My friend Priya — 31, project manager at a logistics company in Chicago — texted me a screenshot last October. It was her bank balance the morning after payday. $2,847. She’d just gotten a $6,400 direct deposit. In under 72 hours, rent, car payment, her student loan auto-draft, groceries, and a Netflix subscription had turned that deposit into enough to last two more weeks. Barely.

“I got a raise this year,” she wrote. “I don’t understand where it goes.”

I knew exactly what she meant. Not because I’m some finance wizard who figured it out early. Because I lived that same math for years and had no framework to explain why it felt like running on a treadmill someone else kept speeding up.

I Was Working Hard for Everyone Except Myself

When I was 26 and living in a one-bedroom apartment I absolutely could not afford, I genuinely believed the problem was my income. I thought if I just made more — got promoted, picked up freelance, hustled harder — the gap would close.

It didn’t close. It widened.

Every raise I got went somewhere before I could touch it. The landlord. The car lender. The credit card company with its 22% interest rate compounding quietly against me in the background. What I hadn’t understood yet — what took me embarrassingly long to see — was that I wasn’t just paying bills. I was funding other people’s capital. Every month, my cash was flowing directly into someone else’s equity. My landlord owned the building. The car company owned the loan. The credit card issuer owned the debt. I owned nothing that would ever pay me back.

Here’s the thing. I was playing the game hard. I just didn’t realize I was playing for the wrong team.

The Reframe That Changes Everything

Think about every bill you paid last month. Rent or mortgage. Car payment. Phone plan. Streaming subscriptions. Your morning coffee — even that $6.50 oat milk latte is a cash transfer to someone who owns a brand with demand behind it.

Now here’s the question I want you to sit with: who’s on the other side of those transactions?

Someone owns the building you live in. Someone owns the platform you stream on. Someone owns equity in the company whose coffee you drink every morning. That “someone” is receiving your cash outflows as their income. Your expense is their asset. Your monthly invoice is their quarterly earnings report.

Wild, right?

Capital — and I don’t mean money sitting in a savings account — is stored demand. It’s a structure that captures what people reliably need and converts that need into cash flow. Your landlord doesn’t need to show up to work Monday morning. The demand for housing does the work. Your Spotify subscription renews automatically at $10.99 whether Daniel Ek is awake or asleep. The demand for music streaming does the work. Capital is demand made permanent. And the person who owns a piece of that demand? They get paid while doing something else entirely.

This is the line. Not rich versus poor. Not lucky versus unlucky. Owners of demand versus everyone else.

Priya’s Turning Point — and Mine

I called Priya after she sent that screenshot. We talked for almost an hour. She kept coming back to the same question: “I’m doing everything right. Why does it feel like I’m going nowhere?”

I asked her one question. “What do you own that someone else pays into?”

Silence.

She had a 401(k) through work — about $18,000 accumulated over four years, mostly in a target-date fund she’d never looked at. That was it. Everything else she’d earned over her career had passed through her hands and into someone else’s.

This is where the story turns. Because Priya’s instinct, like mine used to be, was to work harder, spend less, and save the difference. Which sounds logical. It is logical. It’s also exactly what keeps you on the treadmill. Because saving cash is not the same as acquiring equity. Cash sitting in a savings account at 0.5% annual interest while inflation runs at 3.1% isn’t safety — it’s a slow leak. The math doesn’t work. And more importantly, the structure doesn’t change. You’re still just a node in someone else’s cash flow system.

What Priya needed — what I needed at 26 — wasn’t more income. It was a different question.

Not “how do I earn more?” but “what do I own that earns without me?”

The Contrarian Move Nobody Talks About

There’s a version of “contrarian investing” that gets passed around on finance Twitter — basically, buy what’s unpopular, sell what’s hot, repeat. That’s not what I mean.

The genuinely contrarian move — the one that 9 out of 10 people never make — is switching sides entirely. Stopping being the person that capital flows away from and becoming, even partially, the person it flows toward.

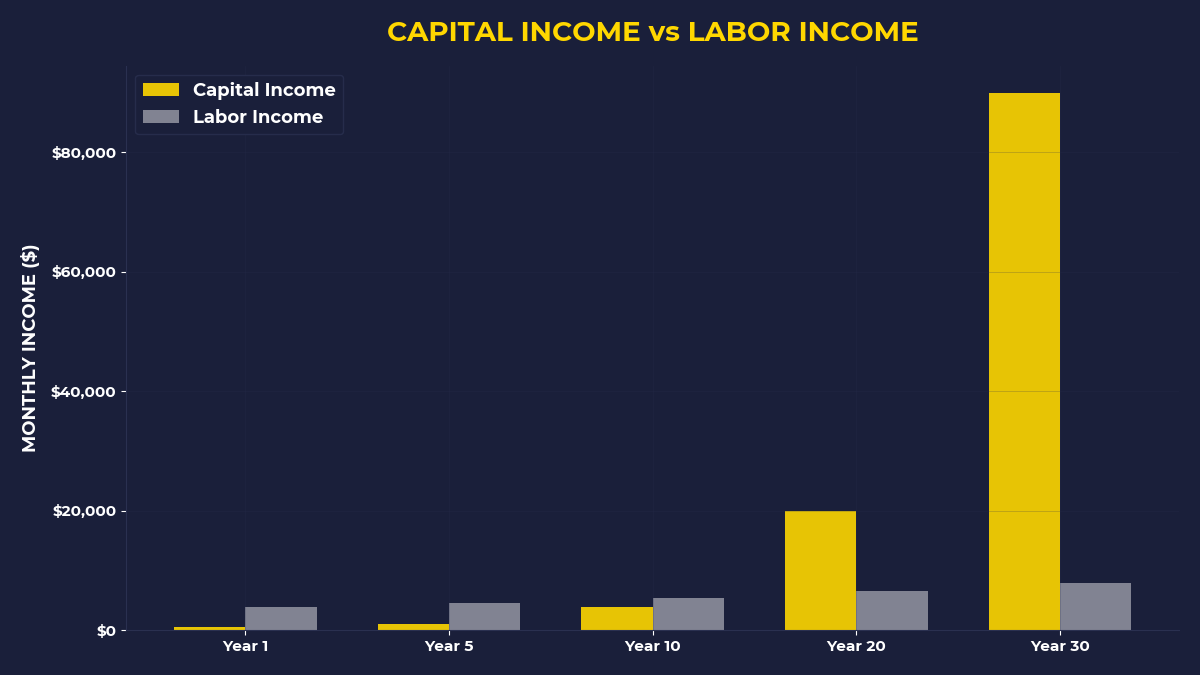

I once made the mistake of waiting until I felt “ready” to invest. Ready meant zero debt, a full emergency fund, a comfortable salary, a clear strategy. I was 29 before I started buying equity in anything meaningful. Three years I’ll never get back. If I’d started at 26 with even $100 a month going into a broad market index — something like QQQ, which tracks the 100 largest non-financial companies on the Nasdaq — and kept going consistently until today, the compounding difference would be somewhere around $34,000 at average historical growth rates. Not because $100 a month is life-changing. Because time inside a compounding structure is.

The contrarian insight is this: you don’t wait until conditions are perfect. You start acquiring equity in demand-backed assets before you feel ready, before the bills are fully paid, before the emergency fund hits the “right” number.

Look. I’m not saying don’t pay your rent. I’m saying the question most people never ask is: what am I buying this month that will still be generating value for me ten years from now?

A paycheck consumed entirely by expenses is just deferred poverty with good optics.

What Buffett Understood at Age 11

Warren Buffett bought his first stock at 11 years old. Before that, as a kid, he collected lost golf balls from the rough near a local course and resold them — 12 balls for $6. He wasn’t just working. He was thinking about what assets he could acquire with the cash, and how those assets could generate more cash without him physically present.

There’s a story I came across once about a man — call him Harry — who noticed a coin-operated scale in a drugstore. He watched eight people use it in twenty minutes. He asked the owner about it, found out the owner leased it and kept 25% of the revenue — about $20 a month. Harry withdrew $175 from his savings account and leased three machines. Within weeks he was making $98 a month. But the part that mattered came next. He eventually owned 70 machines. And 67 of those 70 were purchased entirely with the coins that came out of the first three.

He didn’t work 70 times harder. He built a structure that worked 70 times wider.

That’s the compounding Buffett talks about. Not some abstract financial concept — buying a demand-backed asset, letting it generate cash, using that cash to buy more demand-backed assets. The question was never “how hard should I work?” It was always “what should I buy?”

If This Is You, Keep Reading

If you’re someone who earns a reasonable salary, pays your bills on time, maybe has a small savings cushion, and still feels like you’re not getting anywhere — this post is for you. If you’ve read finance blogs before and bounced because they felt like they were written for someone who already had $500,000 in an investment account — this post is for you.

You don’t need to quit your job. You don’t need to start a business tomorrow. You need to change one question, and then act on the answer consistently enough that the structure starts to shift under you.

Priya did something small after our conversation. She opened a brokerage account — took her about 11 minutes — and set up a $200 automatic monthly transfer into a broad index fund before any of her other bills processed. Not after. Before. The first month she had to put $80 on a credit card to cover groceries. She hated it. But she didn’t cancel the auto-invest. The second month she adjusted her grocery budget and it evened out. By month four, it was invisible in her cash flow. A year later, she has $2,400 in equity she didn’t have before. Small. But it’s hers. And it’s on the right side of the ledger.

The One Thing To Remember

Every month you spend 100% of your income on consumption, you are funding other people’s capital while building none of your own. The contrarian investing move isn’t about stock picks or market timing — it’s about structurally becoming someone who owns a slice of what other people reliably need, and letting that ownership compound while you live your life. The gap between people who build wealth and people who don’t is rarely income. It’s whether any of their money ever switches sides.

- This week: Open a brokerage account if you don’t have one. It takes under 15 minutes. Set up a recurring $100–$200 auto-investment into a broad equity index before your bills process — not after. The discomfort you feel is the point.

- This month: Write down every recurring bill you paid last month. Next to each one, write the name of who owns the asset on the other side. Your landlord. Your car lender. Your phone carrier. Let that list sit with you. Then ask: what am I on the other side of?

- This year: Find one asset with real demand behind it — a stock, an index fund, a small side project with a monetizable audience — and put consistent money into it every single month for 12 months without stopping. Not because you’ll be rich in a year. Because you’ll have built the habit of switching sides.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.