The Day My Friend Learned What Contrarian Really Means

Marcus — 29, software engineer in Denver — called me three weeks after the market dropped 8% in February. “I finally did it,” he said, voice buzzing with pride. “I bought the dip. Amazon, Apple, Tesla. I’m being contrarian now.”

I had to break it to him. “Dude, you just did exactly what 47 million other people did that week.”

Marcus went quiet. He’d read all the same articles I had: “Why This Market Drop Is a Buying Opportunity.” “Smart Money Is Backing Up the Truck.” Every financial Twitter account was screaming the same thing. Buy the dip. Be greedy when others are fearful.

But here’s what Marcus missed — and what most people calling themselves “contrarian investors” never understand: By the time everyone’s talking about buying the dip, you’re not contrarian anymore.

You’re just late to the party.

I Made the Same Mistake for Three Years

Let me be honest. I spent my twenties thinking I was Warren Buffett every time the S&P 500 dropped 5%. I’d see red on my portfolio app and think, “This is it. This is my moment to be contrarian.” I’d scrape together whatever cash I had sitting around — usually about $300 — and buy more index funds.

Then I’d watch CNBC and see Jim Cramer telling millions of viewers to do the exact same thing. That’s when it hit me.

Real contrarian investing isn’t about market timing. It’s not about buying when stocks are down 10% and everyone’s panicking. That’s just following the crowd with a 48-hour delay.

True contrarian investing happens when you’re broke.

The Real Contrarian Move Nobody Talks About

Think about the last time you were really tight on money. Rent due in three days, checking account showing $127, credit card already maxed. What did every financial advisor, every blog, every piece of conventional wisdom tell you to do?

Build an emergency fund first. Get out of debt. Don’t even think about investing until you have six months of expenses saved.

That advice isn’t wrong. But it’s not contrarian either.

Here’s what real contrarian investing looks like: You take $25 from that $127 and buy something that pays you back. A fractional share of a dividend stock. A piece of a rental property through a REIT. One square foot of warehouse space in a logistics fund.

Everyone around you thinks you’re insane. “You can barely afford groceries and you’re buying stocks?” But that’s exactly the point.

You’re buying assets when you can least afford to. When it makes no logical sense. When the conventional wisdom says to focus on debt and emergencies first.

That’s contrarian.

Why Your Emergency Fund Is Training You to Stay Poor

I know this sounds reckless. But stay with me here.

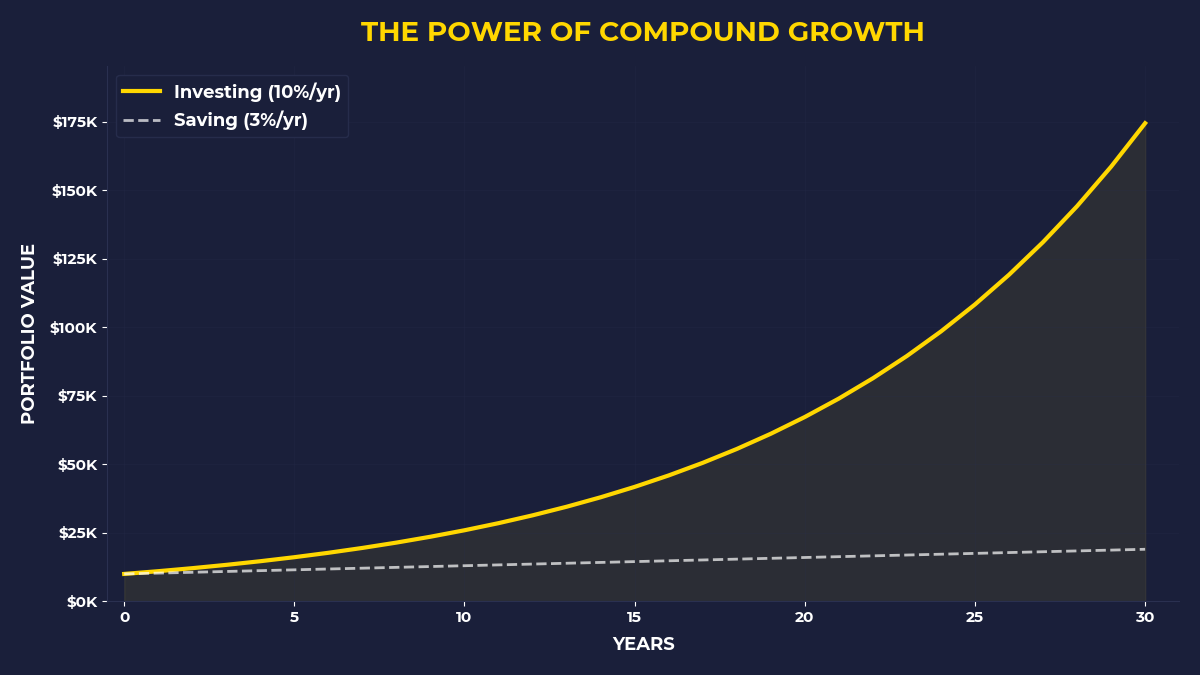

The emergency fund advice comes from a good place. But it’s also advice designed to keep you exactly where you are. Think about what an emergency fund really is: money sitting in a savings account, earning 0.5% interest, losing value to inflation every single day.

It’s dead money. Safe money. Conventional money.

Meanwhile, the assets you could be buying — even in tiny amounts — are working for you. They’re generating cash flow. They’re giving you ownership in companies where other people go to work every day to make you money.

I’m not saying blow off emergencies. I’m saying the real emergency is staying broke your entire life because you followed advice designed to keep you comfortable, not wealthy.

The Korean Golfer Who Changed How I Think About Capital

A friend of mine told me about this golfer in Seoul — let’s call him Kim. Mid-thirties, decent job at Samsung, living paycheck to paycheck like most people his age. But Kim had this weird habit.

Every month, before he paid any bills, he’d buy one share of Samsung stock. Didn’t matter if rent was due. Didn’t matter if his credit card was maxed. One share, every month, for seven years.

His friends thought he was crazy. His girlfriend (now wife) threatened to leave him twice. “We can’t afford groceries and you’re buying stocks?”

But Kim understood something they didn’t. He understood that Samsung was paying him to own a piece of the company where he worked. Every quarter, they sent him dividends. Every year, the stock price generally went up as the company grew.

After seven years, Kim owned 84 shares worth about $47,000. The quarterly dividends were covering his monthly phone bill. He’d built a tiny money machine while everyone else was building emergency funds.

That’s contrarian investing.

What Most People Get Wrong About Being Contrarian

Here’s the thing most “contrarian investors” never figure out: It’s not about being different from the market. It’s about being different from yourself.

Your brain is wired to follow patterns that kept your ancestors alive. Save resources for emergencies. Don’t take risks when resources are scarce. Pay the most urgent bills first.

This worked great when the biggest threat was starvation. It’s terrible advice for building wealth in a capitalist system.

In capitalism, the people who own assets get paid by the people who don’t. Every month, your rent check goes to someone who owns real estate. Your Netflix payment goes to shareholders. Your grocery bill goes to people who own pieces of Walmart and Kroger.

The contrarian move isn’t buying stocks when they’re down 10%. It’s buying stocks when you’re down to your last $100.

Wild, right?

The $47 Experiment That Changes Everything

If you’re someone who’s tired of watching your paycheck disappear into other people’s pockets, here’s what real contrarian investing looks like:

Next time you get paid — before you pay rent, before groceries, before anything — move $47 into a brokerage account. Buy a fractional share of something that pays dividends. Verizon. Johnson & Johnson. A REIT that owns apartment buildings.

Your brain will scream at you. “You can’t afford this!” “What about emergencies!” “This is irresponsible!”

That screaming is how you know you’re being contrarian.

Then, when bills are due and you’re short $47, figure out how to make it up. Work an extra hour. Sell something. Skip the coffee runs for two weeks. Do whatever it takes.

This forces you to think like a capital owner, not a wage earner. Capital owners pay themselves first, then figure out the rest. Wage earners pay everyone else first, then wonder why there’s nothing left.

The One Thing to Remember

Real contrarian investing isn’t about market timing or buying crashes. It’s about doing the opposite of what broke people do with money. Broke people pay bills first, save second, invest never. Contrarian investors buy assets first, then scramble to cover everything else. It feels backwards because it is backwards — and that’s exactly why it works.

• Move money to investments before paying non-essential bills this month

• Buy one share of a dividend-paying stock with your next $50 windfall

• When you feel financially stressed, that’s when you buy more assets, not fewer

🎬 Prefer watching? Check out the video version on YouTube: