The $1,200 Decision That Reveals Everything

Sarah — 29, marketing coordinator in Denver — got her tax refund on a Tuesday morning. $1,247 sitting in her checking account like a small miracle.

She opened her banking app three times that day. The first time, she mentally paid down her credit card. The second time, she pictured finally starting that emergency fund she’d been promising herself since college. The third time, she was scrolling through flights to Barcelona.

By Friday, she’d booked the trip.

Sarah isn’t reckless with money. She pays her bills on time, contributes to her 401k, and genuinely wants to build wealth. But when faced with $1,247 of unexpected cash, her brain made the decision for her before her rational mind even had a chance.

Here’s the thing: Sarah’s brain was doing exactly what it was programmed to do over thousands of years of human evolution. And that programming is why 64% of Americans can’t cover a $400 emergency, even when they earn decent salaries.

I Used To Think I Was Just Bad With Money

I spent my twenties making the same mistakes as Sarah, just with different amounts and different purchases.

Every windfall — bonus, tax refund, birthday cash from relatives — disappeared into something I could enjoy immediately. A new laptop when my old one worked fine. Dinners at restaurants I couldn’t actually afford. A gym membership I’d use for exactly six weeks.

I convinced myself I was just “bad with money,” like some people are bad at math or can’t carry a tune. But the truth is more unsettling than personal inadequacy.

My brain was running ancient software in a modern world. Software that prioritized immediate rewards because, for most of human history, immediate rewards meant survival. If you found honey, you ate it now — winter was coming and there might not be honey tomorrow.

The problem? That same wiring makes us terrible at building capital.

Your Stone Age Brain In A Digital World

Think about the last time you had money burning a hole in your pocket. Maybe it was a work bonus or a surprise check from an old insurance claim. What happened next?

If you’re like most people, you felt an almost physical urge to spend it. Not on anything specific — just to convert that abstract number in your account into something tangible you could see, touch, or experience.

This isn’t a character flaw. It’s behavioral finance in action.

Your brain releases dopamine when you anticipate a reward. The bigger the potential reward, the bigger the hit. But here’s where it gets interesting: your brain gives you a much larger dopamine reward for things you can enjoy today versus things that might pay off in 10 or 20 years.

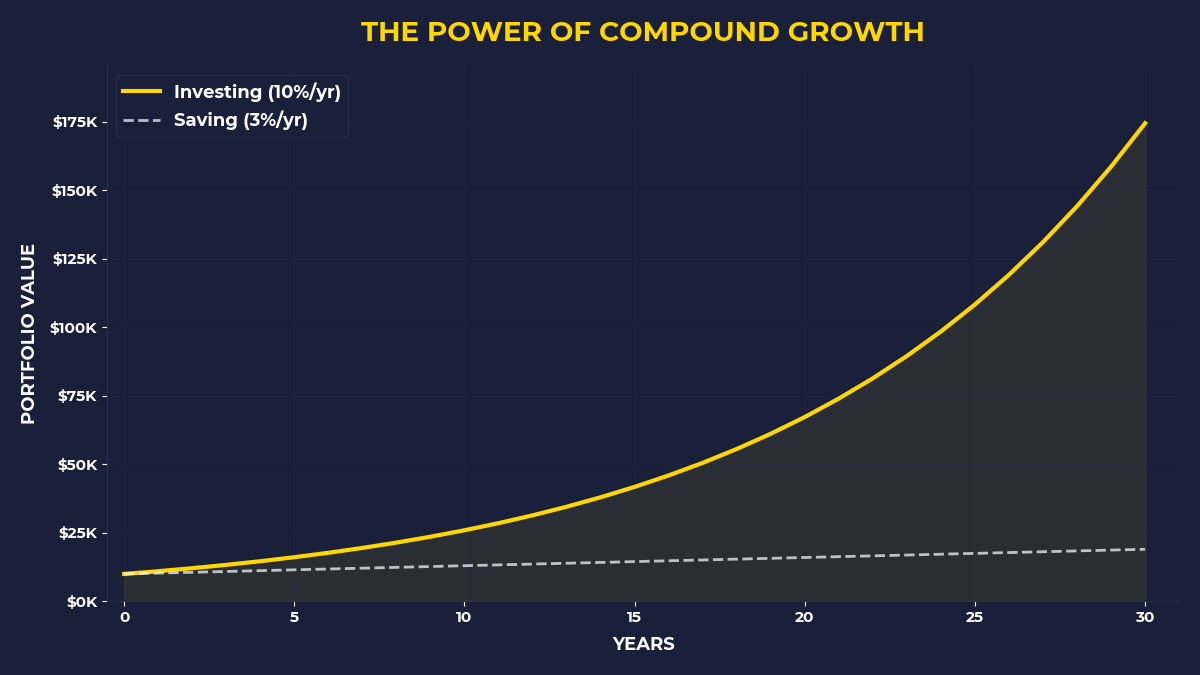

A $1,200 vacation to Barcelona? Massive dopamine hit. The idea of that same $1,200 compound into $4,800 over the next 15 years? Your brain barely registers it as a reward at all.

Economists call this “present bias.” I call it the reason most people never build real wealth.

The Capital Owners Know This About You

Walk into any casino and you’ll see behavioral finance weaponized for profit.

The lights, the sounds, the free drinks — they’re all designed to keep your ancient brain engaged while your rational mind takes a nap. The house doesn’t win because people are stupid. It wins because it understands exactly how human psychology works and profits from it.

But casinos aren’t the only ones using your behavioral biases against you.

Every “Buy Now, Pay Later” button on a website is exploiting your present bias. Every credit card company offering you a higher limit is betting on your brain’s inability to properly weigh future costs against immediate gratification. Every subscription service with an “easy cancel anytime” policy knows that 67% of people will never actually cancel — not because they love the service, but because their brain treats the monthly charge as invisible.

Capital owners study behavioral finance not to overcome these biases, but to profit from them. They know you’ll choose the immediate reward. They know you’ll underestimate future costs. They know you’ll procrastinate on building wealth while staying incredibly disciplined about paying their monthly bills.

The result? Your behavioral biases systematically transfer money from your pocket to theirs.

The Moment I Realized I Was Fighting My Own Brain

I was 26, sitting in my apartment, staring at my credit card statement.

$4,200 in debt, most of it from purchases I could barely remember. A $180 dinner “to celebrate” a small work victory. $320 worth of books I’d never read. A $450 jacket that made me feel successful for exactly one day.

Each purchase had felt reasonable in the moment. Each one triggered that dopamine hit that made my brain think I was making progress toward some version of success.

But sitting there with the statement in my hands, I realized I wasn’t fighting external circumstances or bad luck. I was fighting my own neural wiring.

That’s when I started thinking about behavioral finance as warfare. Not against the market or against other investors — against my own psychological programming.

Why Your Brain Hates Building Capital

Building real wealth requires behaviors that feel unnatural to your stone-age brain:

You have to delay gratification — sometimes for decades. You have to invest in things you can’t see, touch, or immediately enjoy. You have to trust that boring index funds will outperform flashy individual stocks, even though boring doesn’t trigger any dopamine release.

Worse, you have to do this consistently, month after month, while your brain screams at you to spend that money on something more immediately satisfying.

Think about that for a moment. Your brain literally evolved to make decisions that prevent wealth building. The same psychological mechanisms that kept your ancestors alive are now keeping you broke.

The $50 Experiment That Changed Everything

Here’s what I started doing after that credit card wake-up call:

Every time I got paid, before I paid any bills or bought any groceries, I moved $50 into a brokerage account and immediately bought index funds. Not because $50 was a lot of money, but because I needed to retrain my brain’s reward system.

The first few times felt terrible. My brain was used to getting its dopamine hit from spending money, not from investing it. But something interesting happened around month three.

I started getting a small dopamine hit from seeing my investment account balance grow. Not as big as the hit from buying something new, but enough to start rewiring my neural pathways.

By month six, I looked forward to investment day more than I looked forward to most purchases. My brain had learned a new pattern: money going into assets felt good. Money going to consumption felt increasingly wasteful.

This isn’t willpower. It’s behavioral conditioning.

The Compound Interest of Good Habits

Most people think compound interest only applies to money. But habits compound too.

Every time you choose to invest before you consume, you’re strengthening the neural pathway that associates wealth-building with reward. Every time you choose consumption first, you’re reinforcing the pattern that keeps you financially stuck.

The difference compounds exponentially.

Person A spends their tax refund on a vacation and gets a one-week dopamine hit. Person B invests their tax refund and trains their brain to see assets as rewards. Over 10 years, Person A has great vacation memories. Person B has capital that generates passive income.

This is why I say your brain is programmed to keep you poor forever. Left to its default settings, it will choose immediate consumption over delayed wealth-building every single time.

Are You Someone Who’s Ready To Reprogram?

This post isn’t for everyone. If you’re someone who believes wealth is mostly about luck or that rich people just had better starting advantages, this won’t help you. Your behavioral biases will remain intact, and capital owners will keep profiting from them.

But if you’re someone who’s tired of watching your money disappear into forgettable purchases while your friends who earn less somehow build more wealth — then you might be ready to fight your own brain’s programming.

If you’re someone who’s noticed that your best financial intentions consistently get hijacked by impulses you can’t quite explain — you’re looking at behavioral finance in action.

The One Thing To Remember

Your brain evolved to keep you alive in a world of scarcity, but you’re living in a world of abundance. The same psychological mechanisms that helped your ancestors survive are now systematically preventing you from building wealth. Every impulse purchase, every delayed investment decision, every time you choose immediate gratification over future security — that’s not a character flaw, that’s stone-age software running on a modern economic operating system. The only way to win is to acknowledge this programming exists and build systems that work with your psychology, not against it.

• Move money to investments before your brain has time to think about spending it

• Set up automatic transfers that happen without conscious decision-making

• Start small enough that your brain doesn’t perceive it as a threat to immediate needs

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.