My cousin Rachel — 31, teacher, lives in Portland — called me on a Tuesday night last spring, and the first thing she said was: “I just did the math and I’ve earned over $400,000 in the last ten years. I have $11,000 in savings. Where did it all go?”

She wasn’t crying. She wasn’t angry. She was just genuinely confused. Like she’d done everything right — showed up, worked hard, paid her bills on time — and somehow ended up with almost nothing to show for a decade of adult life. That confusion, that quiet bewilderment, is the realest thing I know.

I Asked the Same Question for Years

When I was 27, I had a spreadsheet. I know, I know. But I was proud of it. Income on one side. Expenses on the other. I tracked every coffee, every streaming subscription, every parking ticket. And for about three years I was disciplined about it, in the way that only someone with no money and a lot of anxiety can be disciplined.

Here’s the thing. The spreadsheet told me exactly where my money went. Rent. Groceries. Utilities. Car insurance. Eating out on Fridays because I deserved it after the week I’d had. The numbers were perfectly clear. And yet I wasn’t getting anywhere. I was surviving with precision.

The spreadsheet was answering the wrong question entirely.

I was asking: How do I spend less? The actual question — the one nobody handed me — was: What should I be buying that pays me back?

Those are not the same question. Not even close.

Truth #1: Every Bill You Pay Is Someone Else’s Investment Return

Think about the last 30 days of your financial life. Your rent or mortgage. Your electricity. Your phone plan. Your Netflix and your Spotify and your gym membership. Your groceries, your gas, your car payment. The coffee you grabbed this morning without thinking about it.

Every single one of those payments went somewhere. Not into a void. Into the cash flow of a person or company that owns something you needed. Your landlord collects your rent because they own the building. Amazon collects your Prime subscription because they own the platform. The coffee chain collects $6.50 because they own the brand and the real estate and the supply chain.

You are not just a customer. You are a recurring revenue source for capital owners. Every single month, without fail, you send checks to people who own things.

That’s not a moral judgment. It’s just how the system works. And once you see it clearly — really see it — you can’t unsee it.

Rachel, my cousin with the $11,000, wasn’t irresponsible. She paid $1,850 a month in rent for seven years. That’s $155,400 that went directly to someone who owned her building. She paid car insurance for a car she financed. She had a gym membership she used maybe twice a week. Each one of those was a perfectly reasonable individual decision. Together, they meant she spent a decade on the paying side of the ledger, and someone else spent that same decade on the receiving side.

The divide isn’t income. It’s ownership.

Truth #2: Capital Isn’t Money — It’s Stored Demand

This one took me an embarrassingly long time to grasp. I used to think capital meant having a lot of money saved. Like capital was just a fancy word for a big bank account.

It isn’t.

Capital is what you own when people consistently need what you have. That’s it. When people need your apartment, you have capital. When people subscribe to your software month after month, you have capital. When people buy coffee from your 47 locations every morning because it’s habit and convenience and the logo feels right — that’s capital. The money is just the evidence that the demand exists.

I think about a story I came across once about a guy — let’s call him Harry — who was in a drugstore in the 1930s when someone asked him his weight. He looked around, found a coin-operated scale, dropped in a penny. Then he watched seven more people do the exact same thing in the next few minutes. He asked the store owner about it. Turned out the store was leasing the scale, keeping 25% of the take — about $20 a month.

Harry went home and withdrew $175 from his bank account. He leased three scales. Within weeks he was making $98 a month. Then he bought more. Eventually he owned 70 of them. And here’s the part that matters: 67 of those 70 scales were purchased using the money the first three generated.

He didn’t work harder. He didn’t earn a promotion. He identified a demand — people want to know what they weigh, right now, for a penny — and he put himself on the ownership side of that demand. Then he used the proceeds to own more of it.

That’s the whole game. Identify where demand flows. Buy a piece of it. Use what it generates to buy more pieces.

Wild, right? And yet it’s so obvious once you see it that you almost feel cheated for not being told sooner.

Truth #3: The Question You’ve Never Been Asked

Here’s what I find genuinely strange. I went through 16 years of formal education. I took a personal finance class in high school where we learned to write checks — actual paper checks, by hand — and balance a checkbook. In college I took an economics course that was mostly about supply and demand curves and things that happened in 1929.

Not once did anyone sit me down and ask: What are you going to buy that will pay you back?

Every piece of advice I got was about what to do. Study hard. Get good grades. Find a stable career. Work your way up. Save 10% of your paycheck. The whole framework assumed that my job was to optimize my labor — to be a better, more efficient, more credentialed worker — and that wealth would eventually follow.

It doesn’t follow. Not automatically. Not for most people.

The self-help section at any bookstore is full of books about doing. Wake up at 5am. Build these habits. Develop these skills. Network strategically. These books aren’t wrong, exactly. Being better at your job matters. But here’s what they leave out: a more productive worker is still a worker. The return on your labor is capped by your hours. The return on capital compounds on its own while you sleep.

I have a friend — Marcus, 38, software engineer in Seattle, makes around $160,000 a year — who spent his entire thirties getting better at his craft. He’s genuinely excellent at what he does. He got three raises in eight years. He also has no equity in anything. He owns no shares in the companies that use his code to generate hundreds of millions in revenue. He rents his apartment. He leases his car. Every month he sends money to capital owners while being paid a fixed rate for his time.

Marcus is incredibly smart. But he was answering the question everyone gave him — how do I do my job better? — instead of the question nobody gave him: what should I own?

What Actually Changes Things: Buying Before Paying

Let me be honest about something. When I first started actually thinking about this — not just reading about it, but sitting with it — I didn’t have a lot to invest. I was 29, I had maybe $400 in discretionary cash each month, and I had real bills that needed paying.

The shift that mattered wasn’t finding more money. It was changing the order of operations.

Before, I paid all my bills and bought all my necessities and then, if anything was left, I’d think about investing. Which meant I never invested, because there was never anything left. The bills expanded to fill whatever I had.

What I started doing — uncomfortably, with real anxiety — was moving $100 into a brokerage account on the day I got paid. Before rent. Before groceries. Before anything. Then I figured out how to cover everything else. Sometimes that meant one fewer dinner out. Sometimes it meant a stressful week near the end of the month. But the $100 went in first. Every time.

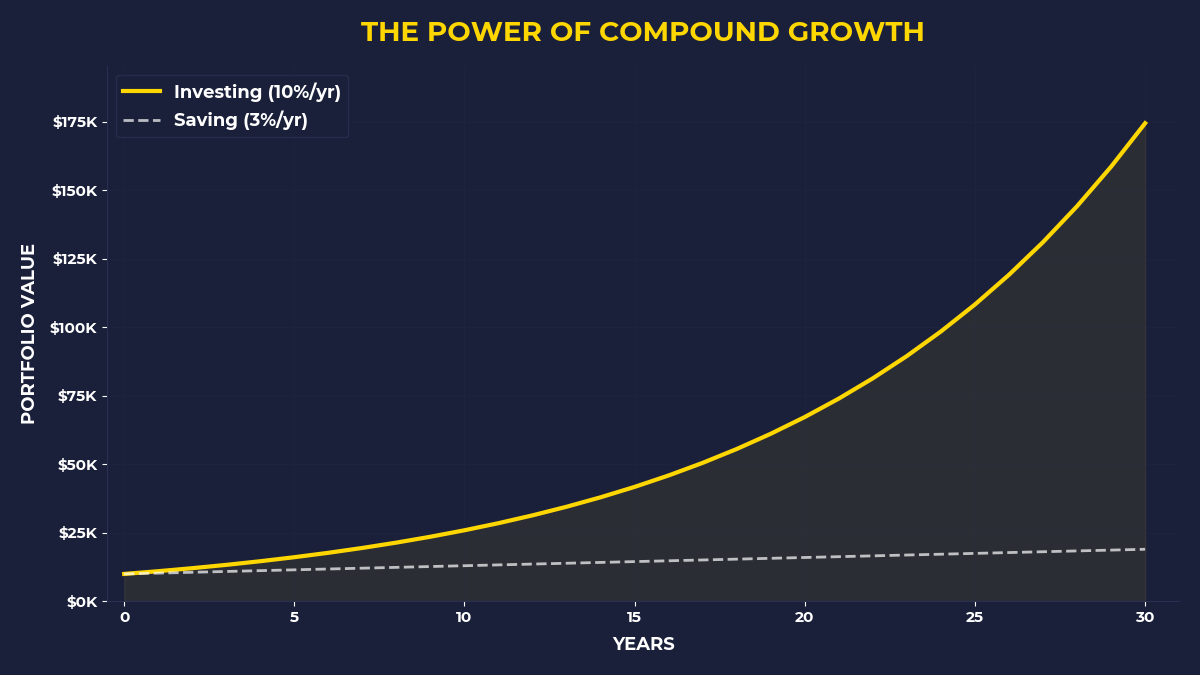

I bought an S&P 500 index fund — basically a tiny slice of the 500 largest American companies — and just let it sit there. By the end of the first year I had $1,340 in there, including some gains. It wasn’t life-changing money. But something else changed. I was, for the first time, on the receiving end of demand. Thousands of companies making money. Some of that money, however microscopically, was mine. I’d crossed a line I hadn’t even known existed.

Two years later I was putting in $400 a month. Not because I earned more — I did, a little — but because the habit had reorganized how I thought about every dollar I made.

If This Is You, Keep Reading

If you’re someone who works hard, earns a reasonable income, pays your bills on time, and still feels like you’re running on a treadmill that’s slowly speeding up — this post is for you.

If you’re someone who reads personal finance content and bounces because it all assumes you have $50,000 sitting around waiting to be optimized — this post is for you.

If you’re someone like Rachel, who did the math one night and felt that quiet bewilderment, that creeping sense that the rules of the game are not what you were told — this is absolutely for you.

The people this post is not for: those who already own significant income-producing assets and are looking for advanced optimization strategies. There are better resources for that. This is for the person still figuring out which side of the ledger to stand on.

The One Thing To Remember

Every month you spend money, you are voting for someone to get wealthy. The question is whether any of those votes ever come back to you. Most people spend their entire lives on the paying side of capital — sending rent checks, subscription fees, and car payments to people who own things — without ever buying a single asset that pays them back. The way out isn’t earning more or spending less. It’s asking a different question: not what should I do to make money, but what should I own that makes money while I live my life. That question, asked seriously and acted on with even modest consistency, is the actual dividing line between people who build wealth and people who wonder where it went.

This week: Before you pay your next bill, move a fixed amount — even $50, even $25 — into a brokerage account. Open one today if you don’t have one. The specific amount matters less than the order of operations. Buy first. Pay second. Do this once and you’ll understand something that a thousand articles about budgeting never gave you.

This month: Write down the five recurring payments you make every month — rent, subscriptions, insurance, whatever. For each one, ask: who owns the asset on the other side of this payment? Then ask: is there any version of this category where I could be the owner instead of the payer? You won’t act on all of them. But one of them might surprise you.

This year: Pick one asset that has consistent demand — an index fund, a rental unit, a small side project with a recurring revenue component — and buy a piece of it. Not a lot. Just something. The goal isn’t the amount. The goal is to get yourself onto the receiving side of demand, even slightly, so you understand from experience what ownership actually feels like. That feeling will do more for your financial life than any spreadsheet ever will.

]]>

🎬 Prefer watching? Check out the video version on YouTube: