The Cruel Math of Addition vs. Multiplication

You spend 8 hours creating $200 worth of value. Your boss keeps $150. You get $50.

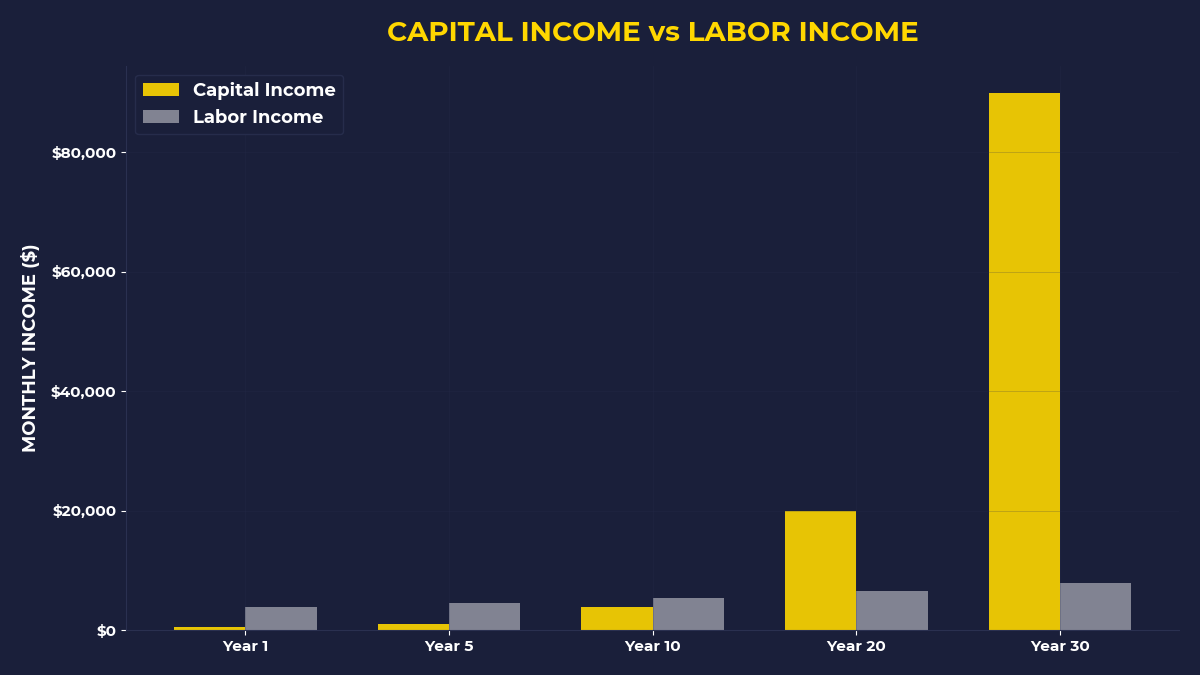

Your boss uses that $150 to buy assets that generate $30 per day while he sleeps. You use your $50 to pay bills to other asset owners. After 10 years, your boss owns $109,500 in cash-flowing assets. You own nothing except the right to show up tomorrow and create another $200 for him.

This is not exploitation. This is mathematics.

Workers add value linearly — one hour, one output, one paycheck. Owners multiply wealth exponentially — one asset purchase, infinite compounding, perpetual cashflow. The difference between addition and multiplication explains why 73% of Americans live paycheck to paycheck while the top 1% own 32% of all wealth.

Here’s what nobody teaches you: capital is not money sitting in your bank account. Capital is stored demand that generates cash flow without your labor.

When I Learned Capital Theory the Expensive Way

I used to think capital meant having money. Big mistake.

In 2019, I had $47,000 in savings. Felt rich. Felt secure. Then I got laid off from my consulting job and watched that cash disappear at $4,200 per month. Rent, groceries, car payment, insurance — every dollar went to someone else’s assets. My savings was not capital. It was just delayed consumption.

That’s when I discovered Warren Buffett’s golf ball story. As a kid, Buffett collected lost golf balls, cleaned them up, and sold them for 6 cents each. But here’s the part that changed how I think about money: he didn’t spend the profits on candy or toys. He used every dollar to buy more assets — pinball machines, farmland, car washes. Assets that generated cash flow without his direct labor.

The golf balls weren’t the business. The capital accumulation was the business.

Most people work harder to earn more. Buffett worked once to buy assets that worked for him forever. This is the demand storage model in action — converting temporary labor into permanent cash flow generators.

Why Capital Is Stored Demand (Not Stored Labor)

Think about every bill in your mailbox. Rent. Netflix. Car payment. Groceries. Phone service.

Each bill represents demand flowing to a capital owner. Your landlord owns the demand for shelter. Netflix owns the demand for entertainment. Tesla owns the demand for transportation. Whole Foods owns the demand for organic kale.

You create value through labor, but you don’t own the demand for that value. Your employer does. That’s why they can replace you with someone cheaper, faster, or more compliant. Labor is abundant. Demand ownership is scarce.

Consider Harry Larson’s weight scale story from the 1930s. He noticed people paying 1 cent to weigh themselves at the pharmacy. Instead of thinking “I should start a weight-checking service,” he thought “I should own the demand for weight checking.” He bought 3 scales for $175, placed them strategically, and collected $98 per month in passive income. Then he used those profits to buy 67 more scales.

Harry didn’t work harder. He owned more demand.

The Creative Labor vs. Repetitive Labor Trap

Why do famous singers earn millions while nurses save lives for $65,000? It’s not about social value. It’s about demand ownership versus demand servicing.

Taylor Swift owns the intellectual property to her songs. When someone streams “Anti-Hero,” she collects royalties while sleeping. The demand for her music is stored in copyrights, streaming platforms, and licensing deals. Her labor created the asset once. The asset generates income infinitely.

A nurse provides critical care but owns no intellectual property, no patient relationships, no medical equipment. She services existing demand but stores none of it. Her labor stops, her income stops.

This explains why creative labor builds wealth while repetitive labor just pays bills. Creative labor produces assets you can own. Repetitive labor produces value others own.

Loss aversion — our primal instinct to avoid losses more than we seek gains — tricks us into choosing “safe” repetitive jobs over “risky” asset creation. We fear losing steady paychecks more than we desire owning equity. This fear keeps us in the addition game instead of the multiplication game.

What Changes When You Ask “What Should I Buy?” Instead of “What Should I Do?”

Most career advice asks: What skills should you develop? What industry should you enter? What certifications should you get?

Capital theory asks: What demand should you own? What assets should you buy? What systems should you acquire?

When you ask “What should I do?”, you’re optimizing for labor efficiency. When you ask “What should I buy?”, you’re optimizing for capital accumulation.

I know a software engineer who makes $140,000 per year. After taxes, rent, and expenses, she saves maybe $18,000. She’s highly skilled, works hard, adds tremendous value. But she owns zero equity in the systems she builds. Every line of code she writes becomes her employer’s intellectual property.

Her colleague makes $90,000 but spends every weekend building rental properties. He owns 4 units generating $1,200 each in monthly cash flow. That’s $57,600 per year in passive income — more than half his day job salary. His capital works while he sleeps.

Same industry. Same city. Different question.

The Compound Capital Accumulation Model

Here’s how multiplication beats addition: Every dollar you earn should first buy you more capital before it pays anyone else’s bills.

Robert Kiyosaki learned this lesson when his business failed and he was living in a friend’s garage. Despite creditor pressure, he paid himself first — investing every available dollar in assets before paying bills. When money ran short, he took weekend jobs cutting grass and washing dishes to cover expenses.

This sounds backwards until you understand the psychology. When you pay bills first, there’s never money left for assets. When you buy assets first, you create pressure to find additional income sources. The discomfort forces you to think like an owner instead of an employee.

Between 1942 and 2020, the S&P 500 generated 11.2% annual returns with dividends reinvested. A worker investing $500 monthly in index funds for 30 years would accumulate $1.36 million. That’s the power of owning demand across 500 companies instead of working for just one.

Why Most People Never Escape the Addition Game

Your brain evolved for immediate survival, not long-term wealth building. When you see $500 in your checking account, ancient programming screams “spend this on immediate needs before it disappears.” The part of your brain that calculates compound returns over 30 years is newer, weaker, easily overridden by fear.

Social proof amplifies this trap. Everyone around you trades time for money, so trading time for money feels normal. Your friends rent apartments, lease cars, pay subscription fees. They’re optimizing for consumption, not capital accumulation. Following their behavior keeps you in the same financial position they’re in.

The most successful capital accumulators I know felt uncomfortable for years. They drove older cars while buying stocks. They lived in smaller apartments while building investment portfolios. They felt behind their peers’ lifestyle until their assets started generating serious cash flow.

If You’re Still Trading Time for Money After Age 35

Look. I get it. Payroll feels safe. Benefits feel secure. A steady job feels responsible.

But every month you don’t own appreciating assets is a month you fall further behind the multiplication curve. The 40-year-old with no equity lives paycheck to paycheck just like the 25-year-old with no equity. Age doesn’t build wealth. Asset ownership builds wealth.

If you’re reading this and thinking “I’ll start investing next year when I have more income,” you’re trapped in linear thinking. Capital accumulation starts with the first dollar, not the perfect dollar amount.

The question isn’t whether you can afford to buy assets. The question is whether you can afford to keep renting your time without owning anything that works on your behalf.

What The Primal Investor Takes Away

• Capital stores demand, not labor — Buy assets that collect payments from others’ ongoing needs, not assets that require your ongoing work.

• Ask “What should I buy?” before “What should I do?” — Optimize for ownership opportunities before optimizing for labor efficiency.

• Pay yourself first in assets, not savings — Direct your first dollars toward cash-flowing assets, then find additional income to cover bills.

• Creative labor builds assets; repetitive labor pays bills — Prioritize work that produces intellectual property, systems, or equity you can own.

• Compound returns require ownership, not just hard work — The S&P 500’s 11.2% annual returns only benefit those who own shares, not those who just work for member companies.

• Discomfort signals you’re building capital — If investing doesn’t feel slightly uncomfortable, you’re probably not investing enough to change your financial trajectory.

Workers add value to other people’s systems. Owners multiply wealth through their own systems. The math is brutal, but the choice is yours.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.

")