The Question That Separates Capital Owners From Everyone Else

I once spent three hours reading productivity books on a Sunday afternoon, looking for ways to optimize my morning routine and streamline my workflow. I wanted to know what successful people do differently. That same week, I watched my rent check disappear from my account — $2,400 flowing to someone who owned the building I lived in.

The irony hit me like a freight train.

While I was asking “What should I do to get ahead?” my landlord was collecting checks from 47 other tenants. He wasn’t working harder than me. He wasn’t following a better morning routine. He had simply asked a different question twenty years earlier: “What should I buy?”

Most people spend their entire lives asking the wrong question about money. They read self-help books, attend seminars, and optimize their habits. Meanwhile, 3% of the population quietly accumulates the assets that generate cash flow from everyone else’s productivity.

Why Your Bookshelf Is Full of the Wrong Advice

Walk into any bookstore and scan the business section. You’ll find hundreds of titles telling you what to do: wake up at 5 AM, network strategically, develop discipline, think positively, work smarter not harder.

I used to devour these books. I implemented morning routines, tracked habits, and attended networking events. I was optimizing my input — my effort, my time, my energy — but I was still trading hours for dollars.

Here’s what those books don’t tell you: Warren Buffett wasn’t successful because he had better habits than other investors. At age 11, he was picking up lost golf balls around golf courses and selling them for 6 cents each. But the genius wasn’t in the work ethic — it was in what he did with the money.

He used those earnings to buy more assets. First, pinball machines that he placed in barbershops. Then stocks. Then entire companies. The pattern wasn’t about working harder — it was about converting labor into ownership, then letting ownership work for him.

The Compound Interest Story Nobody Talks About

In the 1930s, a man named Harry Lawson was buying medicine at his local pharmacy when someone asked him how much he weighed. He noticed a coin-operated scale nearby, dropped in a penny, and weighed himself. Over the next few minutes, he watched seven more people use the same scale.

Curious, Harry asked the pharmacist about the machine. The owner explained he rented it and kept 75% of the revenue — about $20 per month from that single location.

Most people would have filed this away as an interesting fact. Harry asked himself a different question: “What should I buy?”

He withdrew $175 from his savings and purchased three scales, generating $98 monthly. But here’s the part that should rewire your brain: “I eventually bought seventy machines in all, and sixty-seven of them were paid for with coins from the first three.”

Harry understood something that escapes 97% of people: capital compounds when you consistently ask “What should I buy?” instead of “What should I do?”

Why Your Monthly Bills Are Invoices From Capital Owners

Look at your bank statement from last month. Every recurring charge — rent, utilities, subscriptions, car payments — represents someone else’s answer to “What should I buy?”

Your landlord bought real estate. Your electric company bought power plants. Netflix bought content libraries and streaming infrastructure. Your car loan company bought the right to collect interest on your transportation need.

They’re not working harder than you. They’re collecting recurring payments from thousands of people who are working hard.

This is why Robert Kiyosaki’s advice from the 1990s still stings: even when he was living in a friend’s garage after his business failed, he paid himself first. Not his creditors — himself. He bought small real estate investments before paying his bills, then worked extra jobs to cover what remained.

It sounds backwards until you realize what he was doing: prioritizing capital accumulation over expense management. Converting labor into ownership before ownership converted his labor into freedom.

The Leverage Question That Changes Everything

What if Warren Buffett hadn’t picked up those golf balls himself? What if he’d hired neighborhood kids to collect balls from dangerous water hazards and paid them $2 per dozen while selling them for $6?

With ten kids working for him, he’d earn $4 per dozen on 100 golf balls daily. That’s $400 in daily profit while the kids earn $200 each. Everyone wins — but Warren wins without trading his time.

This is leverage: asking “What should I buy?” extends naturally into “What systems should I own?”

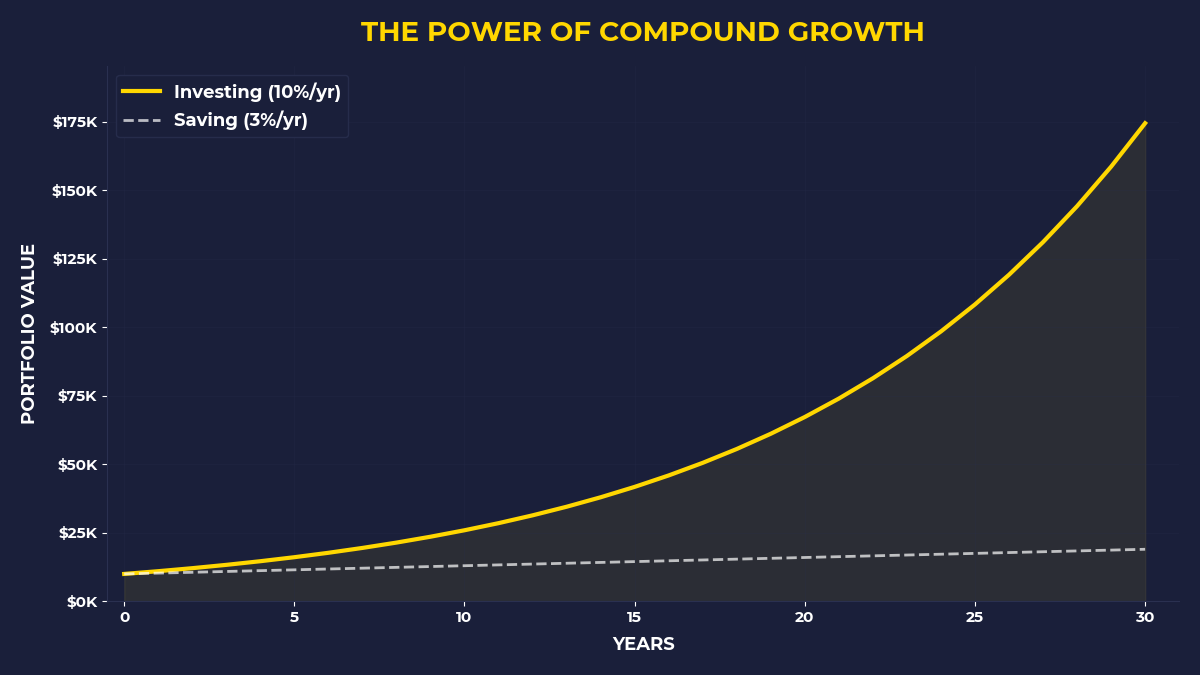

You don’t need to start a golf ball empire. If you’re earning $75,000 annually and consistently invest 15% into assets that historically return 10% per year, you’re buying pieces of systems that generate cash flow. The S&P 500 returned 11.2% annually from 2010 to 2020 — not because investors worked harder, but because they owned pieces of companies where other people worked.

Why Most People Never Ask the Capital Question

The question “What should I do?” feels empowering. It puts you in control. It appeals to our primal need to feel that effort equals results. We’re wired to believe that working harder leads to better outcomes — a useful instinct for hunter-gatherers, but a wealth-destroying bias in a capitalist system.

The question “What should I buy?” feels passive, even lazy. It requires you to admit that your individual effort has limits. It forces you to think structurally about cash flow, demand, and systems rather than tactically about productivity and optimization.

But here’s the uncomfortable truth: the economy rewards ownership, not effort. The Bureau of Labor Statistics shows that median household income has grown 22% since 2000, while the S&P 500 has grown 288% over the same period. Workers add value linearly. Owners multiply it exponentially.

What Should You Buy Instead of What Should You Do?

If you’re earning a salary and wondering how to start thinking like a capital owner, the path is simpler than you think — and harder than you want.

Simple because the options are obvious: index funds, dividend-paying stocks, real estate investment trusts, or small business ownership. Any asset that generates cash flow from other people’s demand.

Harder because it requires rewiring a lifetime of “work harder” programming. It means asking “What should I buy?” every time you get a windfall, a bonus, or even a small amount of discretionary income.

I know a software engineer who earns $140,000 annually but lives like he makes $90,000. The difference goes into Vanguard’s Total Stock Market Index. He’s not trying to pick winners or time markets. He’s buying pieces of systems that generate cash flow from millions of customers he’ll never meet.

After eight years, his investments generate about $1,200 monthly in dividends. Not enough to quit his job, but enough to start asking bigger versions of the capital question: “What should I buy next?”

The Primal Pattern That Keeps You Poor

Every January, millions of people set goals around habits and productivity. They want to wake up earlier, exercise more, network better, learn new skills. They’re optimizing their input.

Capital owners optimize their ownership.

When you ask “What should I do?” you’re thinking like an employee — even if you own a business. When you ask “What should I buy?” you’re thinking like an investor.

The difference compounds over decades. The “what should I do?” person gradually becomes more skilled, more productive, more valuable. The “what should I buy?” person gradually becomes more free.

What The Primal Investor Takes Away

• Change your default question: When you have extra money, ask “What should I buy?” before asking “What should I do with this?”

• Buy recurring demand: Look for assets that generate cash flow from other people’s ongoing needs — not one-time transactions.

• Compound your purchases: Use cash flow from existing assets to buy more assets, following Harry Lawson’s scale strategy at whatever scale you can afford.

• Think systems, not skills: Instead of asking “How can I earn more?” ask “What can I own that earns while I sleep?”

• Pay yourself first: Before paying bills, buy assets — even small ones — then figure out how to cover the difference through additional work.

• Leverage other people’s productivity: Whether through index funds or business ownership, buy pieces of systems where other people create value you can capture.

The question “What should I buy?” separates those who accumulate capital from those who rent their lives from capital owners. Most people will never ask it seriously. That’s exactly why it works.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.