The Question That Separates Capital Owners From Everyone Else

Most people spend their entire lives asking “What should I do to make money?” Capital owners ask something completely different: “What should I buy?”

That single question — what to buy instead of what to do — explains why 3% of Americans own 70% of the wealth while everyone else trades hours for dollars until they die. It’s why Warren Buffett became worth $118 billion while millions of harder-working people struggle to pay rent. And it’s why your smartest, most dedicated friends often stay broke despite doing everything “right.”

I used to be obsessed with the first question. When I was 28, fresh out of graduate school, I had this brilliant plan: I’d work harder, learn more skills, network better, optimize my resume, and somehow climb my way to financial freedom. I read every productivity book, took every course, followed every guru’s morning routine.

The result? I got really, really good at making other people rich.

Why Hard Work Without Capital Is Just Expensive Labor

Here’s what nobody tells you about the “work harder” approach to wealth: it’s fundamentally designed to transfer your energy to capital owners. Every productivity hack you learn, every skill you develop, every extra hour you put in — it all flows upward to people who own equity while you rent your time.

Look at your last paycheck stub. How much of your gross income actually lands in your account after taxes, insurance, 401k contributions, and other deductions? For most Americans, it’s about 65-70% of the headline number. Then look at where that remaining money goes: rent or mortgage (to property owners), car payments (to banks), groceries (to retail and food conglomerates), utilities (to infrastructure owners), streaming services (to media companies).

You’re not building wealth. You’re paying dividends to people who asked a different question than you did.

The primitive instinct driving this pattern is what I call “effort bias” — the hardwired belief that more effort equals better outcomes. Our ancestors survived by working harder when resources were scarce. But in a capital-based economy, effort without ownership is just another person’s profit center.

Think about the most successful people you know personally. I’m willing to bet they’re not the ones working 80-hour weeks. They’re the ones who figured out how to buy something that works for them.

What Warren Buffett Learned Selling Golf Balls at Age 13

When Warren Buffett was 13 years old, he discovered used golf balls around local courses and sold them for $6 per dozen. But here’s the part most people miss: Buffett didn’t just work harder to find more golf balls. He took the money from those sales and bought assets — a pinball machine for a barber shop, then farmland, then more businesses.

By age 16, Buffett had $53,000 (about $600,000 in today’s dollars) not because he worked harder than other teenagers, but because he kept asking “What should I buy?” instead of “What should I do?”

Every dollar he earned went back into purchasing things that generated cash flow without his direct labor. The golf ball money bought the pinball machine. The pinball machine profits bought more pinball machines. The expanded pinball business funded his first real estate investment. Each purchase created leverage — other people’s time and effort working on his behalf.

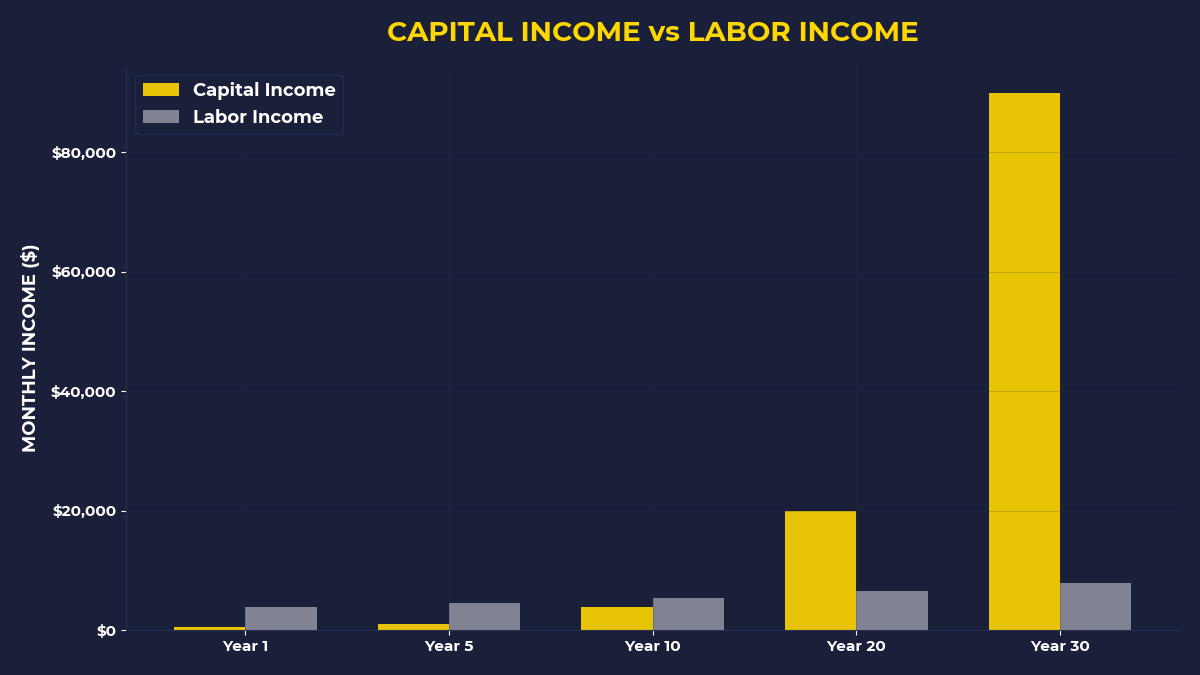

This is compound capital acquisition, not compound interest. The difference matters.

Why Your Monthly Bills Are Invoices From Capital Owners

Let me be honest about something that took me years to understand: every recurring expense in your life represents someone else’s recurring income.

Your rent check? That’s a monthly dividend payment to someone who owns real estate. Your car payment? That’s interest income for a bank that owns loan assets. Your Netflix subscription? That’s recurring revenue for shareholders who own media capital. Even your morning coffee represents cash flow to people who own coffee shops, supply chains, and equipment leasing companies.

I calculated this for my own spending in 2019. Of the $4,200 I spent per month on living expenses, roughly $3,800 went directly to capital owners as dividends, interest, rent, or business profits. Only $400 went to direct labor (tips, personal services, etc.).

That ratio — 90% to capital, 10% to labor — is not accidental. It’s the natural structure of a developed economy. And it reveals why people who only sell their labor stay poor while people who own capital get rich.

The system isn’t broken. You’re just on the wrong side of it.

The Compound Capital Strategy That Changes Everything

Here’s the strategy that completely shifted my relationship with money: pay yourself first, but not into savings — into assets that generate demand.

Robert Kiyosaki tells a story in “Rich Dad Poor Dad” about living in a friend’s garage after his business failed. Despite facing eviction notices and angry creditors, Kiyosaki had one unbreakable rule: every dollar of income went to buying assets first, paying bills second. When he ran short on bill money, he worked extra jobs to cover the gap.

This sounds insane until you understand the psychology. When you pay bills first, you train your brain to see assets as optional — something you’ll buy “when you have extra money.” When you buy assets first, you train your brain to see bills as problems that require creative solutions.

Guess which mindset creates more wealth?

I started applying this in 2020. Every paycheck, 25% went straight to purchasing equity — individual stocks, index funds, REITs, whatever I could get ownership stakes in. Then I lived on the remaining 75% and figured out how to make ends meet. Some months I drove for Uber to cover the gap. Some months I freelance consulted. Some months I ate a lot of rice and beans.

But I never touched the asset purchases. Ever.

By 2024, my investment portfolio generates about $1,800 per month in dividends and distributions. That’s $1,800 per month I don’t have to work for. It’s $1,800 per month that other people’s labor creates for me because I own pieces of their productivity.

Why “What Should I Buy?” Beats “What Should I Do?” Every Time

The fundamental difference between these questions is leverage. When you ask “What should I do?” you’re looking for ways to trade more of your time and energy for money. When you ask “What should I buy?” you’re looking for ways to trade money for other people’s time and energy.

Consider two approaches to increasing your income by $1,000 per month:

The “What Should I Do?” Approach: Get a side hustle, work weekends, learn new skills, ask for a promotion, optimize your schedule, network more aggressively. All of these require ongoing effort from you personally.

The “What Should I Buy?” Approach: Purchase $300,000 worth of dividend-paying stocks yielding 4% annually. Or buy a rental property that cash flows $1,000/month after expenses. Or acquire a small business generating $1,000/month in owner earnings.

Same result. Completely different sustainability.

The first approach caps out when you run out of hours in the day or energy in your body. The second approach scales through compound acquisition — using cash flow from existing assets to buy more assets.

The One Mental Model That Creates Generational Wealth

Here’s the mental model that changed everything for me: capital is stored demand, not stored money.

When you buy shares of Apple, you’re not buying pieces of paper or digital entries in a brokerage account. You’re buying tiny fractions of the world’s ongoing demand for smartphones, computers, and digital services. When you buy real estate, you’re buying stored demand for shelter and location. When you buy a business, you’re buying stored demand for whatever problem that business solves.

This reframe completely changes how you think about asset selection. Instead of asking “Will this stock go up?” you ask “Will people still want this product or service in 20 years?” Instead of asking “What’s the ROI?” you ask “How durable is the underlying demand?”

Amazon stock has returned 12,300% since its IPO in 1997 not because Jeff Bezos worked harder than other CEOs, but because Amazon successfully captured and monetized humanity’s permanent demand for convenience in commerce.

Demand is the engine. Everything else is just engineering.

What The Primal Investor Takes Away

• Stop optimizing your productivity. Start optimizing your capital acquisition rate. Every dollar you earn should face the question: does this buy me ownership or does this buy me consumption?

• Treat monthly bills as invoices from your future self. Every recurring expense should make you ask: how can I own the thing sending me this bill instead of just paying it?

• Flip the payment priority: assets first, bills second. Train your brain to see capital acquisition as mandatory and lifestyle expenses as optional.

• Think in terms of stored demand, not stored money. Buy stakes in things people will still want in 20 years, not things that are popular today.

• Ask “What should I buy?” instead of “What should I do?” at least once per day. This single question will rewire your relationship with money faster than any other mental habit.

The sophisticated investor understands that in a capital-driven economy, the question you ask determines the life you get. Workers ask what they should do. Owners ask what they should buy.

🎬 Prefer watching? Check out the video version on YouTube:

")