The Million-Year-Old Operating System Running Your Portfolio

Your brain has not received a software update in 50,000 years. Yet you’re using this Stone Age hardware to make 21st-century investment decisions.

The same neural wiring that kept your ancestors alive when saber-toothed tigers prowled the savanna now triggers panic selling when the S&P 500 drops 3% in a day. The same herding instincts that helped early humans survive famines now drive you to buy Bitcoin at $65,000 because “everyone else is doing it.”

I learned this the expensive way. In March 2009, when the S&P 500 had already fallen 57% from its peak, I sold everything. Not because of analysis. Because of terror. My primitive brain screamed “DANGER” so loudly that I couldn’t think straight. I was watching my net worth evaporate daily, and every caveman instinct I possessed demanded I run for safety.

That decision cost me roughly $180,000 over the next five years as markets recovered. The math still makes me wince. But the lesson was invaluable: **the biggest threat to your wealth isn’t market volatility — it’s the primal programming between your ears.**

Why Smart People Make Dumb Money Decisions

Here’s what I find fascinating about behavioral finance. You can have a PhD in economics, understand efficient market theory, and still get your lunch eaten by your own amygdala.

Consider this: during the dot-com crash between 2000 and 2002, the average equity mutual fund lost 12% annually. But the average equity mutual fund investor lost 23% annually during the same period. The difference? Behavioral timing. Investors bought high when greed peaked and sold low when fear bottomed out.

Your brain doesn’t care about your financial education. When markets crater, it dumps adrenaline into your bloodstream and screams “ESCAPE NOW.” When everyone else is getting rich on meme stocks, it floods you with FOMO and shouts “GET IN BEFORE IT’S TOO LATE.”

Think about that. The very organ responsible for making investment decisions is actively working against your financial interests.

The Five Primal Forces Destroying Your Wealth

Let me walk you through the primitive instincts that turn smart people into wealth-destruction machines. I’ve fallen victim to every single one.

Loss aversion makes you feel the pain of a $1,000 loss twice as intensely as the pleasure of a $1,000 gain. This isn’t a personality flaw — it’s hardwired survival programming. Your ancestors who were casual about losing resources didn’t survive long enough to become your ancestors. But in investing, this translates to holding losers too long and selling winners too early.

Recency bias convinces you that whatever just happened will keep happening. Real estate only goes up! (2007). Tech stocks never crash! (1999). Inflation is dead! (2019). Your brain takes recent patterns and extrapolates them into permanent truths. This worked when predicting animal migration patterns. It fails spectacularly when predicting market cycles.

Herding behavior made sense when choosing which berry bushes to pick or which hunting grounds to explore. If everyone else was doing it, it was probably safe. Today, this instinct drives you to buy index funds at the peak of bull markets and dump everything during crashes — precisely when you should be doing the opposite.

Anchoring bias locks your brain onto the first piece of information it receives and refuses to let go. You buy a stock at $50, watch it drop to $30, and can’t sell because $50 becomes your “anchor.” Meanwhile, rational analysis might suggest it’s heading to $15.

Availability heuristic makes vivid, recent memories feel more probable than boring statistics. One friend gets rich day-trading crypto, and suddenly that feels more likely to happen to you than the historical data showing 90% of day traders lose money over five years.

What Does Behavioral Finance Actually Mean for Contrarian Investors?

Here’s where most behavioral finance advice goes wrong. It tells you to “be aware of your biases” as if awareness alone fixes the problem.

That’s like telling someone having a panic attack to “just relax.” Your limbic system doesn’t care that you intellectually understand loss aversion. When you’re watching your portfolio bleed red for the sixth straight day, your prehistoric brain takes over.

True contrarian investing isn’t about fighting your biases — it’s about building systems that work despite them. The goal isn’t to eliminate fear when everyone is selling. The goal is to buy anyway.

I’ve learned to think of my emotions as market indicators. When I feel sick to my stomach looking at my portfolio, that’s usually the best time to buy more. When I feel euphoric about my returns, that’s my signal to trim positions. The stronger the emotion, the stronger the signal.

This is why I now invest a fixed percentage of my income every month, regardless of how I feel about markets. The system overrides the monkey brain.

The Warren Buffett Golf Ball Principle vs. Your Primal Brain

Young Warren Buffett used to collect lost golf balls from water hazards and resell them for profit. But here’s what separated him from other kids doing the same thing: he used those profits to buy assets that generated more cash flow, then reinvested that cash flow into more assets.

Most people’s brains are wired to work for money, spend money, repeat. Buffett’s brain was wired to work for money, buy productive assets, let assets work for him, repeat. The difference isn’t intelligence — it’s behavioral programming.

Your primitive brain sees cash as safety and spending as reward. It doesn’t understand compound interest because compound interest doesn’t exist in nature. But **capital is stored demand** — ownership of cash-generating assets that work while you sleep. The golf ball business wasn’t the goal. Building systems that generated cash without Warren’s direct labor was the goal.

Here’s the behavioral trap: when you have $1,000, your brain wants to either spend it (immediate gratification) or save it (loss aversion). Investing it in productive assets feels dangerous because you might lose it. Your ancestors who took unnecessary risks with scarce resources didn’t survive. But in modern markets, not taking calculated risks is the biggest risk of all.

Why Contrarian Investing Feels So Wrong

Every fiber of your being will resist true contrarian behavior. This isn’t a bug — it’s a feature. If contrarian investing felt natural and comfortable, everyone would do it, and the edge would disappear.

When markets crashed in March 2020 and the S&P 500 dropped 34% in five weeks, your brain was screaming one message: “SELL EVERYTHING NOW.” Headlines predicted the end of capitalism. Your 401(k) was evaporating. Every primitive instinct demanded you run for safety.

The contrarian move was to buy more. But buying more when everything feels broken requires overriding millions of years of evolutionary programming.

I remember sitting in my apartment during that crash, physically sick from watching my net worth crater. But I forced myself to buy more index funds. Not because I was brave — because I had trained myself to follow systems instead of feelings. That decision generated more wealth in two years than the previous five combined.

Building Anti-Fragile Investment Systems

Your behavioral programming isn’t going away. The solution is building investment systems that assume you’ll make emotional decisions at exactly the wrong times.

Systematic dollar-cost averaging removes timing decisions from your emotional brain. Automatic rebalancing forces you to sell high and buy low without thinking about it. Pre-committed position sizing prevents you from going all-in during euphoric moments.

But here’s the part most people miss: **you need to design these systems during calm periods, not during crashes.** When markets are volatile, your prefrontal cortex goes offline and your amygdala takes control. You cannot think rationally during moments of peak fear or greed.

The wealthy automate their wealth-building. The poor try to time it.

What The Primal Investor Takes Away

• Your brain’s operating system was designed for surviving famines, not building wealth — acknowledge this handicap and build systems accordingly

• Emotions are market indicators, not decision-making tools — peak fear signals buying opportunities, peak euphoria signals selling opportunities

• Automate investment decisions during calm periods to override behavioral programming during volatile periods

• True contrarian investing means buying when your primitive brain is screaming “sell” — if it feels comfortable, you’re probably following the herd

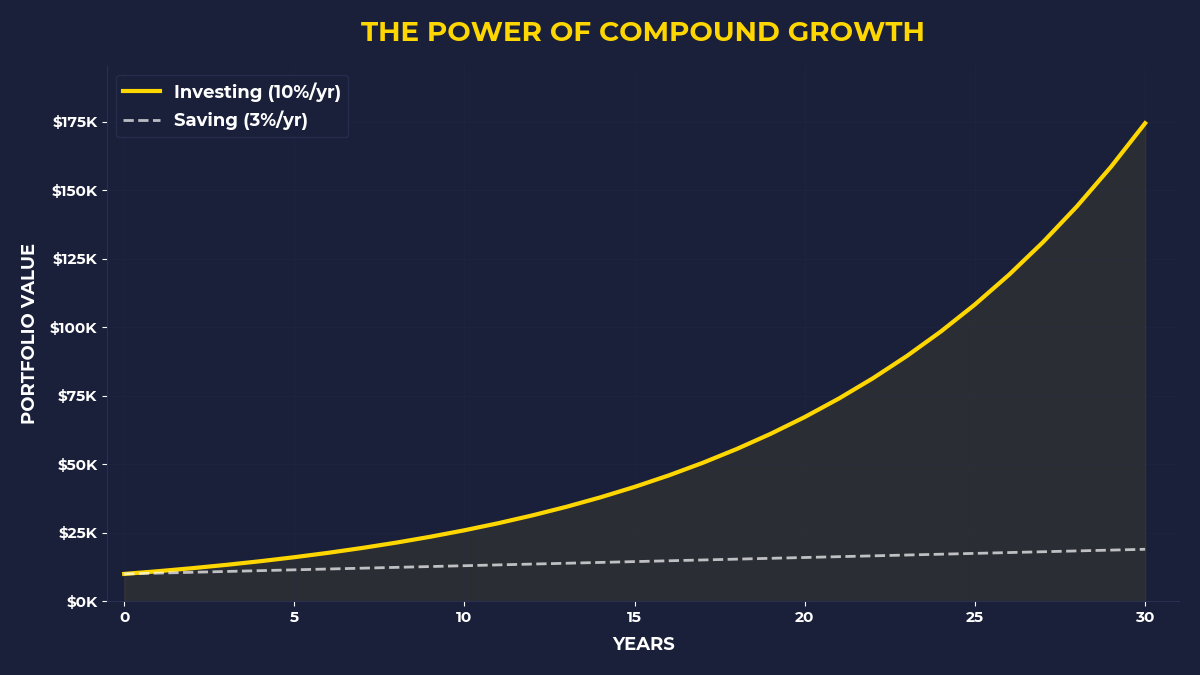

• Focus on acquiring productive assets that generate cash flow while you sleep — your brain wants to work for money, but capital works for you

**The investors who build lasting wealth aren’t the ones who overcome their behavioral programming — they’re the ones who build systems that work despite it.** Your Stone Age brain will never be your ally in building 21st-century wealth. But it doesn’t need to be your enemy either.

🎬 Prefer watching? Check out the video version on YouTube: