Sarah — 29, marketing coordinator in Denver — opened her banking app at 7:23 AM on the first of March. Her paycheck had hit overnight. $3,847 after taxes.

By 7:31 AM, she’d scheduled eight payments that would drain $3,200 before lunch.

Rent to her landlord’s property management company. Car payment to the bank. Student loans to Navient. Phone bill to Verizon. Groceries on her credit card, which flows to Chase. Netflix, Spotify, gym membership. Even her morning coffee — $4.50 to the local chain that’s actually owned by a private equity firm in New York.

Sarah stared at her remaining balance: $647 for the next 29 days.

She’d just sent 83% of her income to capital owners before breakfast.

Here’s What Nobody Tells You About Your Monthly Bills

I know exactly how Sarah felt because I lived that exact morning for seven years straight. Same routine, different amounts. Paycheck arrives, money vanishes to landlords and lenders, I’m left managing the scraps.

But here’s what I didn’t understand then: those weren’t just bills. They were wealth transfer invoices.

Every month, I was funding other people’s retirements while wondering why I couldn’t save for my own. I was paying rent to someone who owned the building I lived in. Making car payments that built equity for a bank’s loan portfolio. Sending student loan payments that generated returns for bond investors.

I was the revenue stream in everyone else’s capital equation.

The moment this hit me — really hit me — was sitting in my studio apartment at 11 PM, watching my landlord’s Tesla pull into the parking garage downstairs. He owned four buildings in my neighborhood. I was helping him buy his fifth.

Capital Isn’t Money (It’s Stored Demand)

Most people think capital means having money in the bank.

Wrong.

Capital is owning something that people need repeatedly. It’s stored demand that generates cash flow without your direct labor. Your landlord doesn’t work 40 hours a week to collect your rent check. The bank doesn’t clock in daily to receive your car payment. Netflix doesn’t personally entertain you for $15.99 per month.

They own systems that capture recurring demand.

Think about Warren Buffett as a kid, selling golf balls he found in the woods near country clubs. Smart move, right? But here’s the part that matters: if young Warren had hired friends to collect the balls while he focused on sales and distribution, he would have built capital. The system works without him.

That’s the difference between working for money and owning capital that works for you.

Sarah’s landlord figured this out. He bought buildings when demand for housing was predictable. Now thousands of people like Sarah send him checks every month, whether he’s awake or asleep, sick or healthy, working or on vacation.

Sarah, meanwhile, trades her time for dollars that immediately flow to capital owners.

Why Your Brain Tricks You Into Staying On The Wrong Side

Here’s the psychological trap that keeps 97% of people funding other people’s wealth: we’re trained to pay everyone else first.

Rent is due on the 1st. Car payment on the 5th. Credit cards by the 15th. We structure our entire financial lives around sending money to capital owners on their schedule, then try to build wealth with whatever’s left.

This is backwards.

I learned this lesson the hard way when I was 26, living paycheck to paycheck despite making decent money. I kept telling myself I’d invest once I had my expenses “under control.” But expenses expand to fill available income. There’s always another bill, another subscription, another reason to delay.

The breakthrough came when I read about Robert Kiyosaki living in a friend’s garage while building his business. Even when facing eviction, he paid himself first. Before rent. Before utilities. Before food.

He bought assets with the first dollars he earned, then scrambled to cover bills with what remained.

Sounds crazy, right? But here’s what happened: the pressure to cover his bills forced him to find additional income streams. He worked nights and weekends to pay rent. But his asset purchases during the day were building his escape route.

The Question That Changes Everything

Want to know the real difference between people who build wealth and people who stay broke?

Poor people ask: “What should I do to make more money?”

Rich people ask: “What should I buy to make money while I sleep?”

This shift in thinking changes everything. Instead of trying to work more hours or get a better job, you start looking for assets that generate recurring cash flow. Instead of optimizing your labor, you optimize your ownership.

Sarah could work 60-hour weeks and maybe bump her income to $4,500 per month. But she’d still be trading time for money. Still sending 80% of her paycheck to other people’s investment portfolios.

Or she could start asking different questions:

“What if I bought a duplex and lived in one unit while renting out the other?”

“What if I bought dividend-paying stocks instead of paying down my car loan early?”

“What if I started a side business that generates recurring revenue instead of overtime pay?”

These aren’t just different strategies. They’re different mindsets. One builds wealth for someone else. The other builds wealth for you.

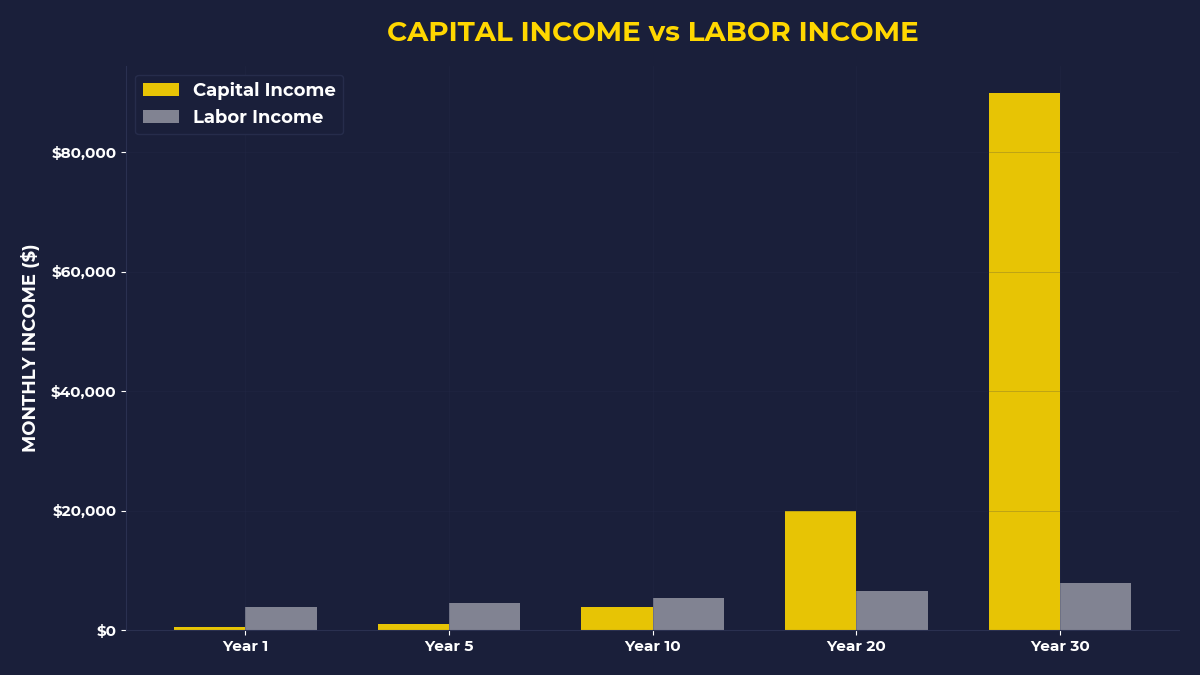

The Compound Effect Of Ownership Versus Labor

Here’s the math that nobody teaches in school:

Workers add. Owners multiply.

When you work harder, you earn more money linearly. Work 20% more hours, earn roughly 20% more pay. But when you own assets, the math changes completely.

Let me give you a real example. My friend Marcus — 31, software engineer — was making $95,000 per year in 2019. Instead of upgrading his lifestyle, he bought a small rental property for $120,000 with 20% down. Monthly rent: $1,200. His mortgage and expenses: $900.

Net cash flow: $300 per month.

Not life-changing money. But here’s what happened over four years: his tenant paid down $18,000 of his mortgage principal while the property value increased to $165,000. Plus he collected $14,400 in cash flow.

Total return on his $24,000 investment: $63,400.

That’s a 264% return while he slept, traveled, and worked his regular job. His tenant — who pays rent instead of owning — helped Marcus build $63,400 in wealth while building zero for themselves.

This is the power of capital. It compounds. It works while you sleep. It turns other people’s monthly payments into your monthly income.

If You’re Tired Of Funding Other People’s Dreams

This post isn’t for everyone. If you’re comfortable sending 80% of your income to landlords and lenders for the next 30 years, keep doing what you’re doing.

But if you’re tired of watching your paycheck vanish to other people’s investment accounts, if you want to switch from sending checks to receiving them, if you’re ready to stop working for capital and start owning it — then you need to flip the script.

The hardest part isn’t finding good investments. It’s breaking the psychological pattern that says everyone else gets paid before you do.

Start small. Start imperfect. But start.

The One Thing To Remember

Every dollar you send to a capital owner is a dollar that could have been working for you instead. Your rent check isn’t just housing expense — it’s equity building for someone else. Your car payment isn’t just transportation — it’s returns for a bank’s shareholders. The question isn’t whether you’ll pay these bills. The question is whether you’ll also start collecting them.

Here’s what to do this month:

• Before you pay any bill, transfer $50 to a brokerage account and buy shares of an S&P 500 ETF

• Calculate exactly how much of your monthly income goes to capital owners (rent, loans, subscriptions) — the number will shock you

• Ask yourself: “What could I buy this month that would pay me back next month?” Start there

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.