Marcus — 29, software developer in Denver — got his credit card statement last Tuesday and did something that would horrify his parents. The balance was $2,847. His checking account held $1,200. His next paycheck wouldn’t hit for eight days.

Instead of scrambling to cover the minimum payment, he opened his brokerage app and bought $200 worth of index funds.

His girlfriend thought he’d lost his mind. His roommate called him reckless. But Marcus had figured out something that 97% of people never learn: real contrarian investing isn’t about picking unpopular stocks when the market crashes. It’s about buying assets when you’re personally broke while everyone around you pays bills first.

The Day I Learned Everything Backwards

I used to be the responsible one.

Every month, like clockwork: rent first, utilities second, groceries third, car payment fourth. Whatever was left over — if anything — went into savings. I felt virtuous about it. Responsible. Adult.

Then I read about Robert Kiyosaki living in a friend’s garage. The man who would later write Rich Dad Poor Dad was essentially homeless. But here’s what haunts me: even while crashing on someone’s floor, he paid himself first. Every dollar that came in, he invested in assets before touching a single bill.

When creditors called, he worked extra jobs — cleaning offices, mowing lawns, whatever it took to cover the bills after he’d already invested in his future.

That story broke my brain.

Why Your Bills Are Someone Else’s Paychecks

Think about yesterday. You probably sent money to a dozen different capital owners without realizing it.

Your rent check went to someone who owns real estate. Your car payment went to someone who owns debt. Your Netflix subscription, your grocery bill, your coffee run — every single purchase transferred your cash flow to someone who owns the thing you need.

Here’s what clicked for me: those bills aren’t just expenses. They’re invoices from people who already figured out the game.

The landlord doesn’t work for rent money. The bank doesn’t work for loan payments. They own assets that generate demand, and your paycheck flows to them automatically.

Most people spend their entire lives on the wrong side of that equation.

The Contrarian Investing Strategy Nobody Teaches

Real contrarian investing means doing the opposite of what broke people do with money.

Broke people pay bills first, invest what’s left over. Capital owners invest first, figure out bills later.

Broke people avoid debt. Capital owners use debt to buy assets that other people pay for.

Broke people save for emergencies. Capital owners create systems that eliminate emergencies.

Look, I’m not saying skip rent and become homeless. But I am saying that if you’re waiting until you have “extra” money to invest, you’re playing someone else’s game by their rules.

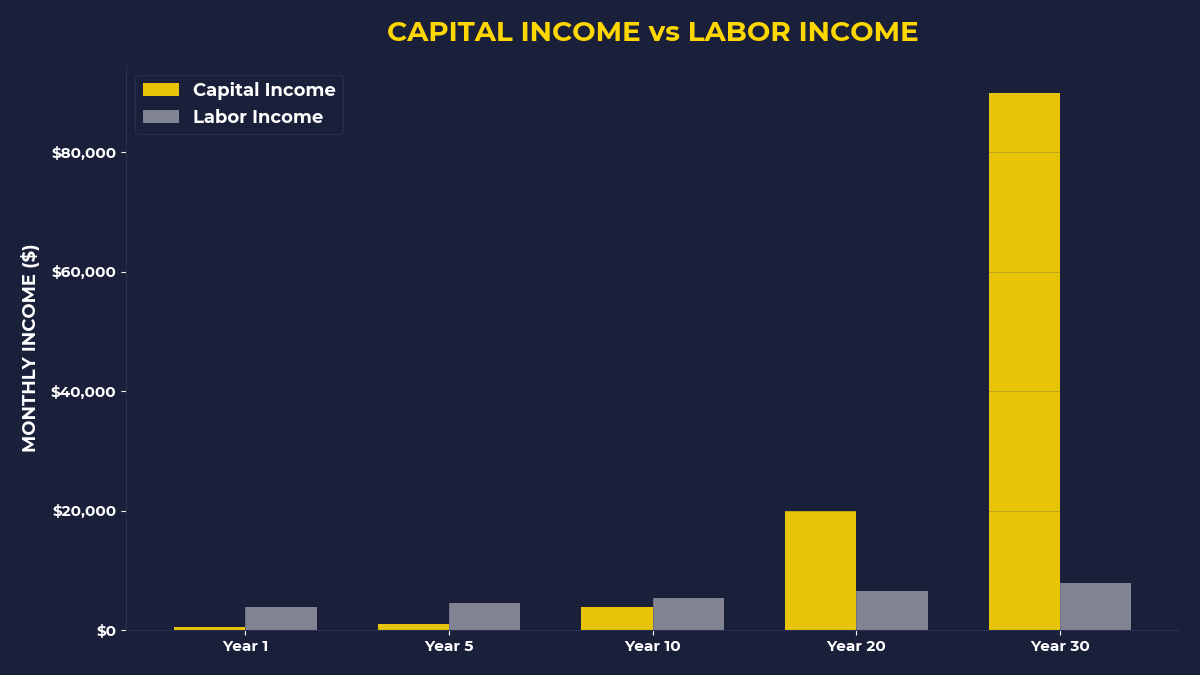

Marcus figured this out. Even with credit card debt hanging over him, he understood that $200 invested today becomes the foundation for everything else. That index fund doesn’t care about his debt-to-income ratio. It just grows.

What Happened When I Flipped The Script

Three years ago, I started an experiment. Every month, before I paid a single bill, I moved $300 into investments. Stocks, index funds, whatever — the point wasn’t perfection, it was sequence.

Some months, this meant scrambling. I delivered food on weekends to cover groceries. I sold stuff I didn’t need. I got creative with meal planning and entertainment.

But something interesting happened.

The stress of covering bills after investing forced me to examine every expense. I canceled subscriptions I’d forgotten about. I negotiated better rates. I found ways to earn extra income that I never would have pursued if I’d felt comfortable.

More importantly, watching that investment account grow — even slowly — changed how I thought about money. Instead of seeing dollars as things to spend, I started seeing them as seeds that could become trees.

Are You Asking The Wrong Question About Money?

Most people ask: “What should I do to make more money?”

That’s a labor question. It assumes your time and effort are your primary assets. It leads to side hustles, skill upgrades, resume optimization — all good things, but they keep you in the trading-time-for-money trap.

Capital owners ask a different question: “What should I buy?”

They’re not thinking about working harder. They’re thinking about owning something that generates demand. Something people need, want, or use repeatedly.

Warren Buffett figured this out as a kid selling golf balls. He didn’t just find balls and sell them. He created a system where other kids found balls, he bought them for less than he could sell them for, and he scaled that system.

The question wasn’t “How can I work harder finding golf balls?” It was “How can I own more of the golf ball demand?”

The Asset That Nobody Teaches You To Buy

You don’t need to start a business to think like a capital owner.

When you buy shares of Apple, you own a tiny piece of the demand for iPhones, iPads, and App Store purchases. Millions of people send Apple money every day, and a microscopic fraction of that flows to you.

When you buy index funds, you own pieces of hundreds of companies that employ thousands of people working to generate profits that partially belong to you.

When you buy real estate, you own the demand for shelter in that location.

The asset nobody teaches you to buy is other people’s productive effort. Not their time — their systems, their innovations, their value creation.

Most people work within other people’s systems. Capital owners collect a percentage of everyone working within the systems they own.

The 3 A.M. Realization

Marcus called me at 3:17 A.M. last month.

“Dude, I just figured something out,” he said. “I’ve been thinking about this all wrong.”

He’d been tracking his expenses for six months since starting his pay-yourself-first experiment. The numbers told a story he hadn’t expected.

“I always thought I was broke because I didn’t make enough money,” he said. “But I wasn’t broke because of my income. I was broke because 100% of my income was already spoken for by other people.”

His rent payment went to his landlord’s mortgage and profit. His car payment went to the bank’s profit margin. His credit card interest went to shareholders of financial companies.

“Every dollar I earned was already promised to someone who owned something I needed,” he said. “I was just the delivery mechanism.”

That’s when it clicked for both of us. Building wealth isn’t about earning more money. It’s about intercepting some of your own cash flow before it reaches other people’s pockets.

If You’re Someone Who Feels Stuck

This post is for you if you make decent money but never seem to get ahead. If you budget carefully but still live paycheck to paycheck. If you’ve been telling yourself you’ll start investing when you have more financial cushion.

It’s for you if you’re tired of sending your paycheck to landlords, banks, and credit card companies while building nothing for yourself.

It’s not for you if you’re looking for stock picks or market timing strategies. This isn’t about finding the next Tesla or predicting the next crash.

This is about rewiring your relationship with money from the ground up.

The One Thing To Remember

Contrarian investing isn’t about buying unpopular stocks. It’s about becoming the person who receives cash flow instead of just sending it. Every month you wait for the “right time” to invest is another month you’re funding other people’s assets instead of building your own. The right time was yesterday. The second-best time is today, even if today feels impossible.

Your next three moves:

Calculate your monthly cash outflow — add up every recurring payment that goes to someone else’s pocket (rent, car payment, subscriptions, debt payments)

Choose your interception amount — decide on a dollar figure to invest before paying any bills next month, even if it’s just $25

Open a brokerage account today — not next week, not next month, today — and buy your first piece of productive assets, even if it’s just a few dollars of an index fund

🎬 Prefer watching? Check out the video version on YouTube: