The investors who blow up the most spectacularly are almost never the ones who didn’t know enough. They’re the ones who knew too much — and trusted it.

I’ve been in rooms with people who could recite Shiller P/E ratios from memory, diagram the yield curve with a napkin, and debate terminal growth rates with the precision of a surgeon. And I’ve watched those same people panic-sell in March 2020, averaging out of their best positions at the exact moment the market was pricing in the end of Western civilization. They knew everything. They acted on fear anyway. That’s the trap nobody in the behavioral finance literature explains clearly enough: the problem isn’t ignorance. It’s the illusion of control that knowledge creates.

I Used to Think Understanding Biases Was Enough

Here’s the thing. I read Kahneman’s work on System 1 and System 2 thinking sometime around 2012. I read Thaler. I read the white papers on loss aversion — the finding that losses feel roughly twice as painful as equivalent gains feel good. I could identify anchoring, recency bias, the disposition effect. I thought I was inoculated.

Then 2015 happened. Chinese markets cratered. The S&P 500 dropped about 12% in two weeks that August. My portfolio had a concentrated position in an industrial company I genuinely believed in — strong free cash flow, narrow moat, cheap on any reasonable earnings basis. It dropped 22% in eleven days. And I sold it. Not because the thesis changed. Not because a single fundamental shifted. I sold it because the number on my screen felt like an accusation. Loss aversion — that ancient primate reflex wired in before humans even had language — reached up through my prefrontal cortex, bypassed everything I’d read, and moved my cursor to the sell button.

That position recovered 78% over the following 18 months. I was not in it.

Reading about cognitive biases is like reading about altitude sickness at sea level. You understand it perfectly. Then the mountain gets involved.

The Real Architecture of Your Brain’s Investment Problem

What behavioral finance gets right is that your instincts evolved for a world that no longer exists. What it often gets wrong is the prescription — as if labeling a bias is the same as defeating it.

Loss aversion made complete evolutionary sense in an environment where losing food in winter meant death. The herd instinct that drives investors to chase whatever sector is up 40% — that same pull kept early humans from wandering alone into predator territory. Recency bias, which causes investors to extrapolate the last 18 months of returns into eternity, was actually adaptive when the last rainy season was your best prediction for the next one.

None of these instincts are malfunctions. They’re legacy code running on modern hardware.

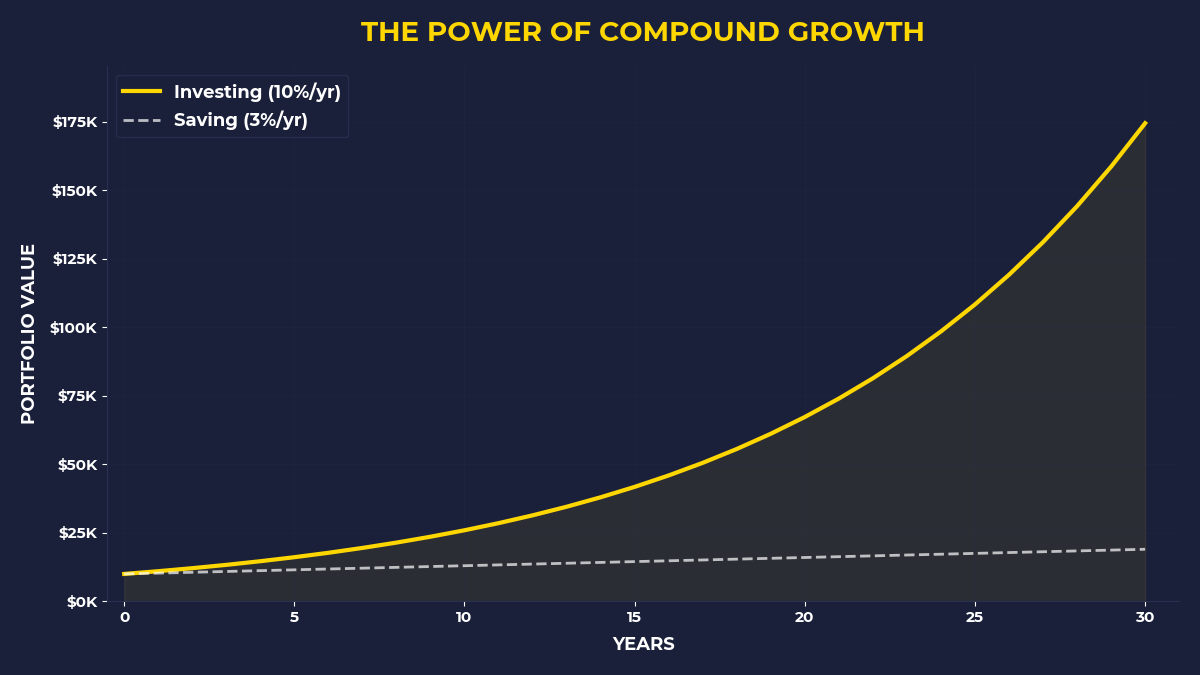

And that gap — between what the code was written for and the environment it now operates in — is where wealth is won and lost. The S&P 500 returned an average of approximately 10.5% annually between 1957 and 2023. The average equity fund investor captured roughly 6.3% of that over comparable periods, according to Dalbar’s long-running quantitative analysis of investor behavior. The missing 4.2% wasn’t stolen by fees alone. It was surrendered, voluntarily, every time a human being overrode their investment thesis with a feeling.

Think about that. The market offered 10.5%. The average investor took 6.3%. The entire gap is behavioral.

What Nobody Tells You About Overconfidence

Does your investment process feel especially clear to you right now? Do you have high conviction in a thesis? Are you certain you’ve identified something the market is mispricing?

Be careful. That clarity is one of the most reliable warning signs in investing.

Overconfidence isn’t just about arrogance. It operates more subtly than that. It emerges precisely after you’ve done the work — after you’ve built the model, read the 10-Ks, talked to industry contacts, assembled a picture that makes sense. The more thorough your analysis, the more your brain signals certainty, and the more it begins editing out disconfirming evidence. Psychologists call this confirmation bias. I call it the part of your brain that decides it has earned the right to stop listening.

In a study of 84,000 investor accounts between 1991 and 1997, researchers Brad Barber and Terrance Odean found that the most active traders — the ones trading most frequently, presumably those with the highest conviction — underperformed the least active traders by 6.5 percentage points annually. Not 0.5%. Not 1%. Six and a half points. Per year. The investing equivalent of running hard in the wrong direction.

Here’s what that study was really documenting: the cost of feeling smart.

The Structural Frame That Actually Helps

I’ve tried willpower. I’ve tried checklists. I’ve tried meditation, cold showers, and sleeping on decisions for 48 hours. All of it helps marginally at the margins.

What works structurally — what actually protects you from yourself — is building a system that takes the decision out of the moment. Because in the moment, you will lose. Every time. The primate brain is fast; the prefrontal cortex is slow. When the market drops 15% in a week, fear arrives in milliseconds. Rational analysis takes minutes. Fear wins on latency alone.

The investors I respect — not the ones who predict well, but the ones who endure and compound — have almost all arrived at the same design principle: make the consequential decisions when the market is closed and your nervous system is calm, then automate their execution so that the emotional version of you can’t intervene.

Warren Buffett, paraphrasing his own approach across decades of letters, has essentially described his edge not as superior analysis but as superior temperament — the ability to be greedy when others are fearful, and fearful when others are greedy. That sounds like advice. It’s actually a structural description. He built Berkshire to be able to hold cash for years and deploy aggressively at bottoms — a system-level design that made patience the default state, not a daily act of willpower.

Between October 2007 and March 2009, the S&P 500 declined 57%. Anyone who held — not bought more, just held — recovered fully by March 2013. Anyone who sold and waited for “clarity” before re-entering locked in the loss permanently. The behavioral gap between those two groups wasn’t knowledge. It was structure.

The Thinking Tool You Can Use Tomorrow

I want to give you something concrete. Not a stock screen. A question.

Every time you feel a strong urge to act on your portfolio — to buy aggressively, to sell, to rotate — ask yourself this: Am I responding to the price, or to the business?

That’s it. That’s the whole tool.

If your answer is “the price moved and it’s making me nervous,” you’re in the grip of a primate instinct. The price is not the asset. The price is the market’s current emotional read on the asset. The business — its demand structure, its durable competitive position, its ability to generate cash for owners — is moving on a completely different timeline than the price.

This is what capital actually is, underneath all the finance theory: it’s stored demand. A great business owns a piece of ongoing human want — for software, for consumer goods, for financial services — and compounds that want into owner returns year after year. The price screen you’re staring at is a daily referendum on sentiment, not on that underlying demand structure. Most of that referendum is noise generated by other primates reacting to each other.

Look. When you feel the urge to sell, the question is not “is the price going lower?” You cannot answer that. Nobody can. The question is “has the demand structure of this business changed?” If yes, sell. If no, the urge you feel is loss aversion pretending to be analysis.

And when you feel the urge to buy something because it’s already up 60% this year and everyone is talking about it, that urge has a name: herd behavior. The tribe is moving; your nervous system wants to move with it. The price has already priced in the excitement. What you’re buying at that moment is the sentiment, not the asset.

This Matters Most If You’re Already Sophisticated

If you’re a complete beginner, none of this is your most pressing problem. Your most pressing problem is not owning equity at all.

But if you’re the kind of investor who reads widely, thinks carefully, has a genuine framework — you are at particular risk. Because your knowledge gives your instincts a vocabulary. Loss aversion doesn’t show up as “I’m scared.” It shows up as “the macro environment is deteriorating and I want to reduce risk.” Herd behavior doesn’t show up as “everyone else is buying this.” It shows up as “the momentum is clearly constructive and the setup is asymmetric.”

Your intellect is not protecting you from your instincts. It is dressing them in better clothes.

A friend of mine — former derivatives trader, genuinely one of the sharper thinkers I know — told me once that his worst trades all had the best-written memos. He’d spent so long building the case that by the time he placed the order, he’d stopped being able to hear anything that contradicted it. Confirmation bias wearing a research report as a costume.

I’ve made the same mistake. Most honest investors have.

What The Primal Investor Takes Away

- Name the instinct before you act. Before any portfolio decision, identify which primate drive is in the room: fear, greed, herd behavior, recency bias, loss aversion, overconfidence. Naming it doesn’t eliminate it, but it creates one second of distance between the feeling and the action. One second is sometimes enough.

- Separate price from business. When you feel urgency, ask whether the underlying demand structure of the asset has changed — not whether the price has moved. If the business is intact, the urgency is noise.

- Make decisions when the market is closed. Your investment policy — what you own, at what concentration, through what drawdowns — should be decided on a Sunday afternoon, not on a Tuesday when prices are cascading. The emotional you should not be the deciding you.

- Automate execution of calm decisions. Systematic monthly purchases into quality equity positions remove the emotional veto. Between 2009 and 2024, an investor who systematically bought the Nasdaq-100 regardless of headlines compounded at approximately 18.4% annually. Most people who tried to time it captured far less.

- Audit your highest-conviction ideas hardest. The thesis that feels most bulletproof deserves the most aggressive stress-testing. Certainty is a symptom, not a signal. The moment you stop looking for disconfirming evidence is the moment overconfidence has you.

- Hold the structure; let the structure hold you. The behavioral edge isn’t cleverness. It’s owning businesses with durable demand, surviving the drawdowns that shake everyone else out, and not confusing your nervous system’s state with the asset’s value.

Your brain is not broken. It’s running code designed for a world that no longer exists, in a market that punishes every instinct that code produces. The contrarian edge has never been about knowing more. It’s about building a structure that keeps the primate from touching the controls.

Feel the fear. Hold anyway. That’s the whole game.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.