Marcus Chen — 29, software engineer at Google, $180,000 salary — called me last September in a panic. He’d been waiting for the “perfect entry point” into the market for eighteen months. Every weekend, he’d run Monte Carlo simulations on different investment scenarios. Every Monday, he’d find another reason to wait.

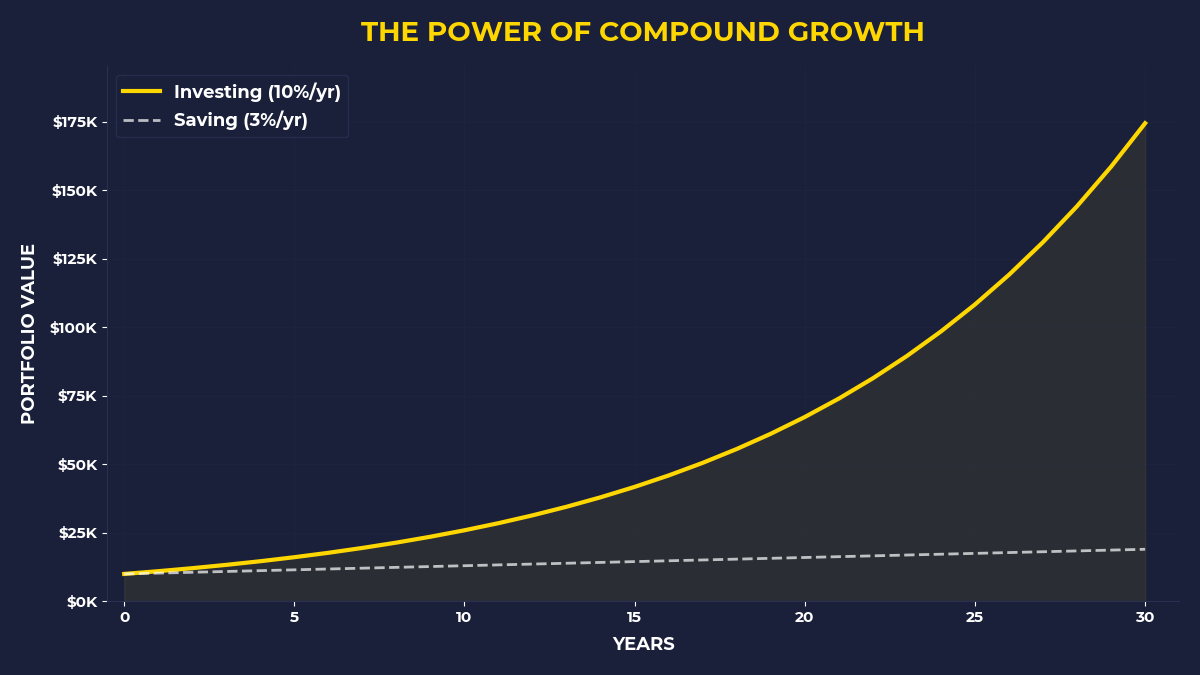

The S&P 500 had climbed 23% while Marcus optimized his spreadsheets.

“I know I’m overthinking this,” he said. “But what if I buy right before a crash? What if there’s a better opportunity next month? What if—”

I stopped him there. “Marcus, you make more money than 90% of Americans. You’ve been ‘researching’ investments longer than most people hold their actual investments. And you own exactly zero dollars of productive assets.”

The silence stretched for ten seconds.

“Smart people,” I told him, “are the worst investors on earth.”

Why Intelligence Is Your Enemy

I know because I was Marcus five years ago. MBA from Wharton, consultant at McKinsey, absolutely convinced that my analytical skills would translate into market success. I spent months building DCF models for individual stocks. I read every 10-K filing. I knew the price-to-book ratios of 47 companies off the top of my head.

My portfolio returned 4.2% annually while the market did 11.8%.

Here’s what nobody tells you about contrarian investing: it’s not about being smarter than the crowd. It’s about being dumber than your own brain. The moment you start thinking you can time markets, optimize entry points, or wait for perfect setups, you’ve already lost.

Smart people suffer from what I call “optimization paralysis.” We see too many variables. We imagine too many scenarios. We want to solve for X when X is deliberately unsolvable.

Meanwhile, my neighbor Janet — 43, works at Home Depot, never graduated college — has been putting $200 into an index fund every month for eight years. No research. No timing. No optimization.

Her returns crush mine.

The Stupidest Smart Money Move

Want to know the most contrarian thing you can do with money? Buy when you’re broke.

Not when you have extra money sitting around. Not when you’ve built the perfect emergency fund. Not when you’ve analyzed every possible scenario and determined the optimal allocation.

When you’re broke.

I learned this the hard way in March 2020. I was between consulting gigs, living off savings, genuinely worried about making rent in a few months. The market had crashed 30%. Every rational voice in my head screamed: “Preserve cash. Wait this out. Don’t be an idiot.”

But I remembered reading about Warren Buffett buying during the 2008 crisis. Not with his fun money. With borrowed money. When banks were calling in loans and everyone else was liquidating everything they owned.

So I took $1,200 from my emergency fund — money I genuinely needed — and bought shares of an S&P 500 ETF.

That $1,200 is worth $2,400 today.

The missed rent payment? I picked up freelance work and covered it three weeks later. But here’s the thing: if I had waited until I felt financially “safe,” that opportunity would have vanished. By the time I had comfortable excess cash again, the market had already recovered.

Why Your Brain Sabotages Your Wealth

Think about the last time you bought something expensive during a financial squeeze. Maybe you needed a new laptop when money was tight. Maybe your car broke down between paychecks. You probably found the money, right? You figured it out.

But suggest buying stocks during that same financial squeeze, and suddenly you become “responsible.” You decide to wait. You prioritize “stability.”

This is your brain protecting you from the wrong thing.

Your financial anxiety isn’t about the money you might lose investing. It’s about the money you’re definitely losing by not investing. Every month you wait, every dollar you keep in savings, every “perfect moment” you’re preparing for — that’s capital flowing away from you toward people who already own assets.

Marcus realized this in October. He finally bought his first index fund shares — not because he’d found the perfect entry point, but because he’d gotten tired of being poor on a six-figure salary.

“I felt nauseous for three days after buying,” he told me. “Then I felt nauseous that I’d waited so long.”

The Rich Do Everything Backwards

Here’s what separated Marcus from actual wealth builders: wealthy people buy assets before they buy anything else. Not after they pay all their bills. Not after they’ve saved up enough to feel comfortable. Before.

They buy assets when they can’t afford them, then figure out how to afford everything else.

This sounds insane until you understand what assets actually do. They don’t sit there looking pretty in your portfolio. They generate claims on other people’s productive output. Every share of Apple stock entitles you to a piece of every iPhone sold, every App Store transaction, every subscription payment — forever.

Your monthly bills, meanwhile, represent claims that other asset owners have on your productive output. Rent payments to your landlord. Loan payments to banks. Subscription fees to platform owners. Utility payments to infrastructure companies.

Notice the pattern? Bills flow money away from you to asset owners. Assets flow money from everyone else toward you.

The only way to switch sides of this equation is to prioritize asset purchases over bill payments. Not because bills don’t matter, but because the longer you wait to buy assets, the longer you stay trapped on the wrong side of the equation.

If You’re Someone Who Thinks Too Much

Maybe you’re like Marcus — analytically minded, financially educated, paralyzed by your own intelligence. Maybe you’ve been researching investments longer than most people have owned them. Maybe you’re waiting for clarity that will never come.

Here’s what I wish someone had told me: contrarian investing isn’t about predicting what the market will do. It’s about predicting what you’ll do when the market moves against you.

And what you’ll do, if you’re honest, is exactly what every smart person does. You’ll panic when prices drop. You’ll get greedy when prices rise. You’ll buy high and sell low while convincing yourself you’re being rational.

Unless you build a system that makes those decisions for you.

The One Thing To Remember

Smart money isn’t smarter than dumb money — it just has better systems. While you’re optimizing entry points, wealthy people are accumulating assets automatically. While you’re waiting for perfect conditions, they’re buying during the worst possible conditions. While you’re preserving capital, they’re deploying capital that doesn’t feel safe to deploy.

The most contrarian thing you can do is stop trying to be smart about money and start being systematic about it.

Set up an automatic transfer of $200 (or whatever you can barely afford) from checking to a broad market index fund every month, regardless of market conditions or your financial situation

Buy additional shares whenever you feel financially squeezed — that anxiety is a buy signal, not a preservation signal

Never check your account balance when you’re making investment decisions; only check it when you’re celebrating gains or rebalancing annually

🎬 Prefer watching? Check out the video version on YouTube: