Have you ever noticed that every financial expert tells you the same thing? Build an emergency fund first. Three to six months of expenses, sitting safely in a savings account, earning basically nothing.

It sounds responsible. It feels secure. And it might be the biggest mistake you’re making with your money.

The Story Everyone Believes (But Shouldn’t)

Picture this: Sarah, a marketing manager, dutifully saves $500 every month. After two years, she’s built her perfect emergency fund — $15,000 earning 0.5% interest in her savings account. She feels proud, responsible, financially secure.

Meanwhile, her rent goes to her landlord’s retirement fund. Her car payment builds the dealership owner’s equity. Her monthly subscriptions fund tech billionaires’ next acquisitions. Her grocery bills enrich food company shareholders.

Every month, Sarah sends thousands of dollars to people who own things. Then she puts her leftover $500 into an account that loses purchasing power to inflation.

Who’s really building wealth here?

The emergency fund advice isn’t wrong because it’s bad for you. It’s wrong because it’s perfect for everyone else. While you pile up cash “for safety,” you’re funding other people’s asset purchases with your monthly bills.

What Robert Kiyosaki Learned Living in a Garage

Here’s a story that changed how I think about financial security forever.

Robert Kiyosaki, before he wrote “Rich Dad Poor Dad,” ran a business selling products at rock concerts. When the business failed due to accounting issues, he and his wife lost everything. They ended up living in a friend’s garage, surrounded by bills they couldn’t pay.

Most people would have taken any job to pay those bills immediately. But Kiyosaki did something that seemed crazy at the time.

Whenever money came in — from odd jobs, from whatever work he could find — he paid himself first. He bought small investments, stocks, anything that could potentially create future cash flow. Only then did he figure out how to pay the bills.

When pressed about unpaid bills, instead of using his investment money, he took on extra work. He mowed lawns at night. He did weekend labor jobs. Whatever it took to cover the bills — after he’d already invested in his future.

The result? Within a few years, his investments were generating enough cash flow that bills became irrelevant. He’d built real financial security — the kind that comes from owning things that pay you, not from hoarding cash that pays others.

Why Emergency Funds Create Emergency Thinking

Traditional financial advice trains you to think like an employee. Save money for when your job disappears. Build a cushion for when the paycheck stops.

But what if the real emergency isn’t losing your job? What if it’s spending your entire life dependent on jobs?

Emergency funds create emergency thinking. They prepare you for financial disasters instead of financial freedom. They’re designed for people who plan to work for money their entire lives.

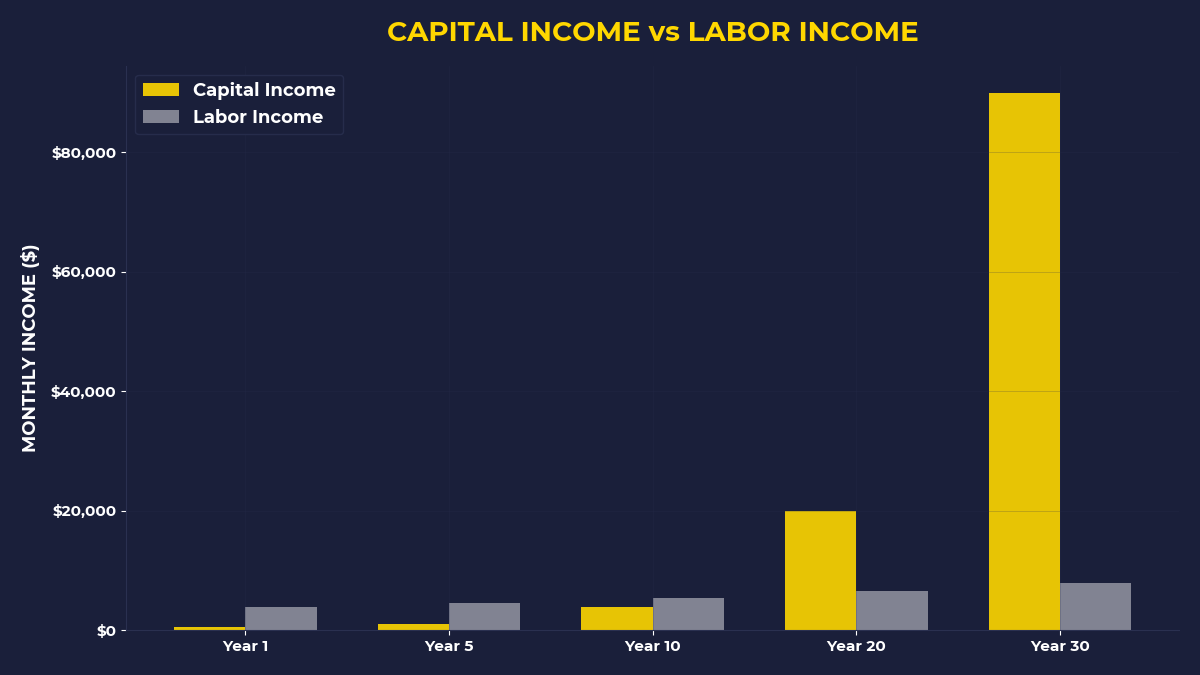

Capital owners don’t build emergency funds. They build emergency-proof income. They own things that generate cash flow regardless of economic conditions. When their pizza restaurant struggles, their apartment building still collects rent. When their consulting business slows down, their stock dividends still arrive.

This isn’t about taking stupid risks with money you need for food. It’s about recognizing that true security comes from ownership, not from cash hoarding.

The Golf Ball Principle of Real Security

Warren Buffett started building wealth as a kid by finding lost golf balls and selling them for $6 per dozen. But here’s what most people miss about this story.

Young Warren didn’t save up his golf ball money in a “golf ball emergency fund.” He reinvested every dollar into more ways to generate money. Better equipment for finding balls. Hiring friends to help collect them. Eventually, buying assets that made money while he slept.

This is compound security. Instead of building a pile of cash that shrinks with inflation, you build a system of assets that grows and throws off more cash over time.

An emergency fund is linear thinking. Put in $100, still have $100 (minus inflation). Asset building is exponential thinking. Put in $100, potentially own something that pays you $10 every year forever.

Which creates more security over time?

What Paying Yourself First Actually Looks Like

This doesn’t mean being reckless with money. It means changing the order of your financial priorities.

When your paycheck arrives, before you pay rent, before you buy groceries, before you cover bills — you invest a percentage in assets that can create future income. Even if it’s just $50 into an index fund.

Then you figure out how to cover everything else. Take on a side project. Sell something you don’t need. Work extra hours. The pressure forces creativity and hustle.

Most people do this backwards. They pay everyone else first, then invest whatever’s left (usually nothing). They’re funding other people’s dreams before their own.

Paying yourself first reverses this. You prioritize your financial freedom over your landlord’s, your bank’s, your insurance company’s. You become the first person who benefits from your labor, not the last.

Why This Feels Impossible (But Isn’t)

Your brain will rebel against this idea. It will show you all the ways this could go wrong. What if you can’t pay rent? What if your car breaks down? What if, what if, what if.

This fear is programming. You’ve been taught to see financial security as having enough cash to pay other people for a few months. But real security is having assets that pay you for decades.

The people who own your apartment building, who finance your car loan, who control your monthly subscriptions — they didn’t get there by building emergency funds. They got there by buying assets that create cash flow.

While you’re saving defensively, they’re building offensively.

The One Thing To Remember

Your emergency fund isn’t protecting you — it’s protecting the current system where you work for money instead of making money work for you. Real financial security comes from owning pieces of businesses, real estate, or assets that generate cash flow regardless of whether you show up to work. Emergency thinking creates a lifetime of emergencies. Ownership thinking creates a lifetime of options.

- This month, invest something before you pay any bills — even if it’s just $25 into an index fund

- Track where your monthly money goes and ask: “Am I funding someone else’s ownership or building my own?”

- Instead of asking “How can I save more?” ask “What can I buy that might pay me back?”

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.