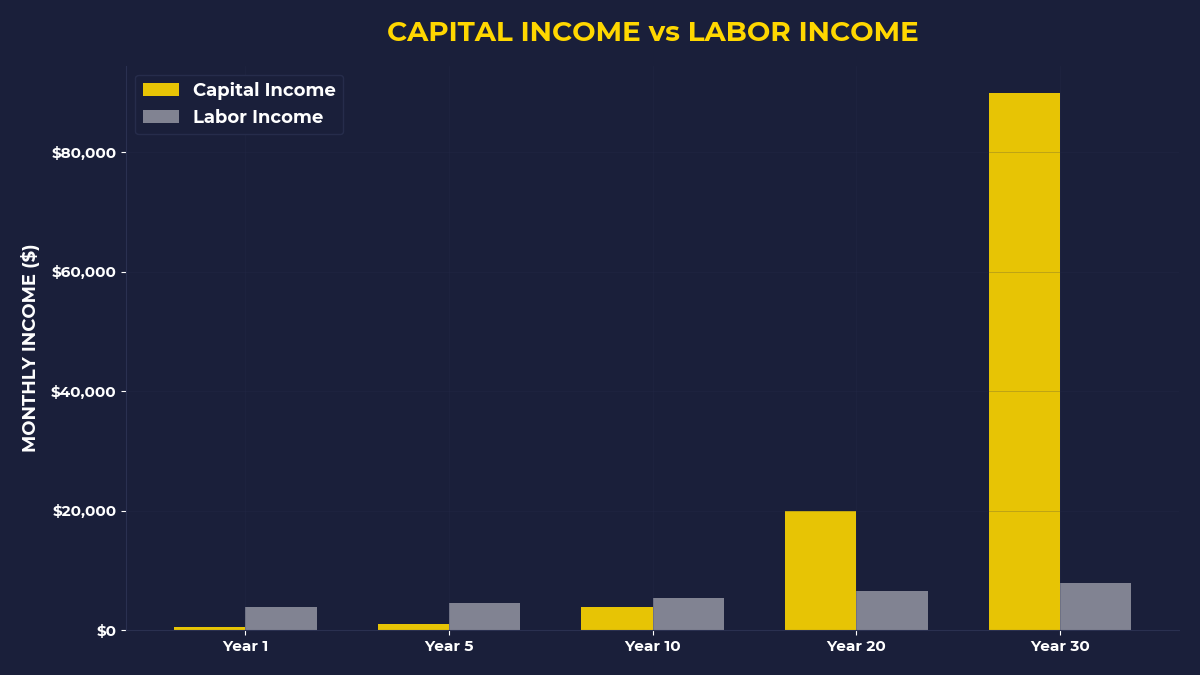

The Invoice Game You Never Signed Up For

Marcus — 29, software engineer in Denver — opened his banking app on a Tuesday morning and stared at something that made no sense. His $4,200 paycheck had hit his account on Friday. By Tuesday, he had $340 left.

Rent: $1,850 to his landlord’s LLC. Car payment: $420 to the bank. Insurance: $180 to the insurance company. Groceries: $320 to the supermarket chain. Netflix, Spotify, gym membership: another $85 to various corporations. Gas, utilities, phone bill: $290 more to different companies.

Marcus wasn’t reckless. He didn’t buy designer clothes or blow money on fancy dinners. He just paid his bills like every responsible adult.

That’s when it hit him: every single one of those payments went to someone who owned something he needed.

I Used to Think I Was Bad at Money

I know exactly how Marcus felt because I lived that same cycle for years. I’d get my paycheck, feel rich for about 48 hours, then watch it drain away like water through a sieve.

I used to think the problem was my spending habits. I’d try to budget, cut back on coffee, meal prep, use coupons. None of it worked. I’d save $50 here and $30 there, but the big chunks — rent, car payments, insurance — kept flowing out to the same places every month.

Here’s what I didn’t understand back then: I wasn’t bad at money. I was just playing the wrong game.

Every bill I paid was an invoice from a capital owner. My landlord owned the building I needed to live in. The bank owned the loan I needed for my car. The insurance company owned the policy I needed for protection. I was sending my labor — converted into dollars — directly to people who owned assets.

They had capital. I had a job.

The Capital Owner’s Daily Collection System

Walk through your typical day and count how many times you hand money to capital owners. Morning coffee: $4.50 to Starbucks shareholders. Gas for your car: $40 to oil company shareholders. Lunch: $12 to restaurant owners. Groceries after work: $35 to supermarket shareholders.

You’re not just buying coffee or gas. You’re paying dividends to people who own the systems that produce what you need.

Think about that for a second. Every time you swipe your card, scan your phone, or write a check, you’re transferring your labor-hours to someone else’s capital. Your 8-hour workday becomes their passive income.

The truly wild part? Most of these capital owners aren’t even actively working in these businesses anymore. They own shares, collect distributions, and use that money to buy more assets that generate more cash flow.

Meanwhile, you clock in Monday morning to earn the money that will flow to them by Thursday.

Are You Playing the Worker Game or the Owner Game?

Here’s the question that changed everything for me: Instead of asking “How can I make more money?” I started asking “What should I buy?”

Most people focus on the first question their entire lives. They get better at their jobs, ask for raises, switch companies for higher salaries. They’re optimizing their labor output.

But capital owners focus on the second question. They don’t ask how to work harder — they ask what assets to acquire that will generate demand from workers.

When I was 26, I had this realization while sitting in my apartment, looking at my rent check. I was about to hand $1,400 to my landlord — again. Same amount, same date, every single month. That’s $16,800 per year flowing from my labor to his capital.

Then I did the math that made me nauseous. If I stayed in that apartment for 5 years, I’d pay him $84,000. If I stayed 10 years, $168,000. All of that money would go toward building his wealth while my net worth stayed flat.

That’s when I understood: the game isn’t about earning more. It’s about switching sides.

The Warren Buffett Golf Ball Lesson Most People Miss

Warren Buffett used to find lost golf balls around Omaha golf courses when he was a kid. He’d clean them up and sell them back to golfers for 6 dollars per dozen. Simple business.

But here’s the part that separates workers from owners: Buffett could have spent his whole childhood personally collecting and cleaning golf balls. Instead, he used the money from golf ball sales to buy other assets — pinball machines, paper routes, eventually stocks and businesses.

He asked “What should I buy?” not “How can I work harder?”

Most people hear this story and think: “Well, I’m not Warren Buffett.” But you’re missing the point. The principle works at any scale. Every dollar you earn presents the same choice: send it to a capital owner, or use it to become one.

Your rent payment could become a house down payment. Your car payment could become an index fund contribution. Your streaming subscriptions could become dividend stock purchases.

Not overnight. Not without sacrifice. But the direction changes everything.

The One Invoice You Never Get

You know what invoice never shows up in your mailbox? A bill from your own assets.

Your checking account doesn’t send you money. Your emergency fund doesn’t pay you monthly distributions. Your 401k doesn’t cut you dividend checks (yet).

Meanwhile, every asset someone else owns sends you a bill. Their apartment building (your rent), their business (your purchases), their intellectual property (your subscriptions).

Look at your bank statement from last month. Count the outgoing payments. Now count the incoming payments that aren’t from your job.

That ratio — outgoing bills versus incoming asset payments — tells you exactly which side of the capital game you’re on.

The Contrarian Move That Feels Wrong But Works

Here’s what I started doing that felt completely backwards at the time: I paid myself first, even when I couldn’t afford it.

Before rent, before groceries, before anything else, I’d move money into investments. Even if it was just $50. Even if it meant I had to scramble to cover other expenses. Even if it meant eating ramen for a week or picking up extra work.

This goes against every piece of conventional financial advice you’ve ever heard. “Pay your bills first, then invest what’s left over.” But here’s the problem with that approach: there’s never anything left over.

Bills expand to consume available income. There’s always another expense, another emergency, another reason to delay building capital.

When I forced myself to invest first — to become a capital owner before paying other capital owners — something interesting happened. I found ways to cover my bills anyway. I worked a few extra hours. I found small savings I’d overlooked. I became more resourceful.

More importantly, I started receiving those other invoices. The ones that come from your own assets. Dividend payments. Interest. Capital gains. Small amounts at first, but they were flowing toward me instead of away from me.

The 2 AM Realization That Changes Everything

Six months into paying myself first, I had another 2 AM moment staring at my phone. But this time was different.

My portfolio had grown to $1,847. Not life-changing money, but something had shifted. For the first time in my adult life, I owned assets that were working while I slept. The companies in my index funds were generating revenue 24/7. Their employees were showing up to work, creating value, and a tiny fraction of that value was flowing to me.

I wasn’t just sending money to capital owners anymore. I was becoming one.

The amounts were small, but the direction had flipped. Instead of every dollar flowing away from me, some dollars were now flowing toward me. The compound effect hadn’t kicked in yet, but the machine was running.

If You’re Someone Who Feels Trapped by Bills

This post is for you if you’re tired of watching your paycheck disappear into other people’s assets. If you’re someone who works hard but never seems to get ahead. If you’re starting to realize that the problem isn’t your income — it’s that you don’t own anything that produces income.

You don’t need to quit your job or start a business (though you can). You don’t need a massive salary or a trust fund. You just need to start asking a different question.

Instead of “How can I afford all these bills?” ask “What can I buy that will send me bills?”

The One Thing to Remember

Every dollar you spend is a vote for the world you want to live in. When you send money to other people’s assets, you’re voting for a world where you stay a worker forever. When you buy assets that generate cash flow, you’re voting for your own financial freedom. The economy is designed to extract money from workers and deliver it to capital owners. The only way to stop being the worker in this equation is to become the owner.

Start today:

- Open a brokerage account and buy $25 worth of a broad market ETF before you pay any bills this month

- List your top 5 monthly expenses and research owning shares in those companies instead of just paying them

- Calculate how much money flowed out of your account to other people’s assets last month, then commit to redirecting 10% of that toward your own assets next month

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.