Walk into any bookstore. Browse the success section. Count how many titles promise to teach you what to do versus what to buy. The ratio reveals everything about why 97% of people spend their lives building other people’s wealth instead of their own.

The primitive brain defaults to action. When financial pressure mounts, the primal response is motion—work harder, learn more skills, optimize productivity, network better. This instinct served our ancestors well when survival meant outrunning predators or gathering more berries. But in a capital-based economy, this same instinct becomes a wealth-destroying trap. The action bias makes us workers, not owners.

Warren Buffett understood this distinction at age six. While other children were asking “What should I do to earn money?”, young Warren was asking “What should I buy that people want?” This question shift—from doing to buying—unlocked the compound returns that transformed him from a golf ball picker into the world’s most successful investor.

The Golf Ball Principle: How Buying Beats Doing

In the 1940s, six-year-old Warren Buffett collected lost golf balls from local courses and sold them twelve for six dollars. Most people focus on the wrong part of this story—the hard work of diving into ponds and crawling through bushes. But the wealth-creating element wasn’t the labor. It was Buffett’s next move: using those earnings to buy assets that generated cash flow without his direct involvement.

He bought a Rolls-Royce to rent out. He purchased farmland. Each asset purchase created what we call compound returns from ownership—money that made money while he slept, studied, or pursued other opportunities. The golf balls were temporary labor income. The assets were permanent wealth engines.

Consider the alternative timeline: What if Buffett had asked “How can I pick golf balls more efficiently?” Instead of buying income-producing assets, he might have invested in better diving equipment, hired a caddie cart, or expanded to more golf courses. His income would have grown linearly with his effort. More work, more money. Stop working, stop earning. This is the trap that captures 97% of people their entire working lives.

The Leverage Effect of Ownership

Here’s where the story gets instructive. Imagine if young Buffett had hired ten friends—swimmers to retrieve balls from water hazards, cleaners to polish them, sellers to handle transactions. He pays each worker two dollars per dozen and keeps two dollars as the owner. Suddenly, Buffett earns twenty dollars per dozen without touching a single golf ball. Scale this to 100 dozens sold daily, and the owner makes $2,000 while the workers collectively make $2,000. Same total value created, but the ownership structure captures the upside.

This demonstrates why the wealthy think in terms of systems, not tasks. The question “What should I buy?” leads to leverage. The question “What should I do?” leads to self-employment.

The Scale Principle: From One to Seventy

The most illuminating wealth-building story involves Harry Larson, featured in a 1930s book called “The 1000 Ways to Make $1000” that influenced Buffett’s thinking. While buying medicine at a drugstore, Larson noticed customers using a coin-operated scale. Curious, he observed seven people weigh themselves in a short period. When he asked the store owner about the arrangement, he learned the scale was rented, generating about $20 monthly for a $175 investment.

Larson withdrew $175 from his bank account and rented his first scale. It generated $98 monthly. But here’s the wealth-creating insight: “I eventually bought seventy machines, and sixty-seven of them were paid for with coins from the first machine.”

This illustrates the compound returns from ownership principle that most people never grasp. Larson didn’t scale his personal effort—he scaled his capital acquisition strategy. Each successful asset purchase funded the next purchase. The cash flow from ownership, not the labor of operation, became the wealth multiplier.

Why This Thinking Remains Rare

The human brain rebels against this logic for primitive reasons. Loss aversion makes us prefer the certainty of labor income over the risk of asset ownership. We can control our effort; we cannot control market outcomes. The primal investor recognizes this bias and buys assets anyway, knowing that ownership of cash-flowing systems beats personal productivity over time.

Most people ask “How can I work harder to earn more?” The capital-minded ask “What can I buy that works for me?” This isn’t semantic wordplay—it’s the structural difference between building wealth and building someone else’s wealth.

Modern Asset Acquisition: Beyond Coin-Operated Scales

You don’t need to start a vintage scale rental business to apply the buying principle. The question “What should I buy?” works at every income level with different answers.

For the beginning investor, the answer might be index fund shares—buying fractional ownership in hundreds of companies whose employees work on your behalf. For someone with business experience, it might mean buying an existing profitable operation rather than starting from scratch. For the digital-native professional, it could mean buying domain names, creating digital products, or acquiring cash-flowing online businesses.

The Paycheck Allocation Test

Here’s how to identify whether you’re thinking like an owner or a worker: When your paycheck arrives, what gets paid first? Most people pay bills first—rent, utilities, groceries, insurance. These are all invoices from capital owners. The landlord owns the building. The utility company owns the infrastructure. The insurance company owns the risk pool.

The primal investor reverses this sequence. Pay yourself first by buying assets, then figure out how to cover the bills. This might mean taking weekend work, cutting expenses, or finding additional income sources. The key insight: Make asset acquisition the priority, not the afterthought.

This approach forces creative problem-solving that compounds over time. Instead of accepting bills as fixed costs, you start questioning every expense and finding ways to redirect money toward ownership.

The Laundromat Test: Systems Thinking vs. Task Thinking

Suppose you decide to enter the laundromat business. The “What should I do?” approach focuses on personal execution—finding a location, learning the business, operating the machines, handling customer service. You become a self-employed laundromat operator, trading time for money at a higher hourly rate.

The “What should I buy?” approach starts differently. You research existing profitable laundromats for sale. You analyze cash-flow statements, customer traffic patterns, equipment depreciation schedules. You consider locations with established demand. Most importantly, you plan for employee management from day one, designing systems that run without your constant presence.

The buying mindset immediately considers scaling—if one location generates positive cash flow, those profits fund the acquisition of location two. Each additional laundromat increases your ownership stake in cash-flowing assets. Eventually, you own a portfolio of automated businesses rather than a job requiring your daily presence.

The Creative Labor Advantage

This shift from repetitive labor to creative ownership unlocks what psychologists call intrinsic motivation. Humans are naturally creative beings. Building systems, solving problems, and designing improvements energizes us in ways that repetitive tasks cannot.

Compare the experience of working in someone else’s laundromat—refilling soap dispensers, handling complaints, cleaning machines—to owning multiple locations where your role involves strategic decisions, expansion planning, and system optimization. Same industry, entirely different psychological experience.

Breaking the Action Bias: From Motion to Ownership

The self-help industry exploits our action bias by selling us more things to do. Read this book, attend that seminar, develop these skills, optimize those habits. All valuable activities that improve human capital—your ability to earn wages. But human capital has a ceiling. Physical and mental energy are finite resources.

Financial capital has no ceiling. Properly structured assets compound indefinitely without your direct involvement. A dividend-paying stock portfolio can grow for decades while you sleep. A well-managed rental property generates cash flow for 30+ years. A profitable business system can operate and expand under competent management.

The Side Project Advantage

For employed professionals, the fastest path to ownership thinking might be side projects designed for capital acquisition strategy. Instead of freelancing for hourly fees, build something you can sell. Instead of consulting for immediate cash, create systems that generate recurring revenue. Instead of trading time for money, trade money for assets.

The test: Can this activity eventually run without your constant involvement? If yes, you’re building capital. If no, you’re building a second job.

What The Primal Investor Takes Away

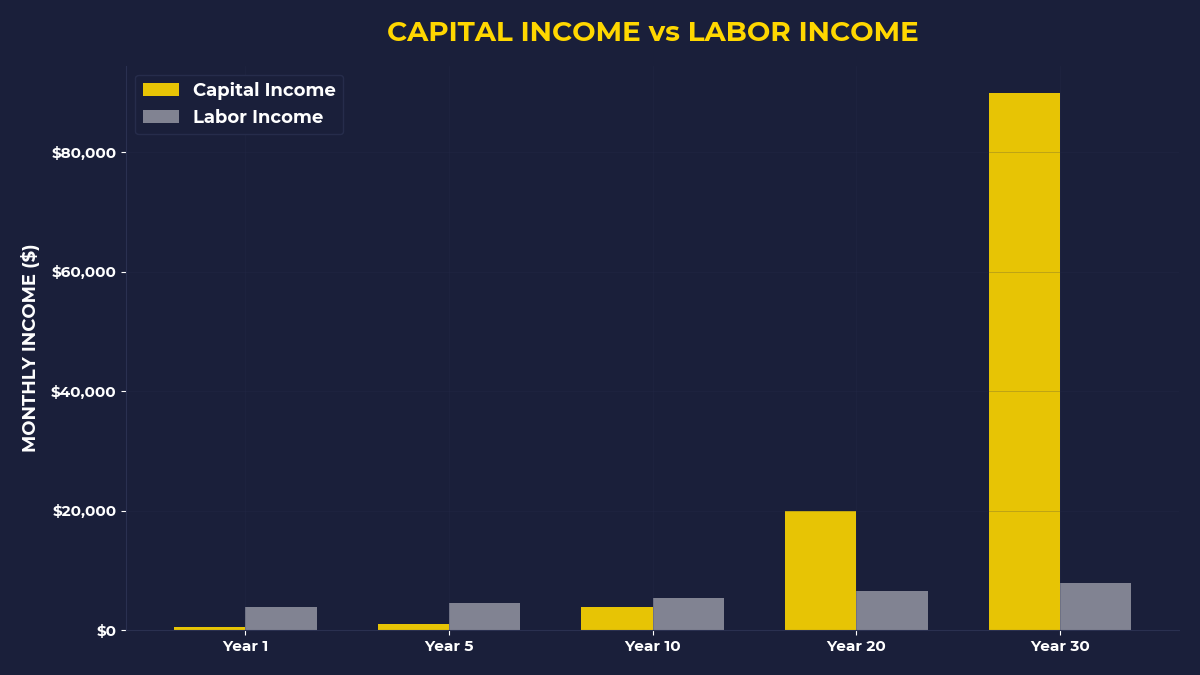

Question quality determines wealth outcomes: “What should I buy?” leads to ownership and leverage; “What should I do?” leads to self-employment and linear income growth.

Compound returns require ownership stakes: Labor income grows arithmetically with effort; capital income grows geometrically through reinvestment and scaling.

Asset acquisition before bill payment: Pay yourself first by buying cash-flowing assets, then solve for expenses—this reversal forces creative wealth-building solutions.

Systems thinking beats task thinking: Focus on buying businesses, not building jobs; acquiring structures that work without your constant presence.

The action bias destroys wealth: Primitive instincts push us toward more doing when we need more buying; motion feels productive but ownership creates freedom.

The wealthy understand that capital works harder than humans ever can. The question isn’t how to optimize your labor—it’s what to buy that will work on your behalf. This single shift in questioning transforms workers into owners, linear income into compound returns, and finite time into scalable wealth.

🎬 Prefer watching? Check out the video version on YouTube: