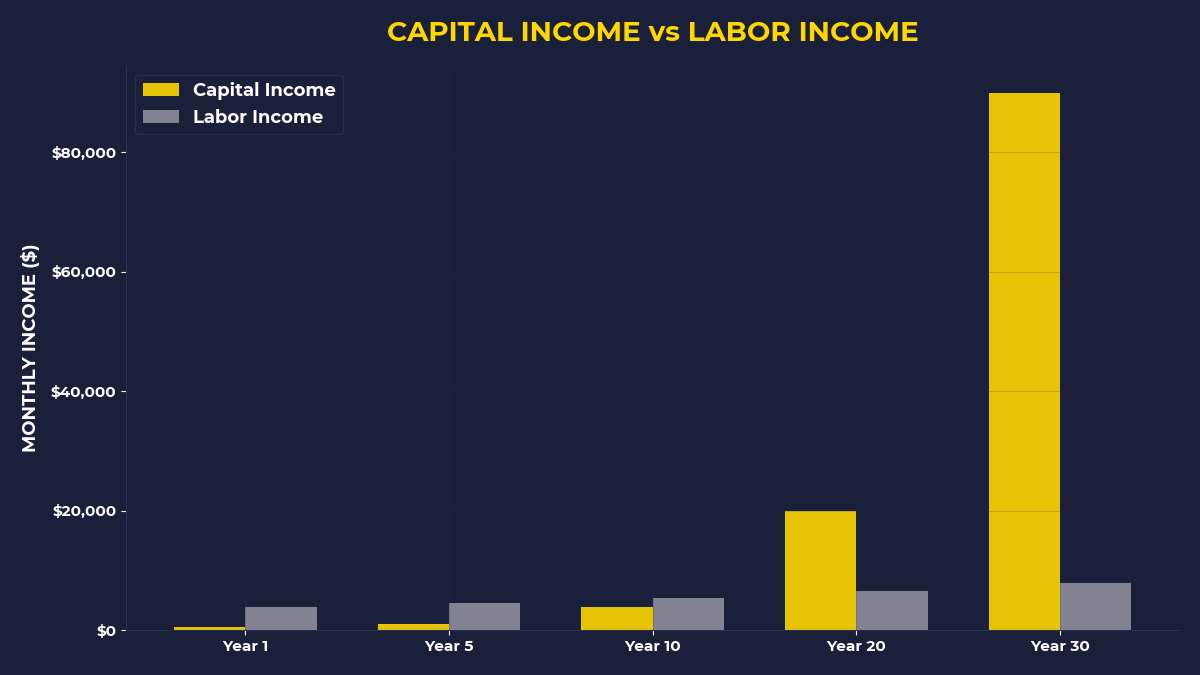

The Monthly Money Migration

Sarah — 29, marketing coordinator in Denver — gets paid every other Friday. By Sunday night, 73% of her paycheck is already gone.

Not to groceries or gas or anything fun. To other people’s capital.

Her $3,200 paycheck lands in her checking account at midnight. Before she’s had her first cup of coffee, the automatic transfers start. Rent: $1,400 to her landlord’s real estate portfolio. Car payment: $380 to Toyota Financial. Student loan: $240 to Navient. Health insurance: $190 deducted before she even saw the money. Phone bill: $85 to Verizon’s shareholders.

That’s $2,295 flowing directly from her labor to someone else’s capital. And she hasn’t bought a single thing for herself yet.

Sarah works 40 hours a week to fund other people’s wealth-building machines.

I Used to Be Sarah’s ATM Too

I know exactly how this feels because I was trapped in the same cycle for years.

When I was 26, I made $52,000 as a junior analyst. I thought I was doing well — first job out of college, steady paycheck, “building my career.” My parents were proud. My friends were impressed.

But every month, I watched my paycheck get carved up like a Thanksgiving turkey. Rent ate 35% before I touched it. Student loans took another 12%. Car payment, insurance, utilities, groceries — by the time I’d covered basic survival, maybe $300 was left for “building wealth.”

I remember sitting in my studio apartment one Sunday, watching Netflix (another $15/month to their shareholders), realizing something that made my stomach drop.

My entire financial life was designed to make other people rich.

Every single monthly payment was flowing upward — from my labor to someone else’s capital. I was working full-time as a wealth transfer mechanism.

The Contrarian Money Flow

Here’s the thing most people never see: **the order matters**.

Sarah pays her landlord first, then figures out what’s left. She funds Toyota’s profits, then sees if she can afford to build her own wealth. She pays Verizon’s shareholders before she pays herself.

Every financial advisor will tell you to “pay yourself first.” But they never explain why most people find this impossible to do.

Because the entire system is designed to extract your money before you get it.

Think about that grocery bill you just paid. Before you even left the store, your money was already flowing to the shareholders of Coca-Cola, Procter & Gamble, Nestlé, and a dozen other corporations. Your rent check went straight to a property management company that owns 847 units across three states.

Your car payment? That’s funding Toyota’s $23 billion in annual profits.

Your Netflix subscription joins 230 million other monthly payments flowing to their capital base.

You’re not just paying for products and services. You’re funding other people’s equity positions.

The Capital Owner’s Perspective

What if I told you there’s another side to this equation?

Somewhere in Austin, a 34-year-old named Marcus owns 1,200 shares of Netflix. Every month, Sarah’s $15 — along with 229,999,999 other $15 payments — flows into the company that Marcus owns a piece of.

Marcus doesn’t work at Netflix. He doesn’t create content or manage servers. But Sarah’s entertainment budget helps fund his investment returns.

Marcus also owns a duplex in Denver. Sarah’s friend Jake rents the other half for $1,350/month. Marcus bought the property in 2019 for $380,000 with 20% down. Jake’s rent covers the mortgage, taxes, and insurance, plus gives Marcus $200/month in cash flow.

Jake works 42 hours a week at a software startup. Marcus owns one building and gets paid while he sleeps.

Same city. Same economy. Different relationship to capital.

Why Smart People Stay on the Wrong Side

The most dangerous trap in building wealth is thinking your labor is your biggest asset.

Sarah is smart. She works hard. She’s responsible with money. But she’s optimizing the wrong variable.

She’s focused on earning more from her job — asking for raises, building skills, maybe switching companies for a 15% bump. Meanwhile, 73% of every paycheck flows to capital owners whether she makes $45,000 or $75,000.

The percentage barely changes. The recipients just get richer.

I made the same mistake for three years. I thought career progression would solve my money problems. I worked nights and weekends, earned my CFA, switched jobs twice. My income went from $52,000 to $78,000.

Know what happened to my wealth? Almost nothing.

Because I was still sending most of my money to capital owners first, then trying to build wealth with whatever scraps remained.

The Contrarian Flip

What if you could reverse the flow?

True contrarian investing isn’t about buying stocks when everyone’s selling. It’s about refusing to participate in the wealth transfer system that keeps you broke.

It’s about becoming Marcus instead of staying Sarah.

Look at your last three months of expenses. Every payment you made went to someone who owns something. Your landlord owns real estate. Netflix owns intellectual property. Verizon owns infrastructure. Apple owns technology platforms.

They all have one thing in common: they capture recurring demand.

Sarah needs a place to live every month. Jake needs internet every month. I need coffee every morning. That recurring demand — multiplied by millions of people — becomes predictable cash flow.

Predictable cash flow becomes valuable capital.

Capital that you can own pieces of.

The Demand Ownership Strategy

Here’s what I wish someone had told me at 26: **stop working for money, start buying demand**.

Instead of asking “how can I earn more?” ask “what can I own that other people need?”

You don’t need to start a company or buy rental properties. You can own pieces of the same companies you’re already paying.

Sarah’s $15 Netflix payment? She could own 0.07 shares of Netflix stock instead of just funding someone else’s shares.

Her $380 car payment? She could own Toyota stock and get paid from her own car loan.

Her $1,400 rent? She could own shares of Real Estate Investment Trusts (REITs) and collect a portion of everyone else’s rent payments.

Every bill you pay represents demand that you could own instead of just fund.

This isn’t about cutting expenses. It’s about changing which side of the transaction you’re on.

My $427 Experiment

Three years ago, I started an experiment. Every month, before I paid any bill — rent, groceries, car insurance, anything — I moved $427 into my brokerage account.

Even when it meant scrambling to cover rent. Especially then.

I bought shares of companies I was already paying: Apple, Microsoft, Verizon, Coca-Cola, the REIT that owned properties in my area. Every purchase meant I owned a tiny piece of the demand I was creating.

Some months were brutal. I ate ramen and cancelled subscriptions to make the numbers work. But here’s what happened:

After 18 months, my “bills” started paying me back.

The $427 monthly investments had grown to $8,900 in stock value. More importantly, I was receiving $23/month in dividends — money that arrived whether I worked or not.

That’s when I understood the contrarian insight that changes everything.

Capital Is Stored Demand

Money sitting in your checking account does nothing. Money flowing to bills just disappears.

But money used to buy pieces of recurring demand? That becomes capital that works while you sleep.

Every person needs housing, food, transportation, entertainment. That need creates predictable cash flows. Those cash flows get captured by companies and real estate owners.

You can own pieces of those cash flows.

The contrarian move isn’t timing the market or finding the next Tesla. It’s refusing to just fund other people’s capital and instead becoming a capital owner yourself.

Even if it’s just $50/month. Even if it feels impossible.

Especially then.

If You’re Someone Who Sends 70% of Your Paycheck to Capital Owners…

This post is for you if you’ve ever looked at your bank statement and wondered where all your money went.

If you work hard but never seem to get ahead financially.

If you’re tired of funding everyone else’s wealth while struggling to build your own.

If you’ve realized that earning more doesn’t automatically mean keeping more.

You don’t need a business degree or a trust fund to flip this equation. You just need to refuse to participate in the current system.

The One Thing to Remember

**Every dollar you send to capital owners is a dollar you could have used to become one yourself**. The system is designed to extract your money before you see it, but you can reverse the flow by owning pieces of what everyone needs. Start small, start today, but start owning demand instead of just funding it.

- Open a brokerage account this week — Fidelity, Schwab, or Vanguard all work.

- Move $50 before paying your next bill — before rent, groceries, or car payment.

- Buy one share of something you already pay for — if you have an iPhone, buy Apple; if you pay rent, buy a REIT.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.