The safest investment philosophy is the one that feels most dangerous to follow.

I learned this the expensive way in March 2020. While everyone was selling, I was buying — not because I predicted the recovery, but because my investment philosophy demanded it. The Dow had dropped 37% in five weeks. Every instinct screamed “sell.” Every expert on CNBC was hedging. Every colleague was moving to cash.

I bought more.

Here’s what I discovered: Most people don’t have an investment philosophy. They have someone else’s wealth plan disguised as their own wisdom. The mutual fund industry collects $100 billion annually in fees by selling you “diversified strategies” that guarantee they get rich while you stay middle class. Your 401k provider makes money whether your account goes up or down. Your financial advisor gets paid 1.2% annually whether they beat the market or lose to it.

Your brain thinks you’re building wealth. You’re actually funding theirs.

Why Smart People Follow Dumb Money

Look, I get it. I spent my first five years in investing following what I thought was my own philosophy. Buy low, sell high. Diversify across sectors. Rebalance quarterly. Dollar-cost average into index funds.

Sound familiar?

That’s not a philosophy — that’s a collection of tactics dressed up as wisdom. A real contrarian investment philosophy starts with a structural understanding of how capital actually works, not a list of best practices borrowed from someone else’s playbook.

The difference is profound. Strategy answers “what should I buy?” Philosophy answers “why do I own anything at all?”

Most investors get this backwards. They spend months researching which stocks to pick and zero minutes understanding why they’re picking stocks instead of bonds, or real estate, or their own business, or nothing at all. They’re optimizing tactics while ignoring the foundational question that determines everything else.

Capital Is Stored Demand, Not Stored Money

Here’s where conventional investment philosophy breaks down completely.

Everyone treats capital like it’s money sitting in different containers — stocks, bonds, real estate, commodities. Pick your allocation, rebalance annually, retire rich. Except capital isn’t money at all. Capital is stored demand.

When you own Apple stock, you don’t own pieces of cash flow. You own pieces of humanity’s demand for smartphones, apps, and digital services. When you own a rental property, you don’t own bricks and mortar. You own someone’s need for shelter in that specific location.

This distinction matters because demand is what creates wealth, not the asset itself.

Warren Buffett understood this at age 11 when he collected lost golf balls and sold them for 50 cents per dozen. He wasn’t in the golf ball business — he was in the stored demand business. Golfers would always lose balls. He found a way to capture that recurring demand and turn it into cash flow.

The golf balls were worthless without the demand. The demand was valuable with or without the golf balls.

Why Your Emergency Fund Is Training You To Stay Poor

Every financial advisor tells you to keep 6-12 months of expenses in cash before you start investing.

This is structural thinking designed to keep you poor.

Let me tell you what actually happened to me when I followed this advice. I spent two years building up $47,000 in a high-yield savings account earning 0.8% annually while the S&P 500 gained 31.5% in 2019 alone. My “safe” emergency fund cost me $14,500 in opportunity cost that year.

That’s not safety. That’s expensive anxiety management.

Here’s what your emergency fund actually trains you to do: pay everyone else first. Your landlord gets paid. Your credit card company gets paid. Your insurance company gets paid. Your grocery store gets paid. You — the person creating all the economic activity — get whatever’s left over.

Then you’re told to save that leftover money in cash “just in case.”

Just in case of what? Just in case you need to give more money to landlords, credit card companies, insurance companies, and grocery stores?

The primal instinct here is loss aversion — the brain’s tendency to overweight potential losses versus potential gains. Your emergency fund feels safe because it protects against downside risk. But it guarantees upside loss. You’re choosing certain poverty over uncertain wealth.

The Only Question That Separates Owners From Renters

What should you buy versus what should you do?

Most people spend their entire lives optimizing the second question. They read productivity books, take courses, build skills, climb corporate ladders, start side hustles. All variations of “what should I do to make more money?”

Capital owners ask a different question: “What should I buy to make money while I sleep?”

This isn’t about being lazy. This is about understanding leverage.

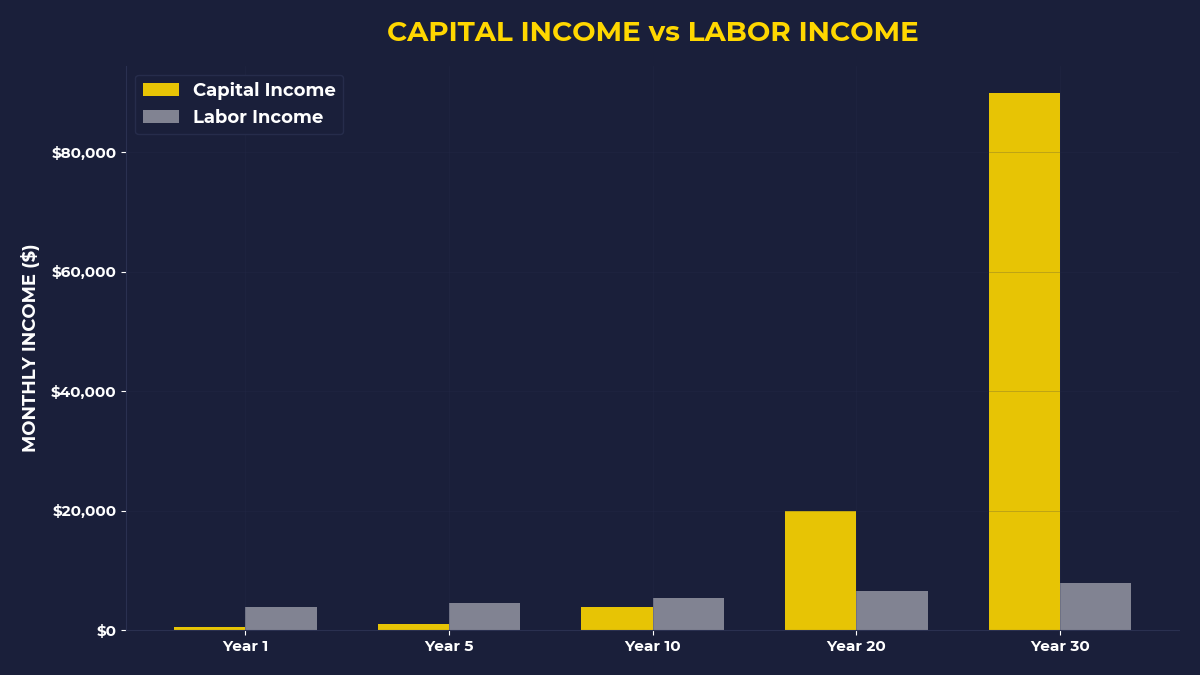

When young Warren Buffett upgraded from picking up golf balls himself to hiring friends to do it for $2 per dozen while he sold them for $6, he wasn’t getting lazier. He was getting structural. His income was no longer limited by his personal time and energy. It was limited by his ability to find and organize demand.

Scale that principle across decades and you get Berkshire Hathaway — a company that owns pieces of dozens of businesses generating cash flow without Warren physically working in any of them.

The golf ball principle scales infinitely. The personal labor principle doesn’t.

Why AI Changes Everything About Contrarian Investment Philosophy

Here’s what 97% of investors miss about the AI revolution: it’s not creating new jobs, it’s creating new forms of capital.

Between 2023 and 2024, NVIDIA’s market cap increased by $1.8 trillion. Not because they hired more engineers — because they built systems that generate value without proportional human input. ChatGPT serves 100 million users with a team of 500 people. Instagram was sold for $1 billion with 13 employees.

AI amplifies capital ownership while diminishing labor value.

If your investment philosophy is built around trading your time and skills for money, you’re about to become obsolete. If your philosophy is built around owning systems that generate demand, you’re about to become wealthy.

The contrarian move isn’t to fear AI — it’s to own it before everyone else figures this out.

The Primal Instinct That Destroys Wealth

Herd behavior is the single biggest wealth destroyer in human history.

During the dot-com bubble, individual investors poured $240 billion into technology mutual funds between 1999 and 2000. The NASDAQ peaked at 5,048 in March 2000, then crashed 78% over the next two years. Those same investors pulled $50 billion out of tech funds in 2001 and 2002 — selling at the bottom.

During the 2008 financial crisis, investors withdrew $234 billion from equity mutual funds while the S&P 500 was down 57%. They missed the entire recovery that followed.

Same pattern. Same instinct. Same result.

Your brain is wired to follow the crowd because for 200,000 years, following the crowd meant survival. The tribe that stuck together lived. The individual who wandered off alone became tiger food.

But capital markets reward the opposite behavior. The crowd is always wrong at turning points because turning points only happen when the crowd changes direction.

A real contrarian investment philosophy means feeling the herd instinct and doing the opposite anyway. Not because you’re smarter than everyone else — because you understand that your brain is running software designed for a different environment.

What The Primal Investor Takes Away

Philosophy beats strategy: Understand why you own capital before deciding what to own. Capital is stored demand, not stored money.

Question the emergency fund: Six months of expenses in cash is six months of guaranteed opportunity cost. Consider keeping 1-2 months max and investing the rest.

Ask “what should I buy?” not “what should I do?”: Labor scales linearly. Capital scales exponentially. Optimize for ownership, not effort.

Own AI instead of fearing it: AI creates capital, not jobs. The wealth transfer is happening now — position yourself as an owner, not a user.

Expect your brain to sabotage you: Herd behavior, loss aversion, and recency bias are features, not bugs. A contrarian philosophy accounts for them structurally.

Start before you feel ready: The best time to build a contrarian investment philosophy is when following the crowd feels safer. That feeling is the signal.

Your investment philosophy determines whether you spend your life building someone else’s wealth or your own. Choose accordingly.

🎬 Prefer watching? Check out the video version on YouTube: