Marcus — 29, software engineer in Denver — called me last Thursday around 11 PM. His voice had that exhausted edge I recognized immediately. “I’m making $95,000 a year,” he said. “I follow every personal finance rule. Emergency fund, 401k, the whole thing. But I’m still broke by the 20th of every month.”

I know exactly how Marcus felt.

The Question Everyone Gets Wrong

Three years ago, I was sitting in my apartment at midnight, staring at my bank balance: $847. I’d just gotten a promotion. I was making more money than I’d ever made. And I was more financially stressed than I’d been since college.

That’s when I realized something that changed everything about how I think about money.

Most people — 97% of people — spend their entire lives asking the wrong question about wealth. They ask: “What should I do to make more money?” Capital owners ask: “What should I buy?”

The difference between those two questions is the difference between freedom and captivity.

Why Your Brain Tricks You Into Staying Poor

Marcus wasn’t broke because he was lazy or stupid. He was broke because he was asking the wrong question. When his paycheck hit his account, his first thought was: “What do I need to do this month?” Pay rent, buy groceries, cover the car payment, hit the gym, maybe grab drinks with friends.

Never once did he ask: “What should I buy this month that will pay me back?”

Here’s what blew my mind when I first understood this: Every single dollar Marcus spent was going to someone who owned something. His rent check went to someone who owned real estate. His grocery money went to companies that owned supply chains. His car payment went to someone who owned capital.

Marcus was funding other people’s wealth while building none of his own.

And here’s the trap — it feels responsible. Society trains you to pay everyone else first. Rent, utilities, groceries, insurance. The system is designed to extract your cash before you even think about keeping any.

The Warren Buffett Golf Ball Story

Warren Buffett figured this out when he was 12 years old. He spent his afternoons crawling through bushes around Omaha golf courses, collecting lost balls. Then he’d clean them up and sell them back to golfers — 12 balls for $6.

Most kids would pocket the $6 and buy comic books.

Buffett asked a different question: “What should I buy with this $6?”

He bought more golf balls. Then he hired friends to collect balls while he focused on selling. Then he used that money to buy other cash-generating assets. By age 16, he owned a 40-acre farm.

The pattern was simple: Buy something that generates cash, then use that cash to buy more things that generate cash.

That’s compound interest. Not from savings account pennies — from ownership.

How I Switched From Worker to Owner

Back to my midnight bank account moment. I was earning $78,000 a year and had nothing to show for it except a neat little emergency fund that earned 0.1% interest.

I started asking Buffett’s question: “What should I buy?”

My first answer was embarrassingly small. I had $200 left after paying bills that month. Instead of leaving it in checking, I bought $200 worth of an S&P 500 index fund. Then I did something that felt insane at the time.

I decided to buy $200 worth of index funds BEFORE paying my bills the next month.

Not after. Before.

That month, I had to borrow $80 from my brother to cover groceries. It felt terrible. But here’s what happened: Instead of finding excuses to skip investing, I found ways to make extra money. I sold stuff I didn’t need. I picked up freelance work. I got creative about cutting expenses.

When you pay yourself first — when you buy assets before you pay bills — you force your brain to solve a different problem.

The Compound Effect of Asking the Right Question

Eighteen months later, my index fund was worth $4,200. Not life-changing money, but something had shifted. I owned a tiny piece of Apple, Microsoft, Amazon. While I slept, hundreds of thousands of employees at those companies were working to make my shares more valuable.

That’s when I understood leverage.

I wasn’t just buying stocks. I was buying other people’s labor. I was buying time itself. Every dollar I owned was working while I worked, creating a compound effect that no amount of personal effort could match.

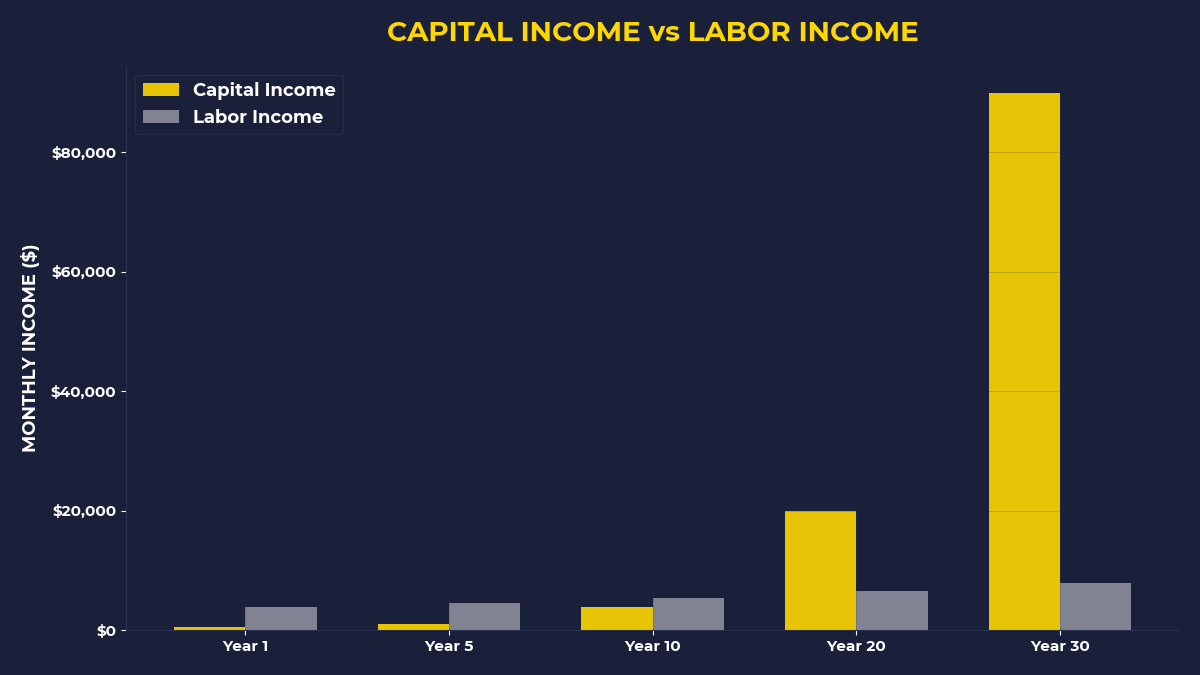

Think about this: If you earn $50,000 a year, you can work harder and maybe push that to $75,000. That’s a $25,000 increase. But if you own $100,000 in assets that generate 8% annually, that’s $8,000 in passive income. And unlike your salary, that compound growth accelerates over time.

What Capital Owners Buy That You Don’t

Do you know what separates capital owners from everyone else? They buy demand.

Every time you pay rent, you’re paying for someone’s demand-generating asset. Every time you buy groceries, you’re funding someone’s supply chain ownership. Every streaming subscription, every coffee run, every Uber ride — you’re sending cash to people who own the systems that fulfill demand.

Capital isn’t money sitting in your checking account. Capital is stored demand. When people need what you own, you have capital.

Here’s the reframe that changed everything for me: Your monthly bills are invoices from capital owners. They own what you need, so you pay them. The goal isn’t to eliminate bills — it’s to switch sides.

The One Question That Creates Wealth

Remember Marcus? When he called me that Thursday night, I asked him one question: “Before you pay a single bill next month, what are you going to buy that will pay you back?”

Six months later, Marcus owns $3,800 in index funds. Not because he suddenly started making more money, but because he started thinking like a capital owner instead of a worker.

The question isn’t complicated: “What should I buy this month?”

Not “What should I do?” — What should I buy?

When you ask this question consistently, your entire relationship with money changes. You stop seeing purchases as expenses and start seeing them as choices. You stop funding other people’s wealth and start building your own.

You join the 3% who understand that wealth comes from ownership, not effort.

If You’re Ready to Think Like an Owner

This post is for you if you’re earning decent money but never seem to get ahead. If you follow all the “responsible” money advice but still feel broke. If you’re tired of funding everyone else’s dreams while building none of your own.

The shift from worker to owner starts with one question.

The One Thing to Remember

Capital owners ask “What should I buy?” while workers ask “What should I do?” The difference creates two completely different financial futures. When you own assets that generate cash flow, other people’s effort compounds your wealth while you sleep. When you only trade your time for money, you’re always one paycheck away from broke.

- Before paying any bill this month, buy $50 worth of an index fund or individual stock — even if it means scrambling to cover expenses

- Replace “What should I do?” with “What should I buy?” every time you think about money

- Track how much money you send to capital owners each month (rent, subscriptions, interest) versus how much you spend buying capital for yourself

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.