The Philosophy You Think Is Yours

Your investment philosophy isn’t yours. It’s a carefully curated collection of other people’s wealth-building strategies, packaged and sold back to you while they keep the real profits.

Think about it. Where did your “diversify across asset classes” mantra come from? The same financial industry that makes money on every trade you make. Your “buy and hold index funds” approach? Popularized by people who got rich selling books about it, not doing it at scale. Your “dollar-cost average into the market” strategy? Perfect for fund companies collecting fees on your automatic contributions for decades.

Here’s what I wish someone had told me when I was 28, sitting in my apartment, reading every investment book I could find: The people teaching you how to build wealth already have theirs. And their wealth came from something completely different than what they’re teaching you.

When I Discovered My Philosophy Wasn’t Mine

I used to think I was a sophisticated investor. I had my asset allocation spreadsheet. I rebalanced quarterly. I talked about efficient market theory at dinner parties.

Then I started paying attention to where my money actually went.

Every month, $2,200 disappeared to my landlord. Another $450 to my car payment. $180 to insurance companies. $320 to utilities. $1,100 to groceries and restaurants. By the time I finished paying everyone else, I had maybe $800 left to “invest” in my carefully constructed portfolio.

I was following an investment philosophy designed by people who didn’t have $2,200 rent payments.

The revelation hit me like a freight train: I wasn’t building wealth. I was funding other people’s wealth while convincing myself I was being responsible. My investment philosophy was actually their business model.

The Real Philosophy Behind Every Fortune

Want to know what every wealthy person’s actual investment philosophy looks like? Here it is:

Buy things that generate cash flow from other people’s needs.

That’s it. Not “diversified portfolio of low-cost index funds.” Not “balanced approach to risk management.” Not “long-term value investing with a contrarian twist.”

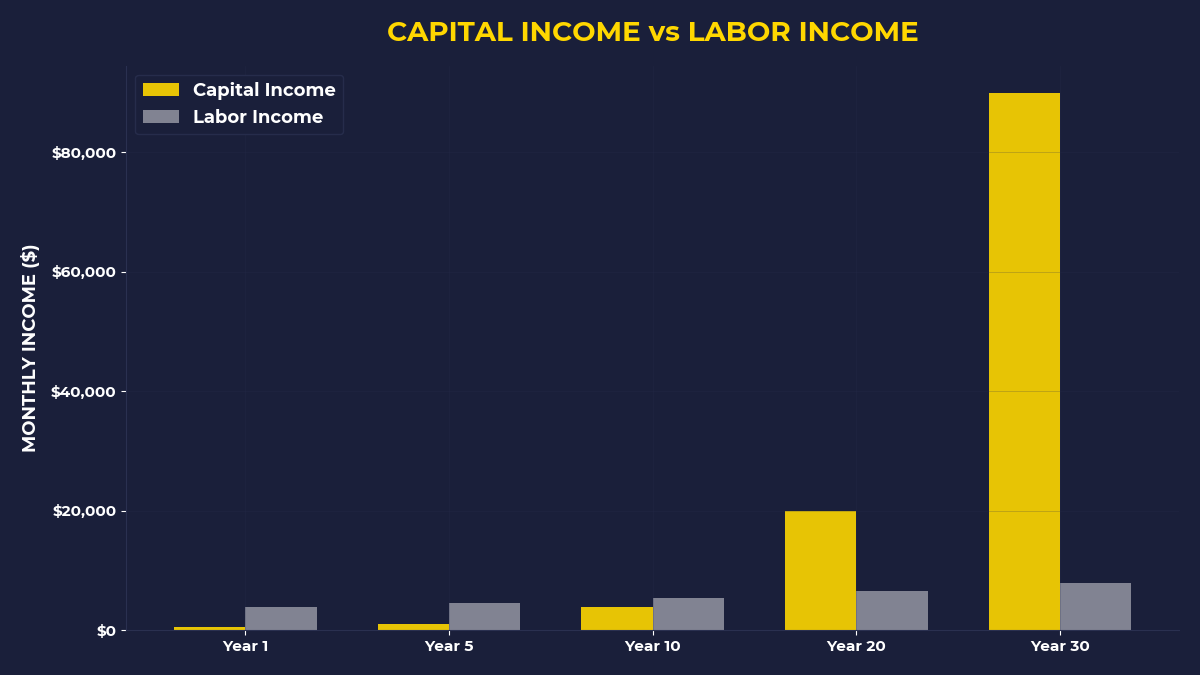

Warren Buffett didn’t get rich dollar-cost averaging into the S&P 500. He bought entire businesses that generated cash from millions of customers. Charlie Munger didn’t build his fortune through modern portfolio theory. He bought apartment buildings in 1960s Los Angeles and collected rent checks for decades.

The wealthy understand something that investment advisors will never tell you: capital is stored demand, not money sitting in accounts.

When you own Apple stock, you own a sliver of the cash flow generated by 1.4 billion people who can’t live without their iPhones. When you own real estate, you own the cash flow generated by people who need shelter. When you own a business, you own the cash flow generated by customers solving their problems.

But when you own a “diversified portfolio,” you own a little bit of everything and not enough of anything that matters.

Why Your Brain Keeps You Following Other People’s Plans

Your brain is wired to follow investment philosophies that keep you poor. It’s not your fault – it’s evolutionary programming.

Loss aversion makes you crave “safety” and “diversification.” You’ll accept 7% returns over 30 years instead of taking concentrated bets on businesses you understand. Herding instinct makes you feel comfortable doing what everyone else does. Social proof makes you trust the advice of people who sound smart on financial television.

Here’s the behavioral trap: the investment philosophy that feels safest is usually the one that keeps you dependent on employment income forever.

Think about that. The “safe” approach – dollar-cost averaging into diversified funds for 40 years – requires you to work for four decades and hope nothing goes wrong. The “risky” approach – buying concentrated positions in businesses you understand – could free you from needing a paycheck in a fraction of that time.

Which one is actually riskier?

What Happens When You Steal Their Real Philosophy

I started asking different questions three years ago. Instead of “What should I invest in?” I asked “What should I buy that generates cash flow?”

Instead of spreading $500 per month across eight different index funds, I saved up $6,000 and bought dividend-paying stocks in companies I couldn’t live without. Instead of buying REITs through my brokerage account, I started looking at actual rental properties in my city.

Instead of asking “How should I diversify?” I asked “How can I own pieces of things people pay for every month?”

The shift sounds simple, but it changes everything. When you think like a capital owner instead of a portfolio manager, you start seeing opportunities everywhere.

You notice that everyone in your apartment building pays rent to the same landlord. You realize that every coffee shop in your neighborhood pays rent to property owners. You see that every subscription service you use generates cash flow for shareholders.

You stop thinking about “asset allocation” and start thinking about “demand allocation.”

The Question That Reveals Your Real Philosophy

Here’s how to know if you’re following your investment philosophy or someone else’s wealth plan:

What percentage of your investment returns come from cash payments versus price appreciation?

If the answer is “mostly price appreciation,” you’re speculating on other people’s opinions about future values. If the answer is “mostly cash payments,” you’re collecting money from ongoing demand.

Price appreciation depends on someone else being willing to pay more than you did. Cash flow depends on people continuing to need what you own a piece of.

Which one sounds more reliable to you?

During the 2008 financial crisis, the S&P 500 dropped 57% between October 2007 and March 2009. But McDonald’s kept serving burgers. Coca-Cola kept selling drinks. Johnson & Johnson kept making products people needed. The cash flows didn’t disappear – just the opinions about what those cash flows were worth.

The investors who focused on cash-generating assets survived. The ones who focused on portfolio theory got wiped out.

If You’re Tired of Building Other People’s Dreams

This matters most if you’re tired of watching your paycheck disappear to other people’s investments while you slowly accumulate shares in diversified funds.

You don’t need permission to change your philosophy. You don’t need to wait until you have more money. You don’t need to take a course or read another book about modern portfolio theory.

You just need to start thinking like someone who wants to collect cash flow instead of someone who wants to own a little bit of everything.

Look around your life. Every bill you pay represents cash flow going to a capital owner. Your rent check goes to someone who owns real estate. Your phone bill goes to telecommunications shareholders. Your grocery bill goes to food company investors.

The question is: do you want to keep sending those checks, or do you want to start receiving them?

What The Primal Investor Takes Away

• Stop asking “How should I diversify my portfolio?” Start asking “What generates cash flow from ongoing demand?”

• Focus on businesses and assets that people pay for monthly, not investments that might appreciate someday

• Measure your progress by cash flow received, not account balance fluctuations

• Buy concentrated positions in things you understand rather than diversified positions in everything

• Think like a capital owner collecting payments, not a portfolio manager managing risk

• Remember that every bill you pay funds someone else’s investment philosophy – make sure yours generates the same income

Your real investment philosophy should be simple: own pieces of what people can’t live without. Everything else is just portfolio decoration designed to keep you employed while other people collect the cash.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.