Priya is 31, a senior data analyst at a mid-size logistics company in Chicago, and she called me on a Tuesday afternoon in February sounding genuinely scared. Not panicked. Not dramatic. Just quietly, specifically scared — the kind of scared that comes from sitting at your desk and realizing the thing you spent six years mastering might have a 24-month expiration date.

“They showed us the new AI pipeline in the all-hands,” she said. “It does in four minutes what my team does in four days.” She paused. “I didn’t know whether to be impressed or start updating my LinkedIn.”

Priya is smart. She earns $94,000 a year. She has a 401(k) she contributes 6% to because her company matches up to 6%, and she’s never thought much harder about it than that. She owns no stock in any AI company. She rents an apartment in Wicker Park for $1,850 a month. Every dollar she makes doing analytical work that AI is about to do faster — that dollar flows out to landlords, grocery chains, utility companies, and subscription services the moment it arrives.

She is, in the cleanest possible sense, on the wrong side of what’s coming.

I Was Priya, Except I Didn’t Even Have the Good Job

When I first started thinking seriously about money, I was 27, living in a one-bedroom that cost me $1,100 a month, and proud of the fact that I was “good at my job.” I genuinely believed that being good at your job was the mechanism. Like — if I just kept getting better at the thing I did, the financial security would follow automatically, the way compound interest supposedly works in the brochures.

Here’s the thing. I was wrong in a way that took me almost four years to fully understand.

I wasn’t building anything. I was servicing other people’s capital. Every deliverable I produced made someone else’s asset more valuable — their company, their platform, their brand. I was a very efficient component in someone else’s machine. And components don’t get equity. They get salaries. Which is fine, until the machine finds a cheaper component. Or a faster one. Or one that doesn’t need health insurance.

What finally cracked it open for me was realizing that capital isn’t money sitting in an account. Capital is stored demand. It’s the structure that holds people’s needs and turns those needs into cash flow — consistently, repeatedly, without requiring you to show up and perform every single time. A rental property is capital because people will always need somewhere to sleep. A share of Apple is capital because hundreds of millions of people are locked into an ecosystem and buy new phones every two years. A piece of a platform that companies depend on is capital. Your salary is not capital. Your salary is the price someone pays to use your time today, with no obligation to keep paying it tomorrow.

When I finally understood that distinction — really understood it, not just intellectually nodded at it — I felt genuinely embarrassed about how long I’d spent optimizing the wrong thing.

What AI Is Actually Doing to the Economy (And Why Most People Are Staring at the Wrong Part)

Every conversation I hear about AI and jobs focuses on one question: will my job survive?

That’s the wrong question.

The better question is: who owns the thing that’s replacing your job?

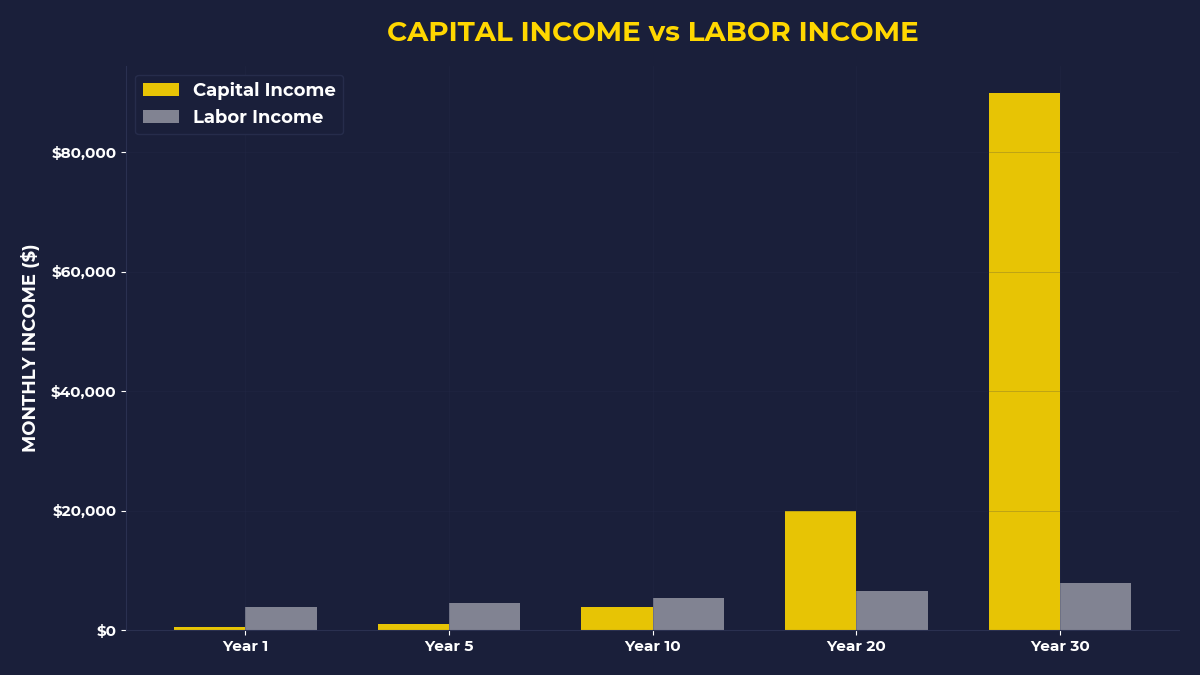

Between 2022 and 2024, Nvidia’s market capitalization went from roughly $300 billion to over $2 trillion. Microsoft, which owns a substantial stake in OpenAI, saw its valuation climb past $3 trillion. The companies building and owning the infrastructure of artificial intelligence created more wealth in 24 months than most countries produce in a decade. That wealth didn’t go to the engineers who used the AI tools. It didn’t go to the analysts whose workflows got automated. It went to the people who owned equity — actual shares, actual stakes — in the systems doing the automating.

This is not new. It’s just happening faster than it ever has before.

Think about it this way. When ATMs became widespread in the 1980s, bank tellers worried about their jobs. Some lost them. But the people who owned bank stocks — who owned a piece of the machine replacing the teller — did very well. The same pattern ran through every major technological shift: the internet, e-commerce, smartphones. There are always two groups. The people who use the new technology to do their jobs better. And the people who own a piece of the technology itself. The first group stays employed a little longer. The second group gets wealthy.

Priya is using AI to do her job better. That’s smart. That’s probably buying her a couple of years.

But she owns none of it.

What Does Owning AI Capital Actually Look Like?

This is where people expect me to say something complicated. Some special access, some insider move, some sophisticated instrument requiring a minimum investment of $250,000 and a signed document agreeing that you are a “qualified investor.”

Look. It’s not that exotic.

When Priya contributes 6% of her salary to her 401(k) — the part her company matches — and that 401(k) sits in a target-date fund, some portion of that money is probably already in Nvidia, Microsoft, Alphabet, and Amazon. She’s technically an owner. The problem is she doesn’t think of herself as one. She thinks of it as a retirement account. It doesn’t feel like capital ownership. It feels like a savings jar labeled “future.”

The reframe is this: every share of a company that benefits from AI adoption is a small piece of the system that’s replacing human labor. When that system generates revenue — when it processes a claim faster, writes a report in four minutes instead of four days, handles a customer service interaction without a human — a fraction of that revenue flows to shareholders. To owners. To people who bought a stake in the demand that AI is capturing.

You don’t have to be a venture capitalist to do this. You don’t have to pick individual stocks or predict which AI company will win. A broad index fund tracking the Nasdaq-100 — something like QQQ — was up roughly 55% between early 2023 and early 2025. That’s not a guarantee of anything going forward. But it illustrates the gap: the people who owned the index owned the AI boom. The people who just used AI tools at work got a slightly more impressive performance review.

I remember the moment I started thinking about my brokerage account differently. I was 29, sitting in my apartment, looking at a $4,200 balance that I’d been treating like emergency savings. And I thought — this is a tiny stake in the demand that powers the global economy. Every time someone buys something on Amazon, every time a business runs an ad on Google, every time a hospital uses software to manage patient records — some microscopic fraction of that transaction is mine. Because I own a piece of the structure that holds the demand.

That realization felt almost physical. Like the ground shifted slightly.

The Thing Priya Did Next (And What It Cost Her to Wait)

After our call in February, Priya did what most smart, cautious people do. She thought about it for three months. She read some articles. She told herself she’d “get serious about investing” once she’d paid down another $6,000 of student debt. She optimized her resume to emphasize her AI collaboration skills. She got a small raise in April.

She did not buy a single share of anything.

I don’t say that to judge her. I say it because I did the exact same thing for four years in my late twenties. I kept waiting for the right moment, the right amount of money, the right level of certainty. And while I waited, I paid rent to someone who owned capital. I paid my phone bill to a company whose shareholders were compounding. I bought groceries from a chain whose investors were collecting dividends. Every dollar I spent was a dollar transferred to a capital owner. Every dollar I didn’t invest was a day I didn’t spend on the right side of the ledger.

The old idea from the Kiyosaki playbook — the one I always resisted because I thought it sounded reckless — is actually just math. Pay yourself first. Before the rent check, before the grocery run, before the Netflix renewal: move money into an asset. Even $200 a month into an index fund is you buying a piece of the demand that AI is amplifying right now. It’s not going to make you rich in a year. But it puts you on the ownership side of the transaction instead of the consumption side.

And here’s the twist that makes this uncomfortable: the AI economy is specifically going to punish the people who wait. Because AI doesn’t just replace jobs gradually. It replaces entire skill categories suddenly, once a threshold is crossed. The analyst who waits until her job feels threatened to start building capital is going to be negotiating from a very weak position. The one who started three years ago — even with small amounts — has equity growing while the labor market shifts beneath her.

What You Can Actually Do This Week

Are you someone who has a brokerage account you opened two years ago and haven’t looked at since? Or a 401(k) you’ve set to autopilot without knowing what it’s actually invested in? Or money in a savings account earning 4.5% while the AI companies captured 55% of gains in a single year?

Then this is for you.

Not for the person who has $500,000 already in the market and is fine-tuning their allocation. Not for someone who needs to fix a crisis first. For the person who is vaguely aware that the AI economy is concentrating wealth somewhere, suspects it’s not concentrating toward them, and hasn’t done anything about it yet because it feels complicated and far away.

It’s not complicated. It’s just uncomfortable. Those are very different things.

The capital owners in the AI economy are not necessarily smarter than Priya. They are not necessarily better at their jobs. They are not harder workers. They are people who asked a different question. Not what should I do to earn more? but what should I own that earns while I sleep? That question sounds almost embarrassingly simple. But the gap between asking it and not asking it — measured in dollars, over twenty years — is genuinely staggering.

The One Thing To Remember

AI is not a threat to people who own AI. It is a threat to people who only work with AI while someone else collects the returns. The same technology that might automate Priya’s job is making the shareholders of the companies building it significantly wealthier every quarter — and becoming a shareholder requires nothing more than deciding to be one and then actually doing it. Capital is stored demand. AI is generating enormous demand. The question is whether you’re on the side that captures it or the side that feeds it.

- Today: Open your 401(k) or brokerage app and find out what you actually own. If it’s a target-date fund, look at its top holdings. If you see Nvidia, Microsoft, Alphabet, or Amazon, you are already a small AI capital owner. Know that. Build on it.

- This week: Set up an automatic monthly transfer — even $100, even $50 — into a broad index fund that covers the technology sector. Automate it so it happens before you see the money. The amount matters less than the habit and the timing.

- This month: Audit one recurring expense — a subscription you barely use, a service you could trim — and redirect that exact dollar amount into equity. You’re not cutting back. You’re switching sides: from paying a capital owner to becoming one.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.