My friend Rachel — 31, marketing manager in Chicago — called me on a Tuesday night about two months after getting a raise. Not to celebrate. To vent.

“I make $74,000 a year now,” she said. “I did everything right. I got promoted. And I still feel like I’m losing.”

She wasn’t wrong. Her rent had gone up $200 the same month her raise kicked in. Her student loan payment resumed. Her car needed new tires. By the time April landed, her $6,000 raise had translated to roughly $180 extra per month after taxes and new costs. A hundred and eighty dollars. She’d worked harder than anyone in her department for three years for $180.

What she was describing wasn’t a budgeting problem. It wasn’t a discipline problem. It was a philosophy problem. And almost nobody talks about it that way.

I Was Rachel for Most of My Twenties

Look, I’m not going to pretend I figured this out early. I was 27, living in a one-bedroom apartment, staring at a spreadsheet I’d made called “Where Does My Money Go.” I had color-coded categories. I was proud of it. I thought the answer to my financial anxiety lived inside that spreadsheet somewhere — if I could just optimize hard enough, the numbers would stop scaring me.

They didn’t.

Every personal finance book I read told me what to do. Wake up earlier. Track every dollar. Cut the lattes. Get a side hustle. Automate your savings. I did most of those things. And they helped — a little. Marginally. The way a better pair of shoes helps when you’re running in the wrong direction.

The problem wasn’t my behavior. The problem was my question. I was asking what should I do to get ahead? when the actual question — the one that changes things — is what should I own?

That sounds like a subtle distinction. It is not.

The Reframe That Broke My Brain (In a Good Way)

Here’s the thing. Every single month, Rachel sends money to capital owners. Her rent check goes to whoever holds the deed on her building. Her Netflix subscription goes to shareholders. Her grocery bill feeds into the equity of a handful of publicly traded food conglomerates. Her car payment enriches a finance company. Even the $4.75 she spends on oat milk lattes flows upward, toward someone who owns a piece of the supply chain that made it possible.

Think about that.

Rachel isn’t poor. She earns $74,000 a year. But every day — every single ordinary Tuesday — she wakes up and participates in a system that automatically transfers her earned cash to people who own things. She’s on the paying side of the ledger. The question is whether she’ll ever get to the receiving side.

Capital isn’t money sitting in a bank account. Capital is stored demand. It’s the ownership of something people need — reliably, repeatedly, over time. When you own a piece of something people keep paying for, you collect. When you don’t, you pay. That’s the whole game, spelled out in one sentence.

I know, I know. This sounds obvious when you say it like that. But here’s why it doesn’t feel obvious: we’re taught from birth to think about wealth as a reward for effort. Work hard, get ahead. Study more, earn more. Grind longer, win bigger. The entire self-help industrial complex — and there are tens of thousands of books on Amazon right now reinforcing this — is built on the premise that the answer to your financial life is found in what you do.

It isn’t. The answer is found in what you own.

The Golf Ball That Explains Everything

There’s a well-documented story about Warren Buffett as a kid — around age 10 or 11 — collecting lost golf balls near his neighborhood course and reselling them for about 50 cents each. Classic hustle. Kid works, kid earns money. Fine.

But the interesting part isn’t the golf balls. The interesting part is what a young Buffett reportedly did next. He didn’t keep hustling golf balls forever. He used that early cash to buy a used pinball machine and place it in a barbershop. Then another machine. Then another location. He stopped trading his time for dollars and started deploying assets that collected money while he was elsewhere. By the time he was a teenager, he had an income stream that didn’t require him to get muddy fishing golf balls out of a pond.

The pivot wasn’t from laziness to hustle. It was from doing to owning.

Here’s an even cleaner version of this idea. There’s an old story — likely from a 1930s-era book on wealth — about a man named Harry who wandered into a drugstore and noticed a coin-operated scale near the entrance. He dropped a penny in, checked his weight, and then stood there for a few minutes watching. Seven other people used it. He asked the store owner about it. Turns out the owner leased the scale and kept 25% of the coin revenue — about $20 a month in that era.

Harry went home, pulled $175 from his savings, and leased three scales.

Within a few years, he owned 70 of them — and critically, 67 of those were purchased using the cash flow from the original three. He didn’t go back to work harder at his job to fund more scales. The scales bought more scales. That’s compound ownership. That’s what Buffett means when he talks about compounding — it’s not a math trick, it’s a structural reality. You buy something that generates cash. You use that cash to buy more things that generate cash. Repeat until the incoming cash covers your life.

Rachel has never thought this way. Not because she’s not smart — she’s one of the sharpest people I know. But because nobody ever asked her the right question.

What Happens When You Finally Ask “What Should I Buy?”

When I started asking this question — genuinely, not rhetorically — everything shifted.

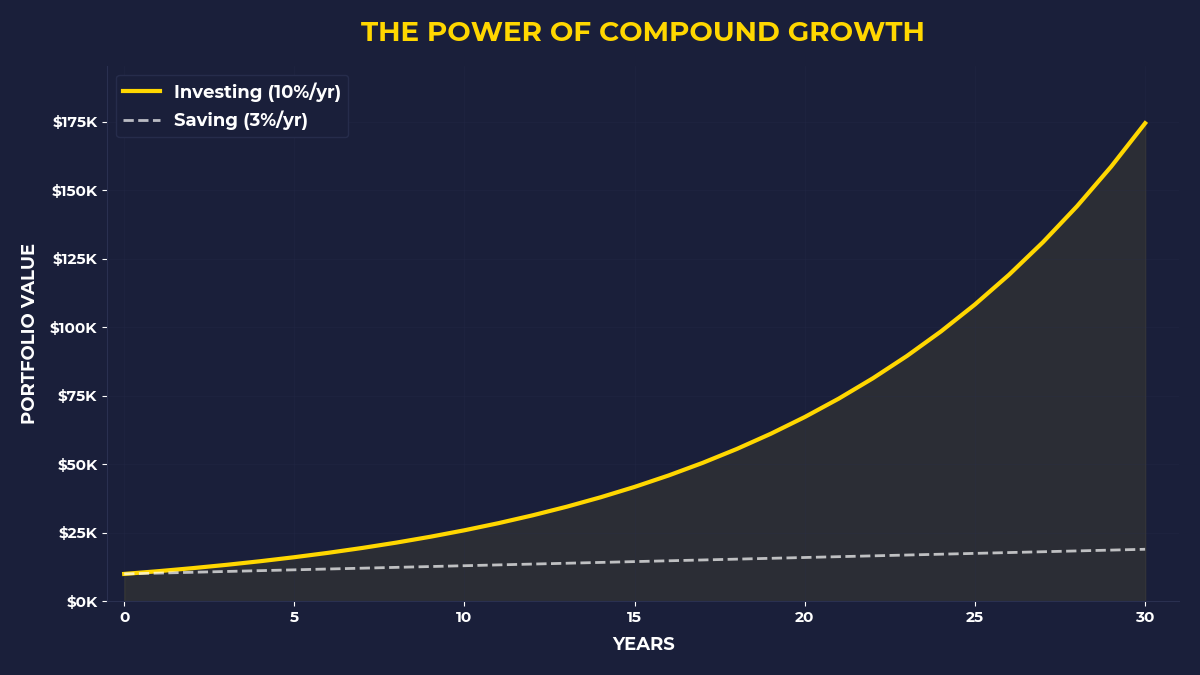

I was 29 when I opened my first brokerage account. I remember sitting on my couch, laptop open, feeling faintly ridiculous. I had $400 to invest. Four hundred dollars. I’d read enough to know I wanted equity — actual ownership stakes — not a savings account that paid 0.01% annually while inflation quietly erased 3% of my purchasing power every year. So I bought a small position in a broad index fund that tracked the 100 largest technology companies. Not because I had some genius insight. Because those companies collectively represented something billions of people used every day — and would keep using.

It wasn’t glamorous. It was $400.

But something changed in how I thought about every dollar after that. Not “how do I spend this wisely?” but “how do I use this to get to the receiving side of a transaction?” I started thinking about every purchase differently — not with guilt, but with awareness. The question wasn’t should I cut this expense? It was is this dollar going out permanently, or can I route some of it toward ownership?

That’s a different relationship with money entirely.

What This Actually Looks Like on a Tuesday

Do you have to quit your job, start a business, and become an entrepreneur to participate in this? No. Absolutely not.

The most accessible version of “buy demand” is to own a small piece of companies whose products people can’t seem to stop using. A broad ETF — basically a basket of stocks you can buy in one transaction, like buying a slice of hundreds of companies at once — gives you fractional ownership in the demand-generating machines of the modern economy. When Microsoft sells another enterprise subscription, when a consumer goods company moves another billion dollars of products through a grocery chain, when a payments processor handles another trillion in transactions — you participate in that. Not dramatically. But structurally.

The minimum viable version of this: before you pay a single bill this month, move $100 into a brokerage account and buy something. Not after the bills are paid. Before. The psychological shift of prioritizing ownership over consumption is the actual habit that matters. Even if $100 feels trivial — and it will feel trivial — the behavior is what you’re training. You are practicing being on the other side of the transaction.

If that feels reckless — if you’re thinking “what if I can’t cover my expenses?” — that discomfort is exactly worth sitting with. Because Rachel’s raise bought her $180 of breathing room, and she spent it all in the first two weeks without even noticing. The money that would have gone to ownership just… dissolved. It always does, until you intercept it first.

This Is for a Specific Kind of Person

If you’re someone who has read twelve personal finance books and still feels like you’re running in place — this is for you. If you’ve gotten raises that disappeared. If you track your spending but still feel like the system is tilted against you. If you’re competent and hardworking and a little bit furious that none of that seems to translate into financial momentum.

You’re not doing it wrong. You’re answering the wrong question.

The hustle gurus want you to ask what should I do? That question keeps you on the labor side of the economy — adding value, getting paid, spending it, repeating. It’s not nothing. But it doesn’t build. The capital question — what should I buy? — is the one that quietly repositions you from the paying side to the collecting side, one small ownership stake at a time.

Wild, right? That the entire shift comes down to which question you’re asking.

The One Thing to Remember

Every day you wake up and spend money, you are either paying someone who owns something, or you are someone who owns something that’s being paid. That’s it. The whole wealth equation, in one sentence. Rachel is smart, hardworking, and currently on the wrong side of that equation — but not permanently. The moment she routes even $100 a month toward ownership, she starts crossing over. It won’t feel like much at first. The math is slow before it’s fast. But the direction matters more than the amount, especially at the beginning.

Before you pay a single bill this month, transfer at least $100 into a brokerage account and purchase a broad equity index fund. Do it first. Today if possible. The bills will get paid — they always do.

Write down every recurring payment you make — rent, subscriptions, car, utilities. That list is a map of who owns things you depend on. Your job is to slowly get onto that list, on the ownership side, for things other people depend on.

Ask “what should I buy?” once a week, not “what should I do?” Even if you only have $50 free. The question trains the mindset. The mindset determines the decade.

🎬 Prefer watching? Check out the video version on YouTube: