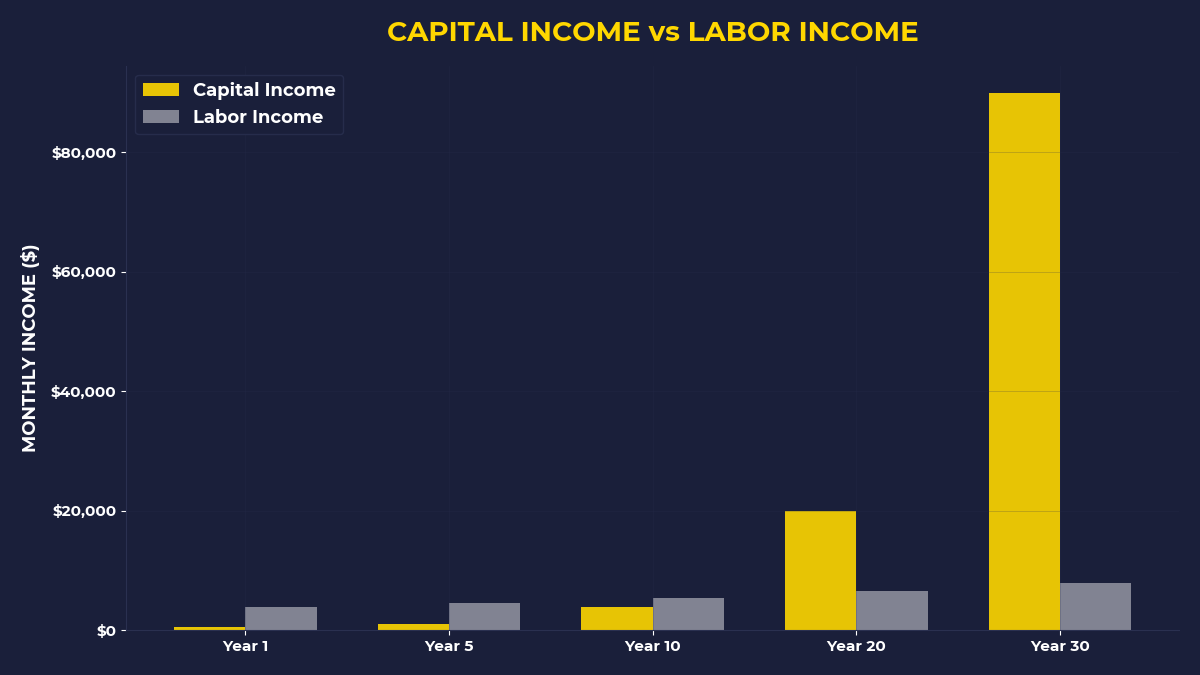

The Paradox of Smart People Making Dumb Money Decisions

I know a software engineer who makes $180,000 a year and lives paycheck to paycheck. Not because he spends wildly—he drives a 2018 Honda and makes coffee at home. He’s drowning because every month, his brain makes the same three decisions that guarantee he’ll never own capital.

First, he pays everyone else before paying himself. Rent to the landlord, car payment to the bank, groceries to the supermarket chain shareholders. Then, if anything’s left, maybe he invests it.

Second, when markets drop 15%, he sells. When they rally 20%, he buys back in. His primitive brain treats volatility like a saber-tooth tiger.

Third, he optimizes for comfort over ownership. Emergency fund fully stocked, 401k getting its match, savings account earning 0.5%. He’s built a fortress around his poverty.

Here’s what blew my mind when I finally understood behavioral finance: it’s not about stock picking or market timing. It’s about recognizing that your brain is running 50,000-year-old software in a capital market that rewards the exact opposite of what kept your ancestors alive.

Why I Used to Think Behavioral Finance Was Academic Nonsense

I used to roll my eyes at behavioral finance. Seemed like professors trying to explain why regular people weren’t as smart as efficient market theory assumed they should be.

Then I lost $23,000 in six weeks during March 2020.

Not because I picked bad stocks. I panicked. The S&P 500 dropped 34% between February 19 and March 23, 2020, and every primitive circuit in my brain screamed “SURVIVAL THREAT.” I sold everything on March 18th, right before one of the greatest rallies in market history.

That’s when I realized behavioral finance isn’t academic theory—it’s combat psychology. Your brain doesn’t distinguish between a market crash and a predator attack. Both trigger the same ancient systems designed to keep you alive, not wealthy.

The problem isn’t your intelligence. It’s your wiring.

The Three Primitive Instincts That Destroy Capital

Every financial mistake you’ve ever made traces back to one of three survival instincts that evolution burned into your neural pathways.

Loss Aversion: The Sabertooth Response

Your ancestors who lost their food cache died. So your brain treats any loss—even a temporary paper loss in your portfolio—like a mortal threat. Studies show people feel losses twice as intensely as equivalent gains. When your $50,000 portfolio drops to $45,000, your amygdala fires like you just lost half your winter food supply.

This is why 89% of active traders lose money over ten-year periods. They sell when it hurts and buy when it feels safe. Pain avoidance trumps wealth building every time.

Recency Bias: The Pattern Trap

If berries from a certain bush made your tribe sick yesterday, you avoided that bush forever. Smart survival strategy. Terrible investment strategy.

Your brain assumes recent events predict future events. Tech stocks crashed in 2000? Avoid tech forever. Housing imploded in 2008? Real estate is dangerous. Bitcoin dropped 80% in 2022? Crypto is dead.

Meanwhile, the data tells a different story. The NASDAQ gained 537% from its 2000 low to 2021. Housing recovered every penny lost in 2008 by 2012. But recency bias keeps you fighting the last war while missing the next opportunity.

Herd Mentality: The Safety-in-Numbers Delusion

Being alone on the savanna meant death. Being wrong with the tribe meant survival. So when everyone around you is buying GameStop at $300 or selling everything in March 2020, every social instinct screams “follow the crowd.”

Think about that. The behavior that kept humans alive for millennia is exactly what keeps you poor in capital markets.

What Does Your Brain Do When Markets Move?

Let me show you how this plays out in real time. It’s January 2022. Tech stocks are getting hammered. Netflix drops 35% in one day. Your brain doesn’t see a company with 221 million subscribers trading at a discount.

It sees danger.

Your amygdala hijacks your prefrontal cortex. Suddenly, you’re not thinking about Netflix’s competitive moat or cash generation. You’re thinking: “What if this keeps falling? What if I lose everything? What if I should have sold yesterday?”

So you sell. At exactly the wrong time.

Six months later, when Netflix recovers 40%, you don’t buy. Why? Because now your brain sees a “risky” stock that “might crash again.” The same pattern-matching system that saved your ancestors from poisonous berries keeps you out of quality assets at reasonable prices.

Your primitive brain optimizes for not dying. Capital markets reward optimizing for asymmetric upside.

The Emergency Fund Trap Most Investors Never Escape

Here’s where behavioral finance gets personal. That emergency fund you’re so proud of? It’s probably keeping you poor.

Not because emergency funds are bad—because of what they represent. Your brain categorizes money into “safe” and “risky” buckets. Safe money sits in savings accounts earning 2%. Risky money goes into “the market.”

But here’s the behavioral trap: once you build a six-month emergency fund, your brain relaxes. You’ve solved the survival problem. Now you can take “risks” with your “extra” money.

Except there’s never extra money. There’s always another bill, another expense, another reason to keep cash “safe.”

I know people with $50,000 emergency funds and $5,000 investment accounts. They’ve optimized for surviving a job loss they probably won’t face while guaranteeing they’ll never build capital.

The primitive brain wins again.

Why You Keep Paying Everyone Else Before Yourself

Every month, the same ritual. Landlord gets paid. Car payment clears. Credit card minimums, insurance, utilities, groceries. Then, if there’s anything left, maybe you invest it.

This isn’t budgeting—it’s behavioral programming.

Your brain treats immediate obligations as survival threats. Skip the rent, lose shelter. Miss the car payment, lose transportation. These feel urgent because your ancestors who ignored immediate needs died.

But wealth building feels abstract. Investing $500 this month doesn’t trigger any survival circuits. Your brain literally cannot perceive the urgency of buying assets because there’s no immediate threat to address.

Meanwhile, every dollar you spend is a dollar flowing to someone who owns capital. Your rent check goes to a property owner. Your car payment goes to a bank’s shareholders. Your grocery bill goes to Walmart’s investors.

You’re not just failing to build wealth—you’re actively transferring it to people who figured out how to own assets instead of just using them.

The One Question That Breaks Primitive Money Programming

After I lost that $23,000 in 2020, I started asking a different question every time I felt the urge to make a financial decision based on fear or comfort.

“What would I do if I were already wealthy?”

Wealthy people don’t hoard cash because they’re afraid of volatility. They buy more assets when prices drop. They don’t pay everyone else first—they pay themselves first, then figure out the rest.

They don’t avoid risk—they understand that not owning capital is the biggest risk of all.

When Netflix dropped 35% in January 2022, my primitive brain wanted to sell everything. But I asked the question: “What would I do if I were already wealthy?”

A wealthy person would see a company with 221 million subscribers, massive cash flow, and global distribution trading at a discount. They’d buy more.

So I bought more.

Netflix gained 64% over the next eighteen months. My primitive brain would have cost me that entire return.

What The Primal Investor Takes Away

• **Name the instinct before it names you**: When you feel the urge to sell during volatility, ask “Is this loss aversion or actual analysis?” When everyone’s buying something, ask “Is this herd mentality or genuine opportunity?”

• **Pay yourself before you pay bills**: Invest first, then solve the cash flow problem. Your brain will find a way to cover expenses—it always does. But it will never prioritize wealth building unless you force it.

• **Turn emergency funds into opportunity funds**: Keep 2-3 months of expenses liquid, not six. Use the difference to buy quality assets when your primitive brain is screaming danger.

• **Ask the wealthy person question**: Before any major financial decision, ask “What would I do if I were already wealthy?” Their behavior reveals what actually builds capital versus what just feels safe.

• **Recognize that avoiding losses guarantees staying poor**: Your brain’s primary job is keeping you alive, not making you wealthy. Those are often opposing objectives in capital markets.

Your brain isn’t broken—it’s just running the wrong program for building wealth. Once you recognize that every financial instinct you have is designed for a world that no longer exists, you can finally start making decisions that lead to capital instead of just comfort.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.