Marcus — 29, software engineer in Denver — made $87,000 last year but still lived paycheck to paycheck. Not because he was reckless. Because every time he got ahead, his brain found a way to sabotage him.

Last March, he’d saved $3,200. First time in years he had breathing room. Two weeks later, his car started making a noise. Not dying. Just a noise. But Marcus’s brain whispered the same story it always did: “Better fix it now before it gets worse.” $2,400 later, he was back to zero.

The mechanic told him afterward the noise was cosmetic. Nothing dangerous. Nothing urgent. Just his brain, doing what brains do — keeping him poor.

I Know This Dance Because I’ve Done It

I spent seven years making the same mistake Marcus made. Different details, same pattern.

Every time I accumulated a few thousand dollars, my Stone Age brain would find a reason to spend it. Emergency car repair that wasn’t an emergency. “Investment” in a course that taught me nothing new. Vacation I “deserved” after working so hard.

Here’s what I didn’t understand then: **Your brain is hardwired to keep you poor.**

Not out of malice. Out of 200,000 years of evolution that taught your ancestors one lesson above all others: spend resources immediately or lose them forever. Store grain, and raiders take it. Save meat, and it rots. Use everything now or watch it disappear.

That programming served our ancestors well. It’s destroying your financial future.

Why Your Brain Sabotages Every Smart Money Decision

Behavioral finance researchers have identified over 150 cognitive biases that affect money decisions. But three dominate everything:

**Present bias** — your brain values immediate rewards roughly 2.5 times more than future rewards of equal size. That’s why $100 today feels better than $250 next year, even though the math is obvious.

**Loss aversion** — your brain treats losing $100 as twice as painful as gaining $100 feels good. So you avoid any investment that might go down, even temporarily. Even when staying in cash guarantees you lose to inflation.

**Mental accounting** — your brain creates separate mental buckets for different money sources. Tax refund money feels “free” to spend on vacation. Overtime money feels earned and serious. Same dollars, different treatment.

Think about Marcus. His present bias made him want to fix the car immediately instead of waiting to see if the noise worsened. His loss aversion made him terrified of ignoring a potential problem. His mental accounting made his savings feel like “emergency money” that existed to be spent on emergencies — real or imagined.

Every decision felt rational in the moment. Every decision kept him poor.

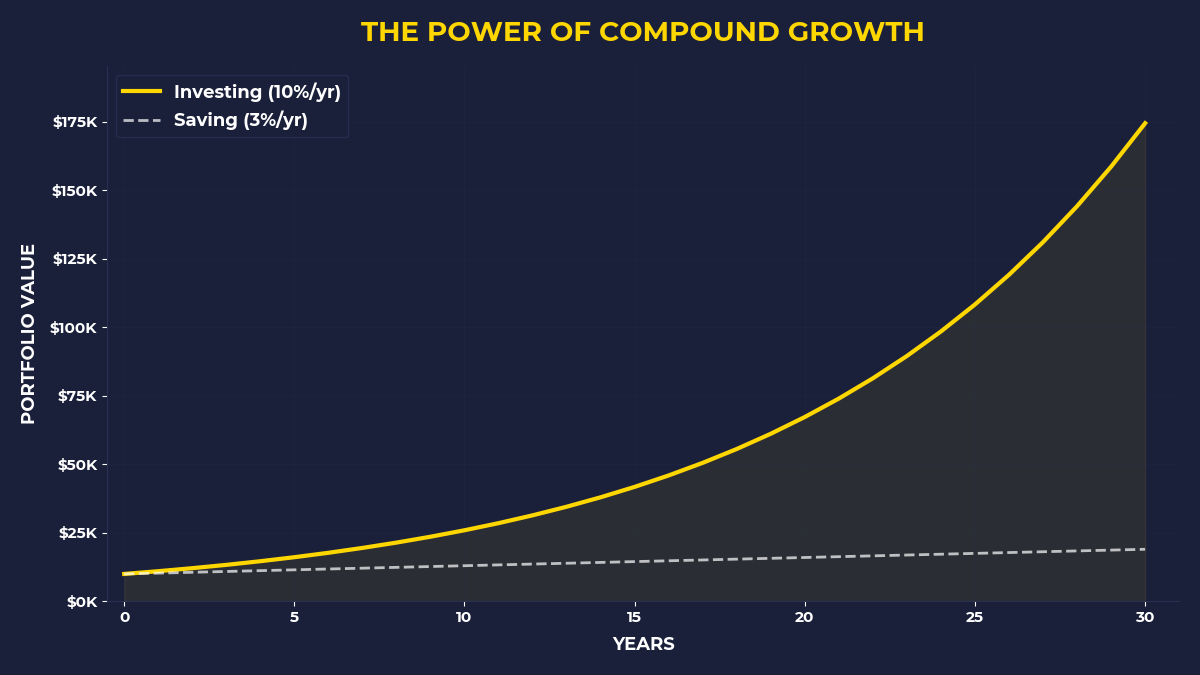

The $47,000 Difference

Want to see how this plays out over time?

Take two 25-year-olds, both earning $50,000. Sarah fights her brain and invests $200 monthly in index funds earning 7% annually. Mike follows his brain and spends that $200 on “necessary” things that feel urgent.

By age 65, Sarah has $525,000. Mike has whatever’s left in checking.

Same intelligence. Same income. One learned to outsmart her Stone Age programming. The other didn’t.

But here’s what really matters: Sarah’s money worked while she slept. Mike traded every dollar for hours of his life. Sarah bought her time back. Mike sold his time away, forever.

Why Rich People’s Brains Work Differently

Do wealthy people have different brains? Not exactly. They’ve learned to work with their brain’s quirks instead of against them.

I learned this from my friend Jennifer, who inherited $180,000 at 26. She could have blown it on a house downpayment or a business idea or “experiences.” Instead, she did something that seemed insane at the time.

She automated everything.

First day after the inheritance cleared, she set up automatic transfers. $1,500 monthly into index funds. $500 into individual stocks. $300 into REITs. Then she forgot about it.

Three years later, I asked how she resisted the urge to touch the money during the 2020 crash. Her answer floored me: “What money? I automated it and never looked at the accounts.”

She’d hacked her present bias by removing present decisions. She’d avoided loss aversion by not watching daily fluctuations. She’d eliminated mental accounting by treating investment money as gone before she could spend it.

Ten years later, that $180,000 is worth $380,000. More importantly, it generates $1,200 monthly in dividends. Money she never worked for. Capital that works while she sleeps.

The One Decision That Changes Everything

Here’s what separates capital owners from everyone else: **They pay themselves before they pay anyone else.**

Not after rent. Not after groceries. Not after the car payment or student loans or credit cards. Before.

Your brain will resist this like poison. It will create emergencies. It will find urgent expenses. It will whisper that you can’t afford to invest until you handle the immediate crisis.

That whisper is your 200,000-year-old programming keeping you poor.

I broke free by following Robert Kiyosaki’s advice from those late-night hours in my friend’s garage: pay yourself first, then scramble to cover the bills. Even if it means eating ramen. Even if it means working extra hours. Even if it feels impossible.

Especially then.

The discomfort you feel? That’s your brain rewiring itself. That’s the exact sensation of becoming a capital owner instead of staying a capital renter.

Your Brain vs. Your Bank Account

Every month, you make hundreds of small decisions that either build capital or destroy it. Buy the fancy coffee or invest the $4. Upgrade your phone or put $200 toward index funds. Take the Uber or walk and invest the $12.

Your brain votes for comfort every time. Capital votes for compound growth.

The winner depends on which one you listen to more often.

Marcus figured this out the hard way. After the unnecessary car repair, he realized his brain was his biggest financial enemy. He started small: $50 automatically transferred to investments every payday, before he could think about it.

Six months later, he’d accumulated $320 without feeling it. His brain stopped fighting because it never had a chance to spend the money. It was gone before the ancient programming could kick in.

If You Work Hard and Stay Poor, This Is Why

You’re probably not lazy. You’re not stupid. You’re not financially irresponsible.

You’re running Stone Age software on modern money problems.

Your brain was designed for a world where storing resources was dangerous and spending them immediately was survival. In that world, your programming worked perfectly.

In this world, it keeps you poor while others get rich.

The One Thing To Remember

**Your brain will always find reasons to spend instead of invest. Rich people don’t fight this urge — they automate around it.** They remove decision-making from daily money choices. They pay themselves first and force their brain to solve for the remaining bills. They turn investing from a decision into a system that runs whether they feel like it or not.

Start here:

Set up automatic transfer of $50-200 to a brokerage account on payday, before you pay any other bills

Buy broad market index funds (VTI, VOO, or similar) with that money automatically

Never check the balance for the first 90 days — let your brain forget the money exists

🎬 Prefer watching? Check out the video version on YouTube: