James — 31, software developer in Seattle, $104,000 a year — called me on a Tuesday in October 2022, right when the S&P 500 was down 24% for the year and every finance headline looked like a funeral announcement. He’d been investing for about three years. He had roughly $18,000 in a brokerage account and another $6,000 in a company 401(k). Not bad for someone who’d started from zero.

He wanted to know if he should sell.

“Everything’s dropping,” he said. “My friends are getting out. My coworker liquidated his entire Roth last week. It just feels like the smart move is to wait until things stabilize.”

I asked him what he was planning to buy once things “stabilized.” He went quiet for a second. “I don’t know. The same stuff, I guess. Just… at a safer time.”

That pause told me everything.

I’ve Been Exactly Where James Was

When I first started thinking seriously about capital, I was 26, sitting in a studio apartment with a $43,000 salary and a deeply confused relationship with money. I had a checking account, a savings account with maybe $1,200 in it, and the general sense that if I just worked harder and spent less, things would eventually work out. Which is what everyone around me believed too.

I remember reading something that stopped me cold. The idea was simple: every single day, money flows from the people who don’t own things to the people who do. Your rent check. Your car payment. Your Netflix bill. Your morning coffee. Every one of those transactions moves your cash toward someone who owns an asset — and away from you. You are, without realizing it, running a daily revenue operation for other people’s capital.

Look, that sounds obvious when you say it out loud. But it didn’t feel obvious to me at 26. It felt like a gut punch. Because once you see it, you can’t unsee it. The question shifts from “how do I earn more?” to “how do I get on the other side of these invoices?”

That reframe changed everything about how I understood investing — and why most people get it backwards.

The Real Reason Everyone Sells at the Wrong Time

Here’s the thing about market crashes. They don’t feel like opportunity when you’re inside them. They feel like everyone finally figured out something you missed. The news is scary. Your friends are scared. Your coworker just sold everything. The intelligent-seeming move is to wait.

But wait for what, exactly?

This is the trap. When prices drop, what’s actually happening isn’t that assets are becoming less valuable. It’s that fewer people want them right now. Demand — temporary, emotional, herd-driven demand — has shifted. And in that gap between what something is worth and what the crowd is willing to pay for it in a panic, that’s where ownership gets transferred.

From the scared to the patient. From the reactive to the deliberate. From people who think about what to do to people who think about what to buy.

James’s coworker didn’t lose money because the market fell. He locked in his losses on the way down and then, almost certainly, bought back higher on the way up. That’s not bad luck. That’s the default setting for a brain that was never rewired toward ownership thinking.

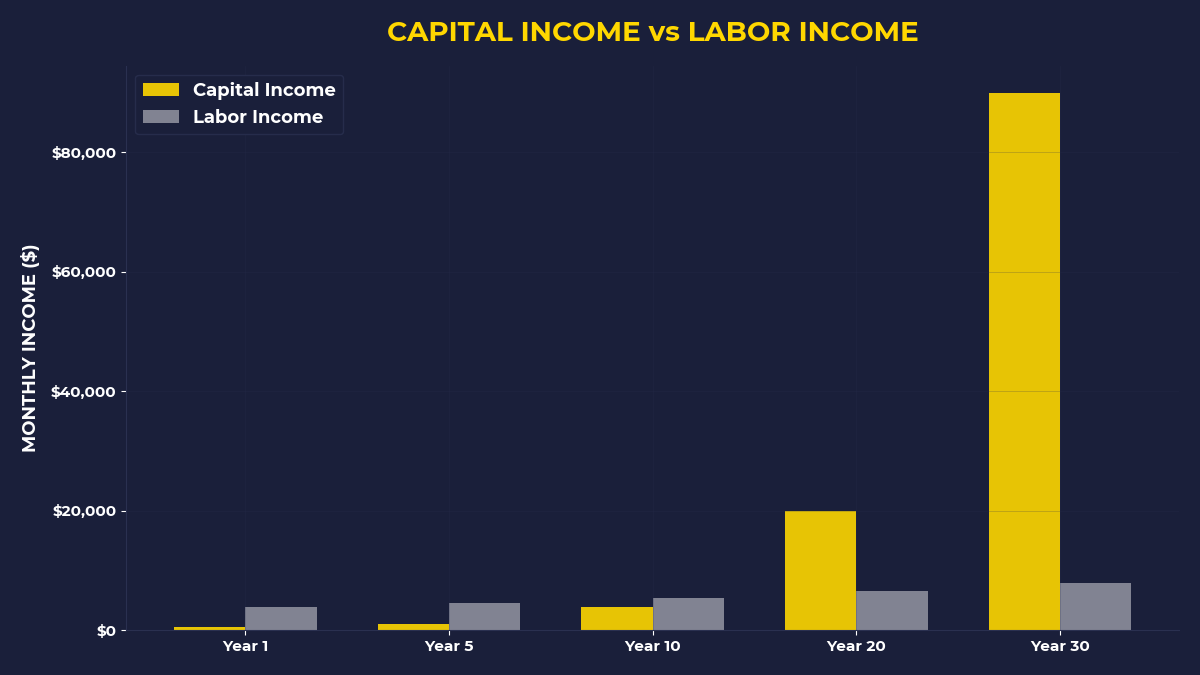

Capital Is Stored Demand — Not Money

This is the reframe that matters most, and almost nobody explains it this way.

Capital isn’t cash sitting in your account. Cash sitting in your account is just waiting. Capital is ownership of something that other people consistently need — and will keep paying for. A share of Apple isn’t a piece of paper. It’s a claim on the demand of 1.4 billion active iPhone users. A rental property isn’t a building. It’s a claim on the demand for shelter in a specific location. A YouTube channel with 200,000 subscribers isn’t a hobby. It’s a claim on audience demand that advertisers will pay to reach.

Think about that. The asset generates cash not because you’re working, but because people want what it represents.

When James was thinking about selling his index funds in October 2022, he wasn’t just selling stocks. He was selling his claim on the demand generated by hundreds of the world’s most used companies — Amazon, Microsoft, Google, Apple — at exactly the moment when everyone else’s temporary panic had discounted that claim. He was about to hand his ownership to someone who understood what ownership actually meant.

I told him that. Not gently, either.

What Contrarian Investing Actually Means

Most people think contrarian investing means being weird. Going against the grain for the sake of it. Buying things nobody else likes just to seem clever.

That’s not it. Not even close.

Real contrarian investing is simpler and harder at the same time. It means understanding the difference between permanent value and temporary sentiment — and having the stomach to act on that difference when the crowd is running the other way. It means asking “what to buy” when everyone else is asking “whether to sell.” It means thinking like an owner when the market is pricing things like a panic.

There’s a story I keep coming back to — a version of it appears in one of the books that shaped Warren Buffett’s early thinking. A man named Harry, sometime in the 1930s, watches seven people use a coin-operated scale in a pharmacy and has a single thought: I want to own that machine, not use it. He pulls $175 out of his savings account, leases three scales, and within a few months is making $98 a month. Then he does it again. And again. By the time he stops, he owns 70 machines — and the last 67 were paid for entirely by the cash flow from the first three. He didn’t work harder. He bought smarter. He asked “what should I own” instead of “what should I do.”

That’s the mentality. And it applies whether you’re buying coin-operated scales in 1932 or index funds during a market correction in 2022.

What Actually Happened to James

James didn’t sell.

I’m not going to pretend I gave him some brilliant speech that changed his life in an afternoon. Mostly I just asked him one question: “If the price of your apartment building dropped 24% tomorrow, would you immediately move out?” He laughed. Obviously not. The building still provides shelter. The demand is still there. The temporary price doesn’t change the underlying reality.

The same logic applies to equity ownership in good businesses. The crowd’s current mood doesn’t change what those businesses generate in real demand every single day.

He kept his $18,000. He actually added $400 more that month — which was real money for him, scraped together by pausing his gym membership and skipping two weekend plans. Not because I told him to. Because once he saw his investments as ownership of demand rather than a number on a screen, selling felt less like caution and more like giving something away.

By the end of 2023, that $18,000 had become roughly $27,000. Thirteen months. He didn’t do anything except not panic.

What You Should Actually Do With This

Here’s what I want you to take away — not as a theory, but as something you can act on this week.

The dividing line in building wealth isn’t intelligence. It’s not income either — I know engineers making $180,000 a year who will retire with almost nothing because they’ve been spending like owners without ever actually becoming one. The dividing line is whether you’ve switched from asking “what should I do to earn more?” to asking “what should I own that earns without me?”

You don’t have to start big. Harry started with $175 in a depression-era economy. Buffett started with lost golf balls he fished out of water hazards and sold for $6 a dozen. The amount matters less than the habit of acquiring ownership — equity in something that captures demand — instead of just accumulating cash that leaks out through a hundred monthly invoices to other people’s assets.

If you’re a salaried employee and starting from scratch, the most accessible version of this is an index fund — something like a broad market ETF that gives you fractional ownership across hundreds of demand-generating businesses at once. Automate at least 10% of every paycheck into it before you pay anything else. Not after. Before. Pay your rent late if you have to, work an extra Saturday if you have to — but get your ownership stake first. This is the contrarian move in a world where 83% of Americans are living paycheck to paycheck while simultaneously funding other people’s capital through every bill they pay.

The crowd is always moving toward comfort. Selling when it’s scary. Buying when it feels safe. Keeping their cash liquid so it “feels” like they have control. And every time they do, someone patient — someone who asked “what should I own?” — is quietly on the other side of that transaction.

This Is For You If…

You’re not a day trader. You’re not someone who checks stock prices seventeen times before lunch. You’re someone who earns a decent living, maybe a great living, and still feels like wealth is something that happens to other people — people who got lucky, or started richer, or knew the right things at the right time.

You’re the person who reads two paragraphs of most finance content and closes the tab because it either talks down to you or drowns you in terminology designed to make simple things feel complicated. You want something real. Something that actually explains why the gap between people who build wealth and people who don’t keeps widening — and what, concretely, you can do about it before another decade slips by.

If that’s you, this is the idea worth sitting with: you are already participating in the capital system every single day. Every bill you pay, every subscription you maintain, every latte you buy — you’re contributing to someone else’s equity. The only question is when you start building some of your own.

The One Thing To Remember

Contrarian investing isn’t a personality type or a trading strategy — it’s the decision to think about ownership when the crowd is thinking about safety, to ask “what should I buy?” when everyone else is asking “should I sell?”, and to understand that real wealth isn’t stored in cash but in claims on things other people need. The crowd will always move toward comfort. Wealth — actual, compounding, time-freeing wealth — almost always lives in the opposite direction.

Today: Open a brokerage account if you don’t have one. Transfer whatever you can — even $50 — before you pay your next bill. The amount is almost irrelevant. The habit of buying ownership before funding consumption is everything.

This week: Write down every recurring bill you pay. For each one, identify who owns the asset you’re paying for. This is your map of where your capital flows right now. It should make you slightly uncomfortable. That discomfort is the beginning of change.

This month: When markets feel scary and the temptation to “wait for things to stabilize” hits — remember James, remember Harry and his 70 scales, and ask yourself: is the underlying demand for what I own actually gone, or is the crowd just temporarily afraid? Nine times out of ten, it’s the crowd. Act accordingly.

🎬 Prefer watching? Check out the video version on YouTube: