Sarah — 29, marketing manager in Denver — was eating ramen noodles for dinner when her phone buzzed. Her investment app notification cheerfully announced that her portfolio had dropped 12% in three days. She’d bought $3,000 worth of tech stocks the week before because they’d been “on sale.” Now she was watching that money disappear while she literally couldn’t afford groceries.

The cruel irony? Her savings account had $47,000 sitting in it earning 0.01% interest.

She’d kept that money “safe” for two years while missing the biggest bull run in decades. But the moment the market dipped, she panic-bought with borrowed money from her credit card. Her brain had played the same trick that keeps millions of people broke: be conservative when you should be aggressive, and aggressive when you should be conservative.

Wild, right?

I Know Because I Was There Too

I used to think I was smarter than my own brain. In 2018, I had $23,000 in cash and was “waiting for the right moment” to invest. I researched companies for months, read every Warren Buffett book, convinced myself I was being disciplined.

Then Tesla dropped 30% in December, and I finally pulled the trigger. Bought $15,000 worth at what felt like a bargain. Watched it drop another 20% in January. Sold everything at a 23% loss because I couldn’t sleep.

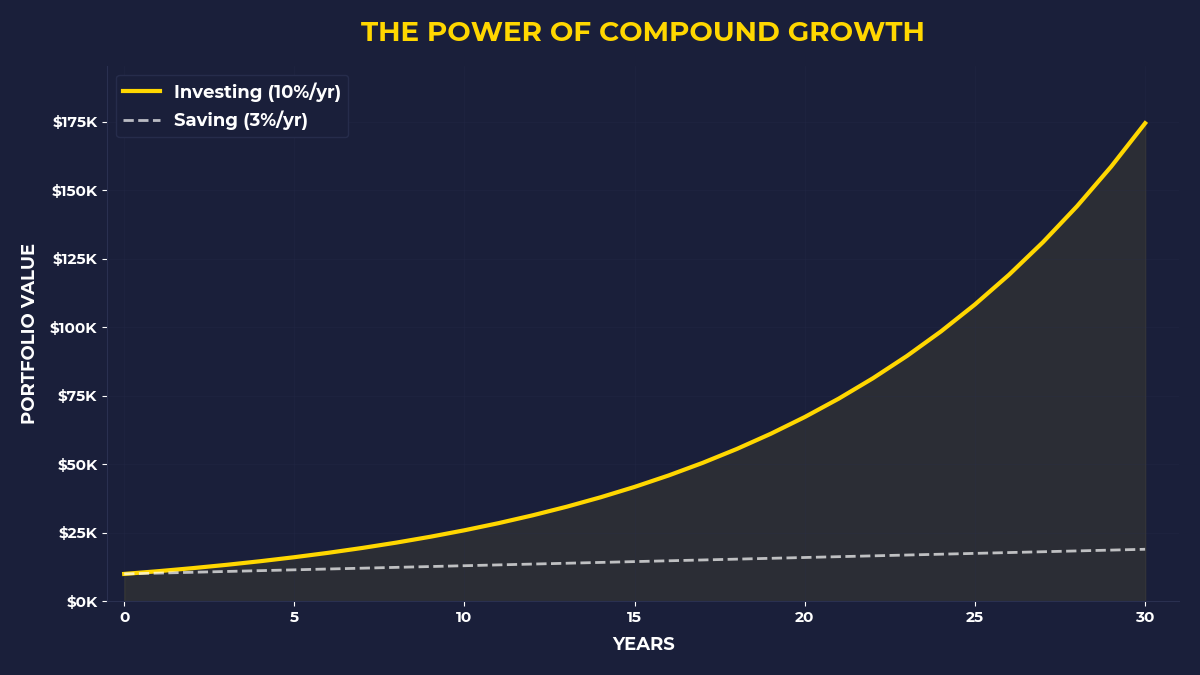

Six months later, Tesla had doubled. My “disciplined” approach had cost me $45,000 in missed gains. Meanwhile, my friend Jake — who knows nothing about finance — had been buying $500 worth of index funds every month like clockwork for three years. His brain never got involved in the decision.

That’s when I realized something terrifying: my own intelligence was working against me.

Your Stone Age Brain In a Digital Age Economy

Here’s the thing about behavioral finance that nobody talks about honestly. Your brain isn’t broken. It’s working exactly as designed — for a world that disappeared 10,000 years ago.

Think about that. Every financial decision you make gets filtered through neural pathways built for hunting mammoth and avoiding saber-tooth tigers. Your ancestors who hoarded resources during good times and panicked at the first sign of trouble were the ones who survived. The optimistic ones who took big risks during uncertain times? They became tiger food.

But in modern capital markets, those survival instincts become wealth-destroying machines.

You see a market crash and your amygdala screams “DANGER!” The same brain circuit that would’ve saved you from a charging bear now makes you sell Amazon at $1,800 and watch it climb back to $3,200. Your pattern-seeking cortex finds faces in clouds and “sure things” in stock charts. The same mental shortcuts that helped your ancestors recognize which berries were poisonous now convince you that past performance predicts future results.

Most people don’t realize they’re fighting 200,000 years of evolution every time they open a brokerage account.

The Scarcity Switch You Can’t Turn Off

Want to see your prehistoric programming in action? Watch what happens when money gets tight.

Last month, my neighbor Tom — 42, electrician, father of two — got his hours cut at work. His first move? He stopped his $300 monthly investment in his kids’ 529 plans. “Can’t afford luxuries right now,” he told me over the fence. The next day I watched him spend $400 getting his truck detailed.

Tom isn’t stupid. He’s human. When resources feel scarce, your brain switches into immediate survival mode. Truck maintenance feels urgent and real. College savings 15 years from now feels abstract and optional. Your amygdala can’t tell the difference between “I have $200 less this month” and “Winter is coming and we might starve.”

So you stop feeding your capital and start protecting your cash. Exactly backwards.

This is why 73% of Americans have less than $1,000 in savings but somehow find $1,200 every year for streaming subscriptions. Your brain categorizes Netflix as a necessity and index funds as a luxury. Because in the moment of decision, entertainment feels more urgent than ownership.

The Pattern That Keeps You Sending Your Money Away

Let me show you the behavioral trap that catches almost everyone.

Every month, you pay rent first. Then utilities, then car payment, then insurance, then groceries, then subscriptions. If there’s anything left over, maybe you invest it. This feels responsible. This feels like being an adult.

But here’s what’s actually happening: you’re training your brain that everyone else’s claim on your money comes before your own.

Your landlord gets paid before you pay yourself. Netflix gets paid before you buy capital. The credit card company gets paid before you build wealth. You’ve programmed your own brain to prioritize other people’s cash flow over your own ownership.

And your brain loves this pattern because it’s predictable. Paying bills feels like completing tasks. Buying assets feels like gambling with your survival.

The One Mental Shift That Changes Everything

What if I told you the solution isn’t about finding more money or better investments? What if it’s about rewiring one simple sequence?

Pay yourself first. Not last. First.

I know what you’re thinking. “I can’t afford to invest before paying bills.” That’s exactly the scarcity programming talking. But here’s what happens when you flip the sequence: when rent is due and you’ve already moved $500 into assets, your brain suddenly gets creative about finding that $500 elsewhere.

You skip the $12 lunch and pack one. You don’t buy the $80 sweater you didn’t really need. You find a way to make it work because now you HAVE to. The artificial scarcity forces efficiency.

But when you invest your “leftover” money, there’s never any leftover. Your spending expands to fill whatever’s available. That’s Parkinson’s Law applied to your bank account.

Breaking the Cycle Before It Breaks You

Sarah from our opening story? She figured this out six months ago.

Instead of trying to time markets or pick individual stocks, she automated the decision away from her brain entirely. Every payday, $800 moves automatically into index funds before she can think about it. Her checking account gets whatever’s left for bills and life.

The first month was brutal. She had to eat out less, skip a concert, actually use that gym membership she’d been paying for. But something interesting happened in month two: she stopped missing the money. Her brain adapted. Her spending compressed. She found efficiencies she didn’t know existed.

Now she’s 12 months in with $11,400 in assets. For the first time in her adult life, she owns something that pays her back instead of sending all her money to other people’s capital.

Her brain still wants to panic-sell during market drops. But the automation removes the decision from her emotional circuits.

If You’re Tired of Your Own Brain Working Against You

This post is for people who are smart enough to know they should be building wealth but honest enough to admit their own psychology keeps sabotaging them. You’ve read the books, you understand compound interest, you know what you should be doing. But somehow you keep making the same behavioral mistakes.

You’re not weak. You’re not undisciplined. You’re fighting programming that’s older than agriculture.

The people who build real wealth don’t have better brains. They have better systems that work around their brains.

The One Thing To Remember

Your brain is wired to keep you alive in a world that no longer exists, but those same survival instincts will keep you broke in the world that does exist. The solution isn’t to fight your psychology — it’s to automate around it. When you remove emotional decision-making from wealth-building, your ancient programming stops working against your future self.

Here’s what to do this week:

Set up an automatic transfer from checking to investments that happens on payday, before you pay any bills

Start with an amount that makes you slightly uncomfortable — if $200 feels scary, that’s probably the right number

When bills feel tight because you paid yourself first, get creative about earning or saving that difference instead of stopping the automation

🎬 Prefer watching? Check out the video version on YouTube: