Marcus — 29, software engineer in Seattle — opened his investment app last Tuesday and saw something that made his stomach drop. His “diversified portfolio” had grown by $2,847 over eighteen months of careful, consistent investing.

His rent had gone up $4,200 in the same period.

Marcus had done everything right according to every finance blog he’d ever read. Dollar-cost averaging. Target-date funds. Index investing. He’d even rebalanced quarterly like the experts suggested. But sitting in his increasingly expensive apartment, watching his net worth crawl forward while his living costs sprinted ahead, Marcus asked the question that changes everything:

“What if my investment philosophy is designed to keep me poor?”

I Used to Be Marcus

I know exactly how Marcus felt because I spent three years building what I thought was wealth.

Back when I was 26, I had $18,000 spread across various index funds. I felt sophisticated. Responsible. I’d read all the right books, followed all the conventional wisdom. My portfolio was a beautiful, diversified rainbow of small losses and smaller gains.

Here’s the thing. I was doing exactly what Wall Street wanted me to do.

Every month, I dutifully sent my $600 to fund companies who used my money to buy stakes in the businesses that sent me bills every month. Netflix, Amazon, Apple, Google — companies that extracted hundreds of dollars from my checking account were getting hundreds more of my investment dollars.

I was funding both sides of my own financial prison.

The breakthrough came during a conversation with my landlord, Dave — a 54-year-old who owned seventeen rental properties across three cities. He wasn’t smarter than me. He definitely wasn’t more disciplined. But he understood something I didn’t.

“Investment philosophy,” Dave told me over coffee, “is just a fancy way of saying ‘who gets rich off my money?'”

That conversation rewired my brain.

The Question No One Asks

What if I told you that 97% of people have their investment philosophy completely backward?

Most people ask: “How can I get good returns on my money?”

Capital owners ask: “What can I buy that other people need every single day?”

The difference isn’t subtle. It’s the difference between working for money and making money work for you. Between hoping the market goes up and knowing that people need what you own.

Marcus discovered this the hard way. After that rent shock, he started tracking where his money actually went each month. Rent: $2,400. Groceries: $420. Netflix, Spotify, and other subscriptions: $67. Car payment: $340. Phone bill: $85. Insurance: $240.

Every single dollar flowed to someone who owned something Marcus needed.

His investment philosophy was making those same people richer twice — once through his bills, again through his portfolio. He was paying rent to his landlord while buying REIT shares. Buying groceries from Kroger while owning KR stock. Paying his phone bill to Verizon while holding VZ in his 401k.

The house always wins when you’re betting on both sides.

Capital Is Stored Demand

Let me tell you about my friend Sarah — 31, marketing director in Austin. Last year, she made a decision that sounded insane to everyone around her.

Instead of maxing out her 401k, Sarah took $15,000 and bought a duplex in a working-class neighborhood 20 minutes from downtown. The place needed work. Her friends called her crazy for “putting all her eggs in one basket.”

Here’s what happened next.

Sarah fixed up one side of the duplex and rented it out for $1,200 a month. She moved into the other side, cutting her own housing costs from $1,600 to zero. Net monthly impact: $2,800 in her favor.

But here’s the part that changed everything for Sarah: she realized she hadn’t just bought a building. She’d bought stored demand. People need housing every single month. The government can’t print more land. Her tenants can’t download shelter from the internet.

Sarah owned something people needed. Her investment philosophy shifted from hoping for returns to creating certainty.

Six months later, she used the positive cash flow to buy another small property. Then another. Today, she owns four rental units that generate $3,400 in monthly cash flow while her old coworkers are still dollar-cost averaging into index funds.

The conventional wisdom said Sarah was taking huge risks. The reality? She’d eliminated the biggest risk of all — depending on other people’s success for her own financial freedom.

Why Your Current Philosophy Keeps You Poor

Here’s the brutal truth about traditional investment philosophy: it’s designed to make you a permanent lender to people who already own everything.

When you buy stocks, you’re essentially saying: “I’ll give you my money now, and maybe you’ll give me some back later if your business does well.” You have zero control. Zero guarantee. You’re hoping that strangers make good decisions with your money.

Think about that. You work 40+ hours a week to earn money, then hand it over to people you’ve never met, betting they’ll use it better than you could.

Meanwhile, those same people are using your investment dollars to buy the assets that extract money from your checking account every month. Your investment returns are literally funding the costs that keep you paycheck-to-paycheck.

It’s not a market. It’s a machine. And you’re not the customer — you’re the product.

Real capital owners think differently. They don’t ask “What should I invest in?” They ask “What do people need that I can own?”

Warren Buffett didn’t get rich by buying index funds. He bought Coca-Cola because people drink Coke every day. He bought railroads because stuff needs to move. He bought insurance companies because people need protection.

He bought demand. Then he sat back and collected his cut of every transaction.

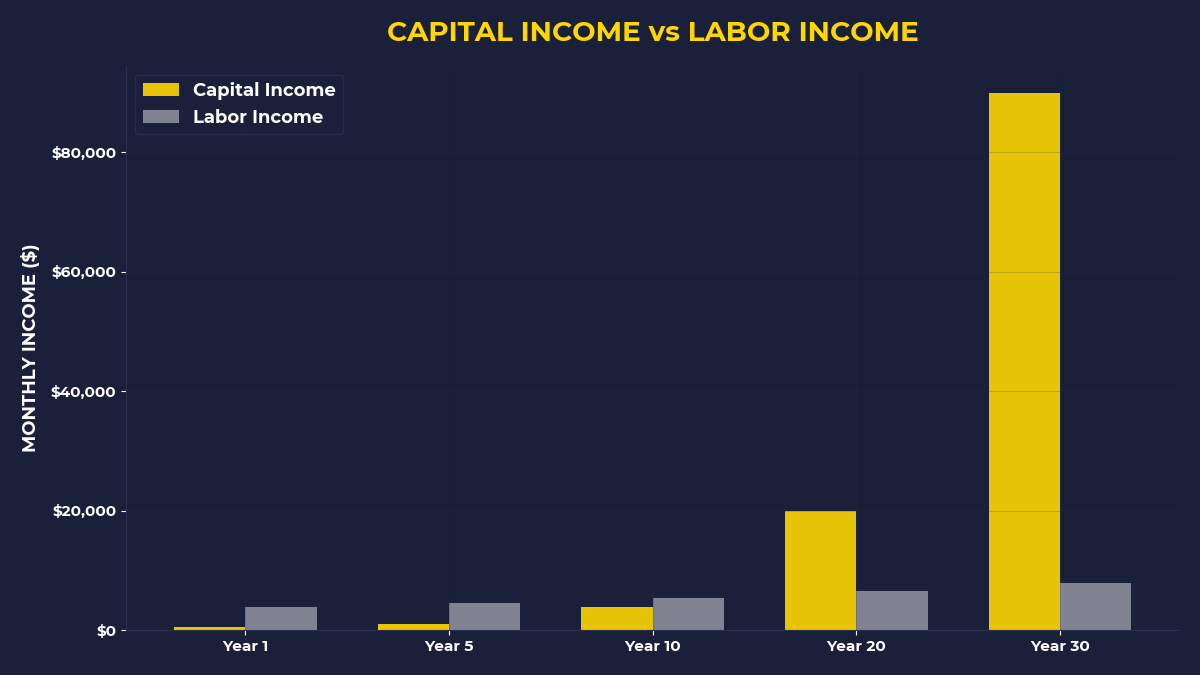

The Philosophy That Actually Builds Wealth

Let me show you what an ownership-first investment philosophy looks like in practice.

Remember Marcus? After his rent shock, he completely flipped his approach. Instead of sending $600 a month to index funds, he started asking: “What can I buy that pays me back faster than it costs me?”

His first purchase: a laundromat in a working-class neighborhood for $45,000. Not glamorous. But people need clean clothes every week. The machine doesn’t care about market sentiment or Federal Reserve policy. People put in quarters, clothes come out clean, Marcus gets paid.

Monthly cash flow after expenses: $1,200.

His second purchase: three vending machines placed in office buildings. Cost: $8,000 total. Monthly profit: $400.

His third move: he started a small pressure-washing business. Invested $3,500 in equipment, spends Saturdays cleaning driveways and decks. Monthly profit: $800.

Total monthly passive income: $2,400.

Marcus didn’t become a business genius overnight. He just stopped giving his money to people who were already rich and started buying things that generated cash flow.

The difference in philosophy: instead of hoping for 7% annual returns, Marcus created 15-20% monthly returns on assets he controlled completely.

Your Emergency Fund Is Your Biggest Mistake

Here’s where conventional investment philosophy does the most damage: it teaches you to hold cash “for emergencies.”

Let me be direct: your emergency fund is an anti-wealth machine.

While you’re sitting on $10,000 earning 0.5% in your savings account, inflation is eating 3-4% of its value every year. You’re guaranteed to lose money. Meanwhile, that same $10,000 could be the down payment on a rental property generating $200+ monthly cash flow.

“But what about emergencies?” you ask.

Here’s what capital owners know: cash flow is the best emergency fund. If you own assets that generate monthly income, you can handle temporary disruptions without touching your principal. If you lose your job, your rental properties still collect rent. Your vending machines still dispense snacks. Your laundromat still washes clothes.

Diversification through cash flow is real security. Diversification through different stock sectors is just sophisticated poverty.

The One Question That Changes Everything

If you’re someone who’s tired of watching your investment portfolio move sideways while your bills move up, you need to change one fundamental question.

Stop asking: “How can I get better returns?”

Start asking: “What can I buy that people need to pay for every month?”

This isn’t about becoming a business mogul or quitting your job. It’s about redirecting your investment philosophy toward ownership instead of speculation.

Maybe that’s a small duplex. Maybe it’s a profitable blog. Maybe it’s equipment you can rent out. Maybe it’s a simple business you can run on weekends.

The point isn’t the specific asset. The point is the mindset shift: from hoping other people make you rich to creating systems that make you rich regardless of what other people do.

Your current investment philosophy is someone else’s wealth plan. The question is: when will you start building your own?

• This month, track every bill you pay and identify which public companies receive your money. Then ask: what would happen if you owned those companies instead of just supporting them?

• Before you make your next investment contribution, research one cash-flowing asset you could buy instead. Even if you don’t buy it, understand the difference between hoping for returns and creating them.

• Calculate how much money you’ve sent to investment accounts over the past year, then imagine what monthly cash flow you could have generated with that same amount invested in assets you control.

🎬 Prefer watching? Check out the video version on YouTube: