Your brain runs on 50,000-year-old code that thinks a stock market crash means saber-toothed tigers are coming.

That software worked perfectly when survival meant fleeing predators and hoarding winter berries. But in financial markets, those same survival instincts systematically destroy wealth. Every fear-driven sell during a crash, every euphoric buy during a bubble, every decision to follow the herd — that’s your ancient operating system executing perfectly obsolete programming.

I learned this the expensive way in March 2020. When the S&P 500 dropped 34% in five weeks, my primitive brain screamed one word: RUN. Every neuron fired the same ancient message: “Danger! Preserve resources! Avoid the tribe’s panic!” I watched my portfolio bleed and felt the overwhelming urge to sell everything.

Here’s the thing about behavioral finance that most people miss: it’s not about controlling your emotions. It’s about recognizing that you’re a primate trying to navigate a system designed by other primates, all running the same buggy software.

The Fear Algorithm That Costs You Fortune

Let me tell you about loss aversion, the most expensive cognitive bias in your brain.

Studies show humans feel the pain of losing $100 about 2.5 times more intensely than the pleasure of gaining $100. This isn’t a character flaw — it’s evolution. When your ancestors lost their winter food supply, they died. When they found extra berries, they just had a slightly better week.

But in capital markets, this survival mechanism becomes wealth destruction machinery.

I once watched a friend sell his Apple stock in 2018 after it dropped 20% from its peak. He couldn’t sleep at night, he said. The loss felt “too real.” Six months later, Apple hit new highs. His loss aversion cost him $23,000 on a position he’d held for three years.

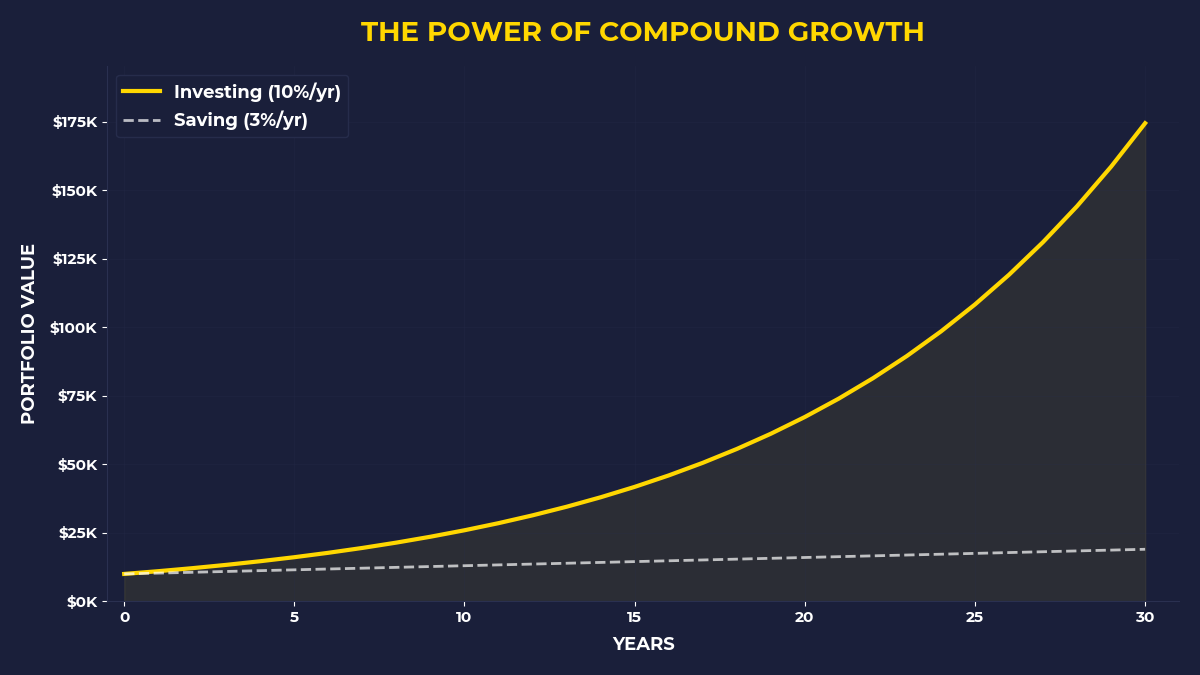

The math is brutal but clear: the average investor earned 3.1% annually over the 20 years ending in 2019, while the S&P 500 returned 6.1%. That 3% gap? Pure behavioral tax. Fear selling bottoms, greed buying tops, loss aversion triggering exits right before recoveries.

Your primitive brain literally cannot distinguish between losing money and losing your life.

Why Your Herd Instinct Makes You Poor

Here’s a question that will make you uncomfortable: How many of your investment decisions were actually YOUR decisions?

Think about it. You bought tech stocks in 1999 because everyone said the internet changed everything. You avoided stocks in 2009 because everyone knew the economy was broken. You bought crypto in 2021 because everyone was getting rich.

Each time, you thought you were being rational. But you were just following the tribe.

Herd behavior saved our ancestors. When the group suddenly ran, you ran too — first, think later. The ones who stopped to analyze the situation became lunch. But financial markets punish herd followers with mathematical precision. When everyone thinks alike, no one thinks very much, and capital flows toward whoever’s thinking differently.

I remember sitting in a coffee shop in late 2008, listening to three different conversations about how “the market will never come back.” The Dow had fallen from 14,164 to 6,547. Everyone knew stocks were dangerous. Everyone was selling.

That’s when I realized the most powerful truth about behavioral finance: the best investment opportunities feel like the worst investment decisions.

The Recency Trap That Steals Your Future

Your brain has another expensive bug: it thinks whatever happened recently will keep happening forever.

After the dot-com crash, investors avoided technology stocks for years, missing the rise of Google, Apple, and Amazon. After 2008, they avoided real estate, missing one of the greatest housing recoveries in history. After every crash, they avoid stocks right when stocks become most attractive.

This is recency bias — your primitive brain’s lazy pattern-matching system. It assumes today looks like yesterday, which made sense when yesterday’s weather predicted today’s hunting conditions. But markets are not weather systems. They’re mean-reverting probability distributions that punish linear thinking.

Look at the numbers: During the 10 years following the 2008 financial crisis, the S&P 500 returned 13.6% annually. But household stock allocation hit its lowest level in decades. Investors were so scarred by recent losses that they avoided the very asset class delivering the highest returns.

The tragic irony? The more recent the market trauma, the better the future returns tend to be.

The Anchoring Bias That Costs You Millions

Want to see your brain malfunction in real time? Ask someone what they think Apple stock is worth.

Most people will immediately anchor to the last price they remember — maybe $180, maybe $150, maybe whatever they saw on their phone this morning. Then they’ll adjust slightly up or down from that anchor. But that anchor is completely arbitrary. It has nothing to do with Apple’s cash flows, competitive position, or intrinsic value.

This anchoring bias destroys wealth by making you think in terms of prices instead of value.

I used to anchor every investment decision to what I paid. If I bought a stock at $50 and it dropped to $40, I’d think it was “down $10” rather than asking whether $40 was attractive for future returns. I’d hold losing positions hoping to “get back to even” and sell winning positions because they felt “too expensive” relative to my purchase price.

Your cost basis is psychologically important and financially irrelevant. The market doesn’t care what you paid. It only cares what the asset is worth today and tomorrow.

The Status Quo Bias That Keeps You Broke

Here’s the most dangerous bias nobody talks about: your brain’s addiction to the status quo.

Humans have a powerful psychological need to do nothing. It feels safer. It requires no decisions. It avoids regret. But in financial markets, doing nothing is a decision — and usually the worst one.

Consider this: 60% of Americans have less than $1,000 in savings, but most aren’t broke because they can’t save. They’re broke because saving feels harder than not saving. Investing feels riskier than not investing. Building capital feels more dangerous than building wages.

Status quo bias makes you default to cash, which loses purchasing power to inflation. It makes you default to your employer’s 401(k) options, which are often expensive and mediocre. It makes you default to whatever financial advice you heard first, rather than seeking better information.

The most expensive decision you’ll ever make is the decision to keep doing what you’re already doing.

How The Primal Investor Rewires The Code

What if I told you the solution isn’t to overcome your biases, but to design systems that work with them?

Smart investors don’t fight their primitive brains — they outsmart them. They build structures that turn evolutionary instincts into wealth-building advantages.

When I feel the urge to sell during market panic, I’ve learned to interpret that feeling as a buy signal. When everyone around me is euphoric about an investment, I take profits. When something feels “too risky,” I look closer — that might be my loss aversion protecting me from asymmetric upside.

The key insight from behavioral finance isn’t that your brain is broken. It’s that your brain is optimized for a world that no longer exists. Once you accept this, you can start building decision frameworks that account for your cognitive limitations.

I now make most investment decisions when markets are calm, not during crises. I automate purchases so my present self can’t overrule my past self’s logic. I write down my investment thesis before I buy, so I can distinguish between changed fundamentals and changed feelings.

What The Primal Investor Takes Away

• Your primitive brain will always try to sell bottoms and buy tops — design systems that override these impulses before they happen

• The strongest investment conviction often feels like the worst investment decision — use discomfort as a contrarian signal, not a reason to avoid action

• Automate capital allocation during calm periods so your panicked future self can’t sabotage your rational present self

• When everyone around you agrees about an investment, that’s usually the most dangerous time to follow the crowd

• Your cost basis is emotionally important and financially irrelevant — focus on future value, not past prices

• The most expensive decision you’ll make is defaulting to whatever feels safest right now

Your ancient brain kept your ancestors alive, but it will keep you poor. The investors who build lasting wealth aren’t the ones with better predictions — they’re the ones with better systems for managing their own predictable irrationality.

🎬 Prefer watching? Check out the video version on YouTube: