Every month, a parade of invoices arrives. Mortgage. Utilities. Car payment. Groceries. Insurance. Netflix. Each represents a claim on your future labor before you’ve even performed it. What most people miss is this: **every bill is a wealth transfer to someone who owns something you need**. The coffee shop owner captures your morning ritual. The landlord captures your shelter requirement. The cell phone company captures your communication need.

This isn’t accidental. It’s the fundamental architecture of capital distribution. Your paycheck represents stored labor—time you’ve already surrendered. But before that stored labor reaches you, it gets carved up by people who positioned themselves between you and your basic needs. They own the infrastructure of your daily existence.

The primitive brain sees bills as unavoidable friction. The contrarian investor sees them as a map of where wealth flows. Every recurring payment reveals a capital position someone built to intercept your cash flow. The question isn’t how to minimize these payments—it’s how to position yourself on the receiving end.

The Invoice Parade: Your Money’s First Destination

Let’s trace where your paycheck actually goes. Housing claims 25-35%. Transportation captures another 15%. Food takes 10-15%. Before you’ve bought anything discretionary, 60% of your income has already transferred to asset owners. The mortgage payment goes to the bank that owns your debt. The rent goes to someone who owns your building. The car payment goes to the finance company that owns your loan.

This isn’t just cash flow—it’s a wealth concentration mechanism. Every month, your labor converts into their equity. The landlord uses your rent to pay down the mortgage, building equity in property. The bank uses your interest payments to fund more loans, expanding their capital base. The utility company uses your payments to maintain and expand infrastructure that generates more recurring revenue.

Robert Kiyosaki discovered this pattern during his most desperate period in the 1980s. Living in a friend’s garage after his business collapsed, he made a counterintuitive decision. Instead of paying bills first and investing with whatever remained, he inverted the sequence. He invested in assets first, then worked additional jobs to cover the bills. This forces scarcity thinking onto expenses while abundance thinking onto assets.

The Recency Bias Trap: Why Emergency Funds Keep You Poor

Recency bias drives most financial advice. The recent memory of economic uncertainty makes “emergency funds” seem prudent. But emergency funds are wealth transfers in disguise. Your savings account earning 0.5% loses purchasing power to inflation while banks lend that same money at 7-15% for mortgages and credit cards.

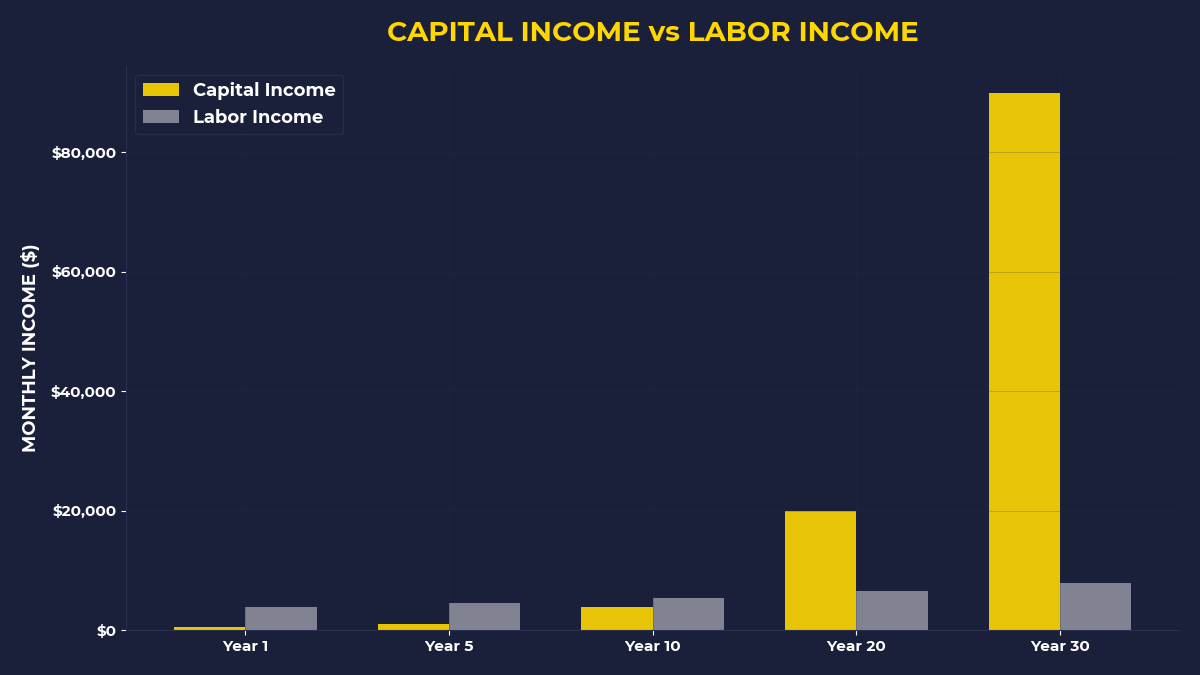

Meanwhile, the S&P 500 has averaged 10% annually over decades. A $10,000 emergency fund sitting in savings for ten years becomes $10,500. The same $10,000 invested in equity markets becomes $26,000. The “safe” choice costs you $15,500 in opportunity—money that instead accrued to bank shareholders and borrowers who understood leverage.

The contrarian approach: maintain minimal cash for true emergencies (1-2 months expenses), then redirect everything else toward ownership positions. The primal brain fears volatility. The investor brain recognizes that inflation is guaranteed wealth destruction while equity ownership offers asymmetric upside.

From Bill Payer to Bill Receiver: The Ownership Flip

Warren Buffett’s childhood golf ball business illustrates the flip from payer to receiver. Young Warren collected lost golf balls, cleaned them, and sold them in sets. But the real lesson isn’t in the hustle—it’s in what he did with the profits. Instead of spending on consumption, he reinvested in assets that generated cash flow without his direct labor.

The scale principle applies to modern investing. Buy shares of companies that collect the bills you pay. Own Procter & Gamble stock to capture profits from consumer goods purchases. Own Realty Income Corporation to collect commercial rent. Own Visa to earn from every transaction. Instead of just paying for services, own pieces of the companies providing them.

This isn’t about picking individual stocks—it’s about understanding cash flow direction. When you own broad market ETFs like VTI or QQQ, you own fractional interests in thousands of companies collecting bills from millions of people. Your position captures the aggregate wealth transfer instead of just contributing to it.

The Compound Effect of Ownership

Harry Larson’s weight scale story from the 1930s demonstrates compound ownership. After observing customers pay to use a drugstore’s coin-operated scale, Larson bought three scales and placed them in high-traffic locations. The monthly income from these assets allowed him to buy more scales. Eventually, he owned 70 machines generating $1,750 monthly—without his physical presence.

Modern equivalent: dividend growth investing. Companies like Johnson & Johnson have increased dividends for 60+ consecutive years. Each dividend payment can purchase additional shares, which generate larger future dividends. The compounding happens automatically through ownership, not through your continued labor.

The Leverage Question: What To Buy, Not What To Do

Most success literature asks “What should I do?” The capital owner asks “What should I buy?” This distinction separates linear wealth building from exponential wealth building. Doing things trades time for money at fixed ratios. Buying assets creates systems that generate returns independent of your time investment.

Consider a simple example: launching a blog. The “what to do” approach focuses on writing more posts, building an audience, creating content. The “what to buy” approach focuses on acquiring domains with existing traffic, purchasing email lists, buying profitable websites with established revenue streams. Both can succeed, but ownership acceleration is faster.

For wage earners, the immediate application is systematic asset purchase. Allocate the first 20% of each paycheck to buying ownership positions before paying any discretionary bills. This forces you to optimize expenses while accumulating capital. The monthly investment constraint creates beneficial scarcity on spending while abundance thinking on wealth building.

The Side Project Multiplier

Side projects offer the fastest path from wage earner to capital owner. But approach them through the ownership lens. Instead of trading more hours for more dollars, create systems that generate revenue without proportional time investment. Digital products, affiliate marketing, rental properties, or small businesses with employees all offer leverage potential.

The key metric isn’t hourly earnings—it’s the ratio of income to time invested. A side project generating $500 monthly with 5 hours of maintenance beats a part-time job paying $15/hour for 40 hours. The side project creates optionality; the part-time job just extends wage slavery.

Breaking the Transfer Pattern: Structural Positioning

The wealth transfer system isn’t broken—it’s working exactly as designed. Capital flows from people who spend to people who own. The system rewards patient accumulators and punishes immediate consumers. Understanding this structure reveals the exit path.

Structural positioning means arranging your finances so cash flows toward ownership rather than consumption. Automate investments before discretionary spending becomes possible. Use debt strategically to acquire appreciating assets while minimizing debt for consumption. Choose housing, transportation, and lifestyle with cash flow impact as the primary criterion.

The goal isn’t to minimize all bills—it’s to position yourself as both bill payer and bill collector. Pay rent while owning REIT shares. Pay for groceries while owning consumer staples stocks. Pay insurance premiums while owning insurance company equity. This hedges your consumption costs against inflation while capturing the profit margins of companies serving those needs.

What The Primal Investor Takes Away

Every bill represents a wealth transfer to capital owners—position yourself to receive these transfers through ownership stakes

Recency bias makes emergency funds feel safe while inflation guarantees wealth destruction—minimize cash, maximize ownership positions

Ask “what should I buy?” instead of “what should I do?”—ownership creates leverage while labor creates linear returns

Systematic investment before discretionary spending—forces beneficial scarcity on expenses while building capital accumulation habits

Side projects should create systems, not additional wage labor—optimize for income-to-time ratios rather than absolute earnings

Hedge consumption costs through ownership stakes—own pieces of the companies collecting your bills

The primitive response to bills is to minimize them. The investor response is to collect them. Your paycheck vanishes because other people positioned themselves between you and your needs. The contrarian path is positioning yourself between other people and their needs—through ownership stakes in the businesses serving those needs. Every dollar that flows away from you should eventually flow back through your equity positions.

🎬 Prefer watching? Check out the video version on YouTube: