The Most Expensive Consultant You Never Hired

Your brain has been managing your money for years, and it’s terrible at the job.

Every market crash follows the same script. Fear takes control in October. Panic spreads by November. By March, when blood runs in the streets, 73% of retail investors have sold their best positions at the worst possible prices. The S&P 500 dropped 57% between October 2007 and March 2009, but individual investors lost an average of 89% because they couldn’t stop their own brains from destroying their wealth.

Here’s what nobody tells you about behavioral finance: it’s not about market psychology. It’s about your psychology. The market doesn’t have emotions. You do. And those emotions are following prehistoric software that kept your ancestors alive but keeps you poor.

I Used To Think I Was Rational About Money

Let me be honest. I once sold my entire position in Amazon at $847 per share in February 2018.

Why? The stock had dropped 8% in three days. My primitive brain screamed “danger” and I listened. I convinced myself I was being “disciplined” and “protecting capital.” Amazon closed that year at $1,501. My brain cost me $37,000 on that position alone.

The kicker? I had studied behavioral finance. I knew about loss aversion. I understood recency bias. I could explain why other investors made terrible decisions. But when my own money was on the line, I became just another primate following the herd off the cliff.

Most people think behavioral finance is academic theory. It’s not. It’s the difference between building wealth and watching others build wealth with your money.

Your Brain Is Running Ancient Software

Every terrible investment decision you’ve made follows the same pattern. Fear overrides logic. Greed silences reason. The herd instinct drowns out independent thinking.

Think about your last major investment mistake. I’ll bet it involved one of three primitive responses:

Loss aversion: You held losing positions too long because selling would make the loss “real.” Your brain treats a $1,000 loss as more painful than a $1,000 gain feels good. This isn’t a personality flaw — it’s genetic code that helped your ancestors survive famines but keeps you holding garbage stocks.

Recency bias: Whatever happened recently feels permanent. Tech stocks crashed in March 2020? Technology is dead forever. Crypto gained 400% in 2021? Digital assets only go up. Your brain extrapolates the immediate past into the distant future because pattern recognition once helped identify seasonal changes and predator behavior.

Herd behavior: When everyone else is buying GameStop at $300, joining the crowd feels safer than thinking independently. Your ancestors survived by sticking with the tribe. But markets reward independent thinking, not social cohesion.

These instincts aren’t bugs in your psychological system. They’re features that kept humans alive for 200,000 years. They just happen to be financial suicide in modern markets.

Why Smart People Make Dumb Money Decisions

Intelligence doesn’t protect you from behavioral traps. Sometimes it makes them worse.

A 2019 study of 60,000 brokerage accounts found that investors with graduate degrees underperformed the market by 1.2% annually compared to 0.8% for high school graduates. Why? Smart people create elaborate justifications for their emotional decisions. They build complex models to explain why their gut feeling must be correct.

I know a neurosurgeon who lost $180,000 day-trading during the pandemic. Brilliant man. Saves lives daily. Can’t stop his own brain from buying high and selling low. His intelligence gave him confidence to make bigger mistakes, not fewer mistakes.

The problem isn’t lack of information. It’s too much confidence in your ability to process information rationally when money is involved.

What Does Fear Actually Cost You?

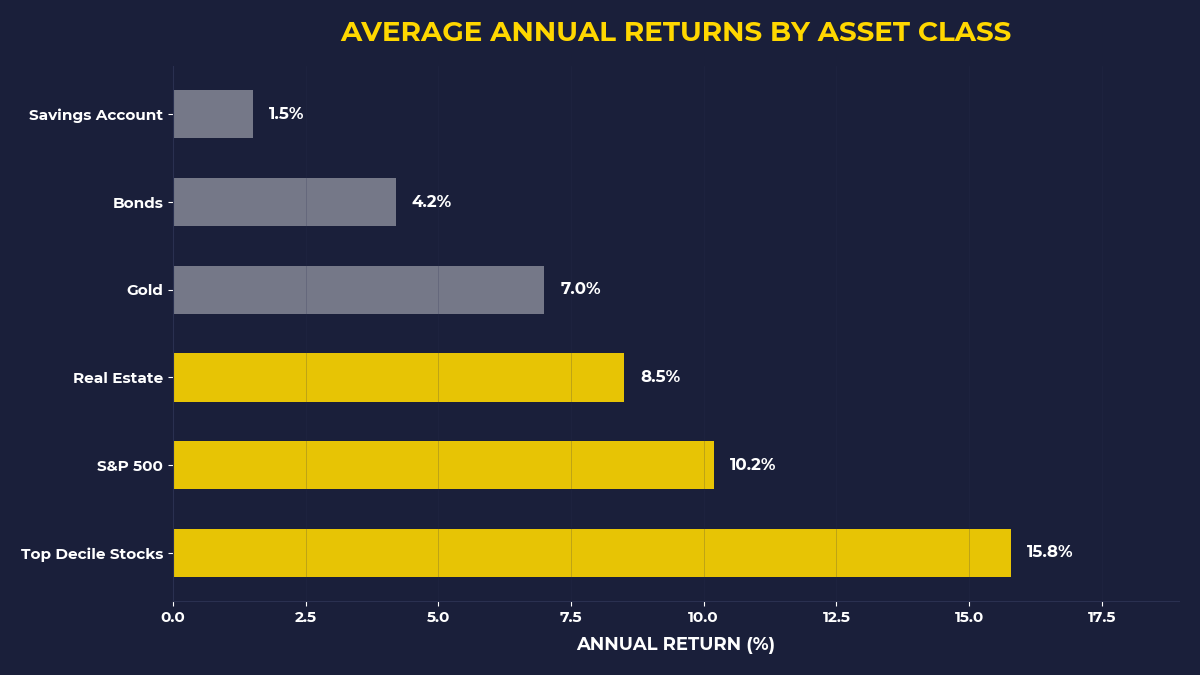

Here’s a number that should terrify every investor: the average equity mutual fund returned 10.2% annually between 2000 and 2020, but the average investor in those funds earned just 3.9%.

That 6.3% annual gap represents $847,000 over 20 years on a $50,000 initial investment. Fear didn’t just cost you money. It cost you financial freedom.

Why the massive gap? Investors bought after gains and sold after losses. They let primitive instincts override compound returns. They treated investing like hunting dangerous animals instead of owning productive assets.

Every behavioral finance textbook explains this phenomenon. Almost no one fixes it.

The Contrarian’s Behavioral Edge

Real contrarian investing isn’t about being different. It’s about recognizing when your instincts are about to destroy your wealth — and doing the opposite anyway.

Warren Buffett didn’t become rich by predicting the future. He became rich by buying when his gut said “sell” and holding when his gut said “run.” In October 2008, while everyone else was panic-selling, Buffett published an op-ed titled “Buy American. I Am.” The market dropped another 25% after his article. His primitive brain probably screamed at him daily. He ignored it.

Berkshire Hathaway gained 5,600,000% between 1965 and 2021 not because Buffett has superhuman intelligence, but because he has superhuman discipline. He recognizes the voice of fear and greed — then does the structural opposite.

The contrarian edge isn’t emotional. It’s mechanical. Feel fear? Buy quality assets. Feel euphoria? Take profits. Feel uncertain? Stick to the system.

How To Reprogram Your Money Brain

You can’t eliminate behavioral biases. But you can build systems that work despite them.

Here’s what actually works: automate the decisions your emotions want to hijack. Set up systematic buying when markets drop 10%, 20%, and 30%. Program selling rules when positions reach predetermined profit targets. Remove discretion from the moments when your brain will sabotage you most.

I learned this the hard way. After my Amazon disaster, I built mechanical rules. If the S&P 500 drops 15% in any month, I buy. If any position reaches 25% of my portfolio, I trim. If I feel “certain” about any investment thesis, I reduce position size.

The system isn’t perfect. But it’s better than trusting my primate brain with compound returns.

The One Question That Changes Everything

Before every investment decision, ask yourself: “What primitive instinct is driving this choice?”

Are you buying because everyone else is buying? That’s herd behavior. Are you avoiding an asset because you lost money on it before? That’s loss aversion. Are you extrapolating recent performance into the future? That’s recency bias.

Name the instinct. Then ask: “What would I do if I were trying to compound capital over 20 years instead of surviving the next threat?”

This simple question has saved me more money than any technical analysis or fundamental research. It forces conscious thought over unconscious reaction.

What The Primal Investor Takes Away

• Your brain uses 200,000-year-old software to make investment decisions in modern markets — recognize the mismatch and plan accordingly

• Fear sells bottoms, greed buys tops, and herd behavior chases performance — mechanical systems beat emotional decisions every time

• The 6.3% annual gap between fund returns and investor returns represents $847,000+ in lost wealth over 20 years

• Before every investment decision, ask: “What primitive instinct is driving this choice?” — naming the bias neutralizes half its power

• Automate decisions during emotional extremes — systematic buying during crashes and systematic selling during bubbles

• Intelligence doesn’t protect against behavioral traps — it often makes them more expensive by providing better rationalizations

Your brain will never stop trying to sabotage your wealth. But once you recognize the patterns, you can build systems that compound capital despite your instincts. The market rewards patient capital, not primate reactions.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.