Sarah — 29, marketing coordinator in Denver — opened her brokerage app for the third time that Tuesday morning. Her Apple stock was down 12% from where she’d bought it six weeks earlier. Her stomach twisted the same way it did when her boss called her into meetings. She closed the app, opened it again, then finally hit sell. “I can’t lose any more,” she muttered, transferring the remaining $3,400 back to her checking account where it felt safe.

Three months later, Apple had recovered and hit new highs.

Sarah had just demonstrated the most expensive behavioral finance mistake in human history — and her brain had convinced her it was the smart thing to do.

I Used To Be Sarah’s Brain

I know exactly what Sarah was feeling because I was there too. Back in 2019, I bought Tesla at $240 per share. Not because I understood the company, but because everyone on Twitter was talking about it. When it dropped to $180, my brain went into full panic mode. The same brain that could analyze marketing campaigns all day suddenly turned into a frightened animal when it came to money.

Here’s the thing.

I sold at $165. Tesla went on to hit $900 the next year.

That $4,000 loss taught me something crucial: our brains aren’t wired to build wealth. They’re wired to survive. And in the modern economy, survival instincts keep us exactly where capital owners want us — sending them our money every single day.

Your Brain’s Ancient Operating System

Your brain runs on 50,000-year-old software trying to navigate a 50-year-old financial system. Think about that for a second. The same neural pathways that helped our ancestors survive on the savanna now make decisions about compound interest and stock volatility.

The mismatch is brutal.

When Sarah saw her Apple position dropping, her amygdala — the brain’s alarm system — flooded her body with cortisol. Her ancestors felt this exact same chemical cocktail when a predator appeared. The appropriate response back then? Run. The appropriate response to a temporary stock decline? Usually nothing.

But her brain doesn’t know the difference. It just knows: danger, loss, escape.

Meanwhile, the people getting rich off these psychological money traps understand this system perfectly. They’ve built entire business models around your brain’s predictable irrationality. Every behavioral finance mistake you make puts money directly into their pockets.

The Fear-Greed Wealth Transfer Machine

Here’s what actually happened to Sarah. When Apple dropped 12%, institutional investors — the people who already owned massive amounts of capital — started buying. They have systems, rules, and most importantly, enough wealth that a temporary decline doesn’t trigger their survival instincts.

Sarah, operating from paycheck-to-paycheck anxiety, sold her shares directly to them at a discount.

Wild, right?

The same psychological pattern plays out millions of times every day. Regular people buy high when everything feels safe (greed), then sell low when things get scary (fear). Capital owners do the opposite. They buy when others are scared and sell when others are greedy.

This isn’t about being smarter. It’s about having enough capital that your survival brain doesn’t hijack your decisions.

I learned this the expensive way. After my Tesla disaster, I started tracking my own investor behavior patterns. What I discovered horrified me: I was systematically buying assets when they were expensive and selling them when they were cheap. Not because I was stupid, but because my brain was designed to do exactly that.

The Instant Gratification Trap

Have you ever noticed how easy it is to spend money on things that make you feel good right now, but incredibly hard to buy assets that will pay you later?

That’s not an accident.

Your brain releases dopamine — the same chemical triggered by cocaine — when you make an immediate purchase. New shoes, fancy coffee, restaurant meals. The neurological reward is instant and powerful.

But buying index funds? Boring. No dopamine hit. No immediate gratification. Your brain treats it like eating vegetables — necessary, maybe, but not exciting.

This is why 78% of Americans live paycheck to paycheck while spending $1,200 per year on coffee and $3,500 per year on dining out. Their brains are optimized for immediate pleasure, not long-term wealth building psychology.

Meanwhile, capital owners have learned to flip this script. They’ve trained themselves to get excited about cash flow, compound returns, and asset appreciation. They’ve literally rewired their reward systems.

The Scarcity Programming

Most people I talk to about investing immediately mention risk. “What if I lose money?” “What if the market crashes?” “What if I need that cash for an emergency?”

But they never ask: “What if I keep doing what I’m doing and stay broke forever?”

This isn’t balanced thinking. This is scarcity programming. Your brain assumes the default state is poverty, so any financial risk feels existential. Capital owners assume the default state is wealth creation, so not investing feels risky.

I remember the first time I had $10,000 in savings. My brain kept generating scenarios where I might need that money immediately. Car repair. Medical bill. Job loss. The money felt safer sitting in a checking account earning 0.1% interest.

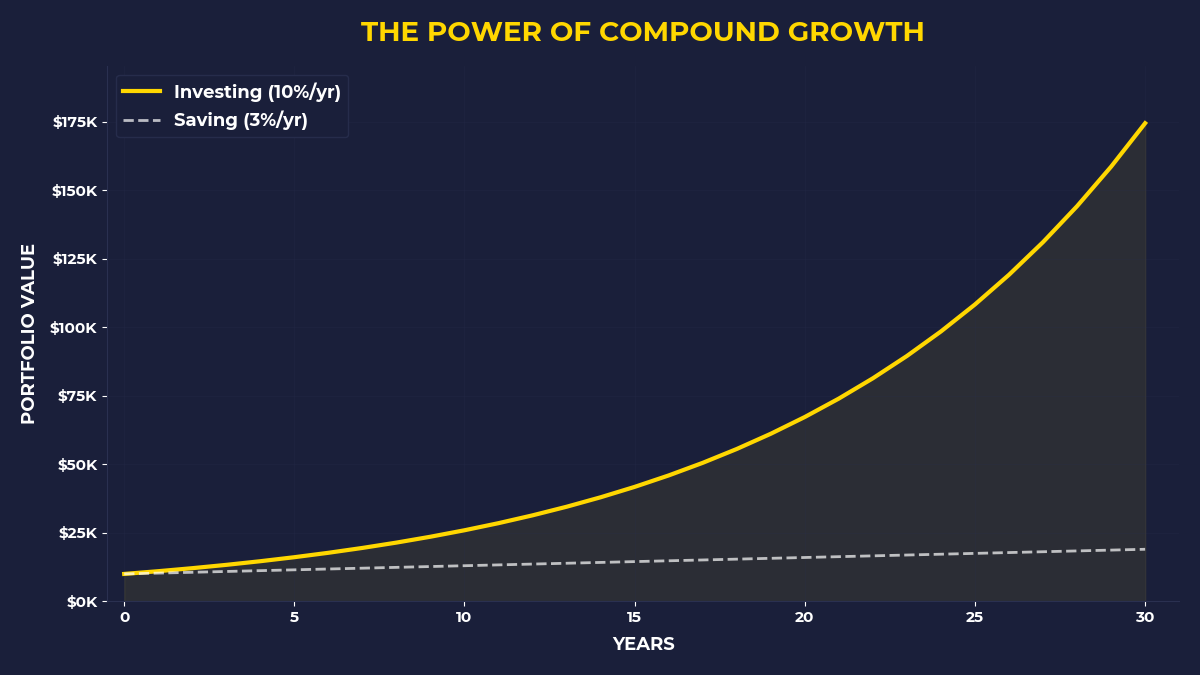

What my scarcity-programmed brain couldn’t calculate was the opportunity cost. That $10,000 in an S&P 500 index fund would have grown to $18,000 over the next five years. But my ancient survival software convinced me that guaranteed poverty was safer than potential wealth.

The Pattern Recognition Problem

Your brain is incredible at recognizing patterns. It can spot a face in a crowd, remember where you parked your car, and detect when someone is lying to you. But when it comes to financial decision making biases, this pattern recognition becomes a liability.

Here’s why.

Your brain looks for patterns in random market movements. It sees three green days in a row and thinks “trend!” It sees a stock drop and thinks “danger!” It creates narratives where none exist.

Professional investors know this. They’ve learned to ignore the patterns their brains want to see and focus on the underlying demand that creates capital. They buy businesses that solve human problems, not chart patterns that trigger their psychology.

But most people are still trying to time the market, predict crashes, and find the “perfect” moment to invest. Their pattern-seeking brains turn wealth building into gambling.

The Social Proof Money Trap

Look around your friend group. How many of them own significant assets? How many talk about cash flow, equity positions, or capital appreciation?

If you’re like most people, the answer is close to zero.

This creates a massive social proof problem. Your brain assumes that whatever most people around you are doing must be the safe, normal choice. If everyone is living paycheck to paycheck, spending money on experiences, and avoiding “risky” investments, your brain interprets this as the correct strategy.

But think about this: the bottom 50% of Americans own just 2% of total wealth. The social proof you’re following is actually proof of how to stay poor.

Capital owners surround themselves with other capital owners. Their social proof reinforces wealth-building behaviors instead of wealth-destroying ones.

Reprogramming Your Financial Operating System

The good news is that your brain is plastic. You can literally rewire your psychological money traps by changing the inputs and rewards.

Start here: every time you feel the urge to buy something that doesn’t produce cash flow, pause. Ask yourself: “Am I about to send money to a capital owner, or am I about to become one?”

That $150 dinner sends money to a restaurant owner. That $40,000 car sends money to an auto manufacturer’s shareholders. That $2,000 rent check sends money to a real estate investor.

What if you flipped just one of those decisions?

Instead of the expensive dinner, you buy $150 worth of index funds. Instead of financing the car, you buy used and invest the difference. Instead of just paying rent, you start saving for a down payment on your own place.

Your brain will resist this at first. It won’t feel rewarding. But here’s what I learned: you can train yourself to get excited about becoming a capital owner instead of just making capital owners richer.

The One Thing To Remember

Your brain’s wiring isn’t your fault, but it is your responsibility. Every day, your ancient survival instincts are making financial decisions that benefit people who already have capital. The fear that keeps you in cash is making bank owners wealthy. The greed that makes you buy high is making fund managers bonuses. The scarcity that prevents you from investing is guaranteeing you’ll stay scarce.

Capital owners succeed not because they’re smarter, but because they’ve learned to work with their psychology instead of against it.

Here’s what you can do today:

Set up automatic investing so your scared brain can’t interfere with your wealth-building decisions

Before any purchase over $100, ask yourself: “Does this create cash flow or consume it?”

Start getting excited about assets the way you currently get excited about consumption — track your net worth like you track your social media likes

🎬 Prefer watching? Check out the video version on YouTube: