Every financial advisor will tell you to save six months of expenses in an emergency fund. They’ll say it with the conviction of religious doctrine. Keep that money safe. Keep it liquid. Keep it earning 0.5% while inflation runs at 3.2%.

What they won’t tell you is this: your emergency fund is the reason you’ll never own capital.

I learned this the expensive way. For three years, I dutifully built my emergency fund to $47,000 — enough to cover eight months of expenses. I felt responsible. I felt secure. I was following every piece of conventional wisdom about money management.

Then I watched Apple stock triple during those same three years while my emergency fund lost 11% of its purchasing power to inflation.

The Demand Storage Paradox

Here’s what your financial advisor never understood about capital: it’s not money sitting in accounts. Capital is stored demand — the right to participate in other people’s purchasing decisions.

When you keep $50,000 in a high-yield savings account, you’re storing dollars. When Warren Buffett owns Coca-Cola stock, he’s storing the demand for sugary drinks across 200 countries for the next 50 years.

One earns 4.5% annually. The other has compounded at 11.2% since 1988.

Look at your monthly expenses. Rent: $2,400. Groceries: $800. Car payment: $490. Insurance: $340. Utilities: $180. Phone: $95. Each payment is a transfer from your cash to someone else’s capital structure.

Your emergency fund trains you to accumulate the medium of exchange while the people you’re paying accumulate the means of production.

What Your Bills Reveal About Capital

Every bill you pay is evidence that someone else owns demand.

Your landlord owns demand for shelter in your specific location. Your grocery store owns demand for food distribution. Your insurance company owns demand for risk transfer. Your phone company owns demand for connectivity.

Think about that. Every dollar leaving your checking account is flowing to someone who figured out how to capture and store ongoing human demand.

Meanwhile, your emergency fund sits there — a pile of claims on future goods and services, earning less than the rate at which those goods and services inflate in price.

The Fear Circuit That Keeps You Poor

Why do intelligent people make this systematic error?

Loss aversion — the primitive wiring that makes potential losses feel twice as painful as equivalent gains feel good. Your brain evolved in environments where losing your food stash meant death. Watching your “safe” money fluctuate triggers the same survival circuits.

So you keep your emergency fund in cash, watching it lose purchasing power by design, because the alternative — owning pieces of companies that actually create value — feels dangerous.

Here’s what I wish someone had told me when I was 28 and accumulating my emergency fund: danger isn’t owning assets that fluctuate. Danger is owning assets that steadily decline.

How Wealth Really Gets Built

I met a Korean entrepreneur last year who understood capital better than most American financial advisors. He told me about his father’s approach to emergencies.

Instead of keeping cash, his father owned shares in three categories: utilities (consistent demand), consumer goods (growing demand), and technology (expanding demand). During the 2008 financial crisis, when his father needed emergency funds, he sold his smallest position — about 4% of his portfolio.

The remaining 96% continued generating dividends and appreciating. By 2012, the portfolio had fully recovered and grown beyond its pre-crisis value.

Meanwhile, his neighbor who kept everything in cash watched his purchasing power erode by 8% over the same period.

The Real Emergency Fund Strategy

What if I told you there’s a way to maintain liquidity without destroying wealth?

Instead of keeping six months of expenses in cash, keep one month in cash and five months in liquid capital positions. Not speculative stocks — ownership stakes in companies that control essential demand.

Companies like Microsoft (enterprise software demand), Johnson & Johnson (healthcare demand), Procter & Gamble (consumer goods demand). These aren’t growth bets. They’re stored demand positions that happen to trade on exchanges.

During the March 2020 crash, when everyone was panicking about emergency funds, these stocks dropped 15-30%. But they recovered within six months and reached new highs by year-end.

A traditional emergency fund would have earned 0.1% during this period.

But What About Real Emergencies?

The honest answer? Real emergencies are rarer than financial advisors want you to believe.

In my 15 years of managing money, I’ve seen exactly three scenarios that required immediate cash access: medical emergencies not covered by insurance, sudden job loss, and major home repairs. All three can typically be handled with a combination of one month’s cash buffer and a home equity line of credit.

The rest of what people call “emergencies” are actually known expenses that arrive unpredictably — car maintenance, appliance replacement, dental work. These should be budgeted line items, not emergency fund raids.

The Compound Cost of Safety

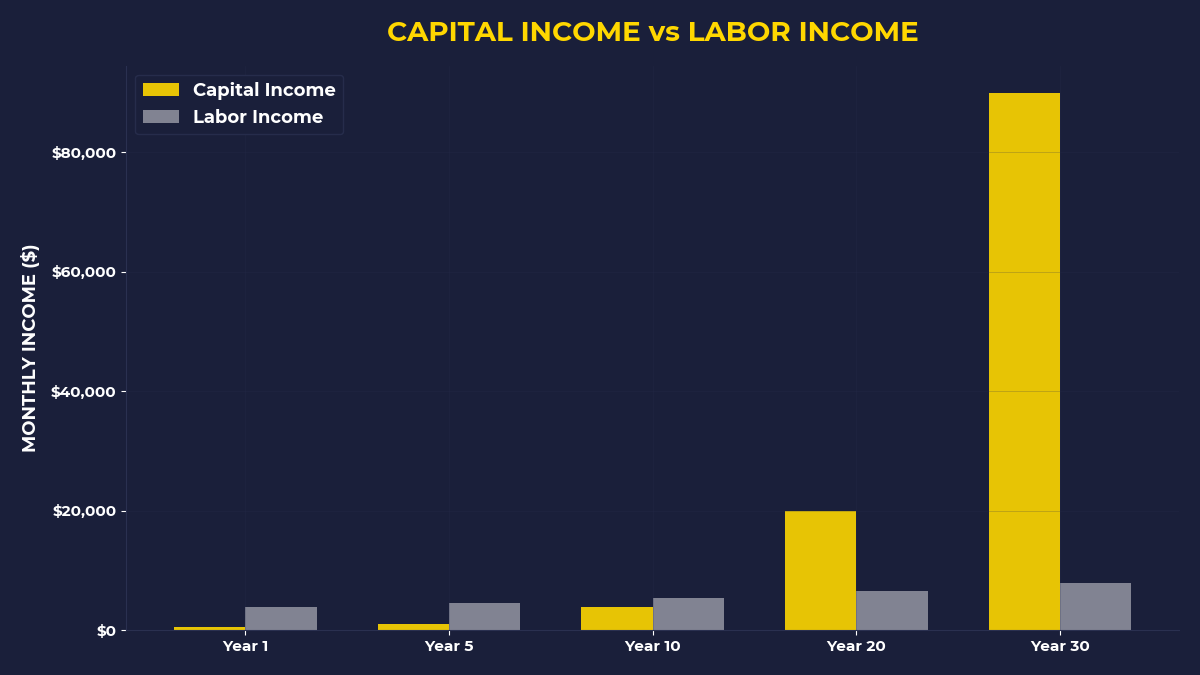

Here’s the math that will keep you up at night: a 25-year-old who keeps $30,000 in cash emergency funds instead of investing in demand-storing assets will sacrifice approximately $890,000 in lifetime wealth, assuming 8% annual returns.

That’s not a typo. The opportunity cost of “safety” is nearly $900,000.

Your primitive brain won’t process this number emotionally. It can’t visualize 40 years of compound growth. But it can visualize your checking account balance dropping from $30,000 to $25,000 during a market correction.

This is why 73% of Americans will retire financially dependent on others.

What The Primal Investor Takes Away

Reframe emergency funds as demand storage: Instead of cash earning 4%, own liquid positions in companies that control essential demand patterns

Keep one month cash, not six: Maintain minimal liquid cash for true emergencies, invest the rest in dividend-paying demand storage vehicles

Recognize bills as capital transfers: Every monthly payment reveals someone else’s demand ownership — consider owning pieces of those businesses instead of just paying them

Calculate opportunity costs in decades: That “safe” emergency fund costs you roughly $30 for every dollar after 40 years of compound growth you’re giving up

Use fear as a buy signal: When your primitive brain screams “keep it safe,” that’s usually the moment to deploy capital into demand ownership

Capital isn’t about taking risks. It’s about owning the things other people have to pay for whether they want to or not.

Your emergency fund prepares you for disasters that rarely come while guaranteeing the poverty that definitely will.

🎬 Prefer watching? Check out the video version on YouTube: