would capture most of her labor’s value for the next thirty years.

That’s when Sarah had the same realization Marcus did: the goal isn’t to budget better. It’s to switch sides.

The Capital Owner Mindset

What if instead of asking “How can I afford my bills?” you asked “How can I own something that generates bills for other people?”

This is how capital owners think. They don’t focus on managing expenses — they focus on acquiring assets that generate income from other people’s expenses.

Warren Buffett doesn’t budget his grocery bill. He owns shares in grocery store companies that collect money from millions of people buying groceries. Jeff Bezos doesn’t optimize his Amazon Prime membership — he owns the company that collects $139 annually from 200 million members.

The landlord who collects Marcus’s $1,650 monthly isn’t managing a household budget. They’re managing an asset that converts other people’s budgets into their wealth.

The Smallest Possible Start

You don’t need millions to begin owning stored demand instead of just paying for it.

When Marcus realized his bills were wealth transfers, he made one change: before paying any bill each month, he moved $200 into a brokerage account and bought shares of companies that collect bills from people like him.

Verizon pays dividends to shareholders from phone bills like his. Public Storage pays dividends from storage unit rentals. Realty Income pays monthly dividends from rent collected at thousands of commercial properties.

Same money, different direction. Instead of Marcus’s $200 flowing to capital owners, it was buying him microscopic ownership in the systems that collect money from other people’s bills.

The first month was uncomfortable. Marcus had to scramble to cover his car payment. But something fundamental shifted: for the first time in his working life, he owned something that paid him instead of something he paid.

The One Thing To Remember

Your bills aren’t expenses — they’re invoices from capital owners. Every month, you’re converting your labor into other people’s equity while building none for yourself. The wealth gap isn’t about income differences; it’s about ownership differences. Some people pay bills. Other people collect them. The fastest way to financial freedom isn’t budgeting better — it’s gradually switching from the first group to the second.

Before paying any bill this month, move $50-200 into a brokerage account and buy shares of dividend-paying companies

Pick one monthly bill and research who ultimately profits from it — then consider buying their stock instead of just paying their invoice

Calculate how much you’ve paid in rent over the past five years, then imagine if that money had bought rental property shares instead

🎬 Prefer watching? Check out the video version on YouTube: