The Morning Maria Finally Got It

Maria — 29, marketing coordinator in Phoenix — stood in line at her neighborhood Starbucks on a Tuesday morning in March. She’d just checked her savings account balance: $8,400. Not bad for someone making $47,000 a year. She felt responsible, even proud.

Then she watched the barista scan fifteen customers ahead of her, each paying $4.50 for their daily fix. In ten minutes, she watched $67.50 flow into some corporate account. Every single day. Seven days a week.

That’s when it hit her. Her $8,400 was just sitting there, earning 0.5% annually. Meanwhile, she was funding someone else’s wealth machine with her daily coffee habit.

The numbers were staggering once she started adding them up.

I Used to Think Saving Money Made Me Smart

Look, I get it. I was Maria five years ago, except I was 31 and living in Denver, working as a project manager. I had $12,000 in my savings account and thought I was winning at personal finance.

Every finance blog told me the same thing: build an emergency fund, save for retirement, live below your means. I followed every rule. I was the responsible one among my friends.

But here’s what nobody explained: while I was saving money, other people were buying my demand.

Every month, I sent $1,200 to my landlord, $280 to my car payment, $150 to my phone and internet providers, $400 to grocery stores, $80 to Netflix, Spotify, and other subscriptions. I was writing checks to capital owners all day long while my own money earned nothing in a savings account.

I was funding everyone else’s wealth while mine stayed flat.

Capital Isn’t Money — It’s Stored Demand

Here’s the thing most people never understand about capital: it’s not the money sitting in your bank account. Capital is stored demand.

When people need what you own, you have capital. When they don’t, you just have stuff.

Think about Maria’s coffee shop experience. That Starbucks location represents stored demand. Every morning, hundreds of people show up needing caffeine. The demand is predictable, recurring, and profitable. Whoever owns that demand stream — through real estate, franchise rights, or corporate stock — collects money while they sleep.

Meanwhile, Maria’s $8,400 savings account represents zero demand. Nobody needs her cash except the bank, which pays her almost nothing to borrow it.

The difference between capital and money is the difference between freedom and captivity.

Why Your Bills Are Really Invoices From Capital Owners

Let me show you something that changed how I see money forever.

Pull up your bank statement from last month. Look at your automatic payments and regular expenses. Every single one is a payment to someone who owns capital.

Your rent check? That’s paying someone who owns the capital asset called real estate. Your car payment? Someone owns the capital that produces cars. Your Netflix subscription? Capital owners who control entertainment demand.

Even your morning coffee is a payment to capital owners who control caffeine distribution.

You’re not just buying products and services. You’re transferring your cash flow to people who own the infrastructure of demand.

The average American sends money to capital owners dozens of times every day without realizing it.

What Happens When You Start Buying Demand Instead

I remember the exact moment I switched sides. It was October 2019, and I’d just gotten my quarterly bonus — $3,200 after taxes. Instead of adding it to my savings account, I bought shares of companies I was already paying every month.

I bought stock in my cell phone carrier. In the company that owned my apartment building. In the index fund that included my grocery store chains.

Wild, right? I went from being purely a customer to being a partial owner.

Within six months, those companies were paying me dividends with money that came partly from people like my old self. I was collecting tiny pieces of everyone else’s monthly bills.

That bonus kept working. My savings account never did.

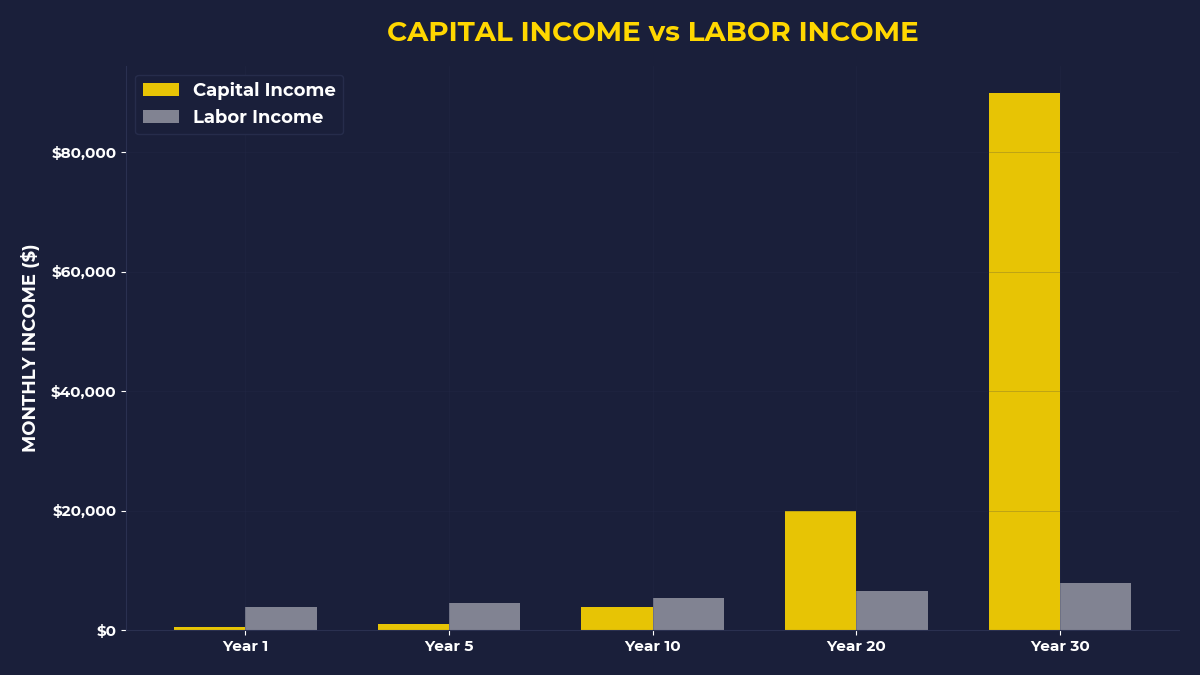

The Compound Power of Stored Demand

Here’s where it gets interesting. Capital compounds because demand compounds.

When you own stored demand, you collect cash flow. When you use that cash flow to buy more stored demand, you collect more cash flow. Warren Buffett calls this the “snowball effect,” but it’s really just buying demand with the money that demand generated.

A friend of mine — software engineer, $85,000 salary — started buying one share of Apple stock every month in 2018. Not because he loved the company, but because he noticed he was sending Apple money every month anyway through his iPhone payment, App Store purchases, and iCloud storage.

By 2023, his Apple shares were paying him quarterly dividends larger than his monthly iPhone bill. He’d reversed the cash flow.

That’s stored demand at work.

Are You Someone Who’s Ready to Switch Sides?

This isn’t for everyone. If you’re living paycheck to paycheck, focus on increasing your income first. If you have high-interest debt, pay that off before buying anything else.

But if you’re like Maria or my old self — sitting on a savings account while writing checks to capital owners every month — you’re ready to start thinking differently about money.

The goal isn’t to become rich overnight. The goal is to stop being purely a customer and start being partially an owner.

The One Thing to Remember

Capital is stored demand, not stored money. Every month you send cash to capital owners while your savings account collects dust, you’re choosing the wrong side of the wealth equation. The people getting rich aren’t working harder than you — they’re collecting pieces of demand that never stops flowing. Start buying what people need instead of just being someone who needs things.

Here’s what to do this week:

• Look at your three largest monthly bills and research if you can buy stock in those companies

• Move your next $200 from savings into a brokerage account before paying any non-essential bills

• Ask yourself: “What am I buying versus what should I be buying?” every time you spend money this week

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.

")