Marcus — 29, software engineer in Denver — called me last Tuesday at 11:47 PM. He’d just finished calculating his net worth for the third time that month.

“I have $47,000 in savings,” he said. “More than most people my age. So why do I feel like I’m falling behind?”

His voice carried that specific frustration I recognize immediately. The confusion of someone who followed all the rules and somehow ended up losing the game anyway. Marcus had done everything the financial advisors told him to do. Six months of expenses. Emergency fund fully loaded. High-yield savings account earning a whopping 4.5% annually.

He was proud of that discipline. I would have been too.

But here’s what Marcus didn’t realize: his savings account wasn’t protecting him from poverty. It was guaranteeing it.

I Was the King of Emergency Funds Once

Look, I get the appeal. I used to be obsessed with my cash position.

When I was 26, I had $23,000 sitting in a savings account earning 2.1% interest. I checked the balance multiple times per day. Not because it was growing — it barely moved. But because that number represented safety. Control. The ability to handle whatever life threw at me.

I felt financially responsible. Mature. While my friends were “gambling” in the stock market or “wasting money” on startup investments, I was building a fortress of cash.

What I didn’t understand then was that my fortress was actually a prison.

Every month, I’d deposit another $800 into that account. And every month, I’d watch my purchasing power quietly erode while rent went up 7%, groceries increased 6%, and everything else I needed to buy got more expensive. My $23,000 could buy less in December than it could in January.

But the number stayed the same, so I thought I was winning.

Your Cash Is Someone Else’s Capital

Here’s what hit me like a freight train three years later: while I was saving cash, other people were buying capital.

My landlord used my rent check — along with hundreds of others — to buy more rental properties. My monthly $1,847 wasn’t just paying for a place to live. It was funding his expansion into a portfolio that now generates $34,000 per month in cash flow.

The grocery store chain where I spent $400 monthly used that revenue to open 23 new locations. The streaming services I paid $67 monthly used my subscription fees to produce content that attracted more subscribers.

Every dollar I saved was a dollar I didn’t use to buy a piece of those cash-generating machines.

And here’s the twist that really stung: the bank where I kept my savings? They were lending my money to real estate investors at 6.8% while paying me 2.1%. My own cash was being used to help other people buy the assets I should have been buying.

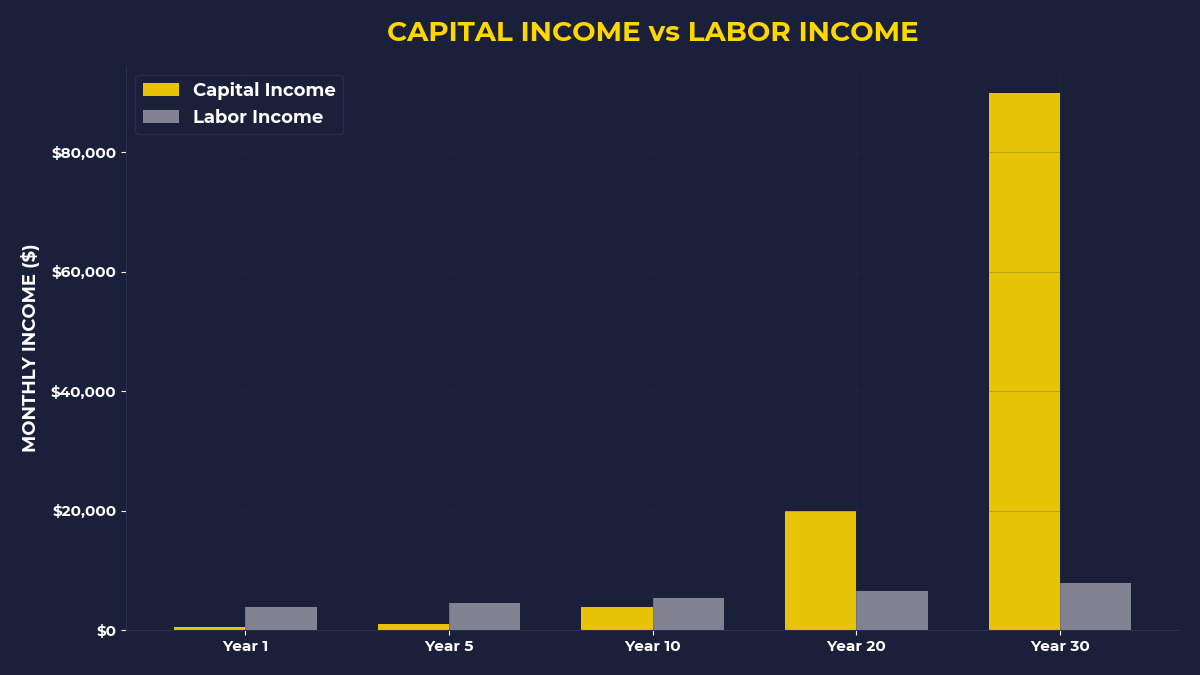

The Capital vs Cash Difference

What’s the fundamental difference between cash and capital?

Cash sits there. Capital works.

Marcus’s $47,000 in savings generates roughly $2,115 per year in a 4.5% account. That’s $176 per month. Not nothing, but hardly life-changing money.

Compare that to what happened when his college roommate Jake used a similar amount as a down payment on a duplex in 2019. Jake lives in one unit. The other unit rents for $1,650 monthly. After mortgage, taxes, and expenses, Jake nets about $400 per month — plus the property has appreciated $78,000 in five years.

Same starting amount. Completely different outcomes.

Jake bought demand. Marcus stored cash.

The Emergency Fund Myth

But what about emergencies?

This is where conventional wisdom gets dangerous. The financial industry has convinced millions of people that keeping 6-12 months of expenses in cash is “responsible.” But responsible for what? Responsible for ensuring you never build wealth?

I’m not saying emergencies don’t happen. They do. But here’s what I learned from watching hundreds of people navigate financial crises:

The people with substantial emergency funds still struggle when real emergencies hit. Six months of expenses doesn’t cover a serious illness, job loss in a recession, or family crisis. It just creates the illusion of preparation while keeping you poor.

Meanwhile, people with assets have options. They can borrow against their investments, sell appreciated positions, or generate income from their holdings.

Capital creates flexibility. Cash creates dependence.

How to Break the Cash Hoarding Habit

This shift requires rewiring your entire relationship with money.

Most people think: Earn money → Save money → Spend on necessities → Maybe invest what’s left.

Capital owners think: Earn money → Buy assets first → Use cash flow and income to cover expenses.

It sounds backwards until you realize that the first approach guarantees you’ll never have enough. There’s always another expense, another emergency to save for, another reason to keep cash on the sidelines.

When I finally made the switch at 29, I started with a simple rule: before paying any monthly bill, I moved $200 into a brokerage account to buy index funds. Even when it meant scrambling to cover rent.

Especially then.

That scrambling forced me to find additional income sources. Freelance projects. Side gigs. Creative solutions I never would have discovered if I had comfortable cash cushions.

The discomfort was the point. Comfort keeps you poor.

Why This Feels So Wrong

Your brain will resist this idea violently.

We’re wired to hoard resources during uncertain times. Cash feels safe because you can see it, touch it, count it. Investments feel risky because the numbers move around.

But this instinct developed when resources were scarce and storage was survival. In a modern economy built on credit and inflation, cash hoarding is a wealth-destroying behavior disguised as prudent planning.

The people getting rich understand this. They use debt to buy assets and inflation to erode their debts. They borrow against their portfolios instead of selling them. They think in terms of cash flow, not cash piles.

If You’re Someone Who Takes Pride in Your Savings Rate

This post isn’t for people who struggle to save money. If you can’t consistently save 10% of your income, work on that first.

This is for people like Marcus — disciplined savers who’ve built impressive cash positions but can’t figure out why they still feel broke. People who’ve mastered the mechanics of saving but never learned the art of capital formation.

If you have more than three months of expenses in savings, you’re not being financially responsible. You’re being financially naive.

The wealthy don’t keep large cash positions. They keep large asset positions with small cash reserves for liquidity.

The One Thing to Remember

Your savings account isn’t protecting your future — it’s preventing it. Every month you choose cash over capital, you’re choosing to stay exactly where you are. The number might grow, but your purchasing power and wealth-building capacity shrink. Capital owners understand that reasonable risk with appreciating assets beats “safety” with depreciating cash every single time.

Start this week:

• Calculate how much cash you have beyond one month of expenses

• Move 80% of that excess into low-cost index funds or dividend-paying stocks

• Before paying next month’s bills, invest $100-500 first (whatever amount makes you slightly uncomfortable)

🎬 Prefer watching? Check out the video version on YouTube: