Marcus — 37, software engineer in Seattle, pulling $118,000 a year — called me on a Tuesday night last February sounding genuinely shaken.

He’d just sold his index fund position. All of it. Every share he’d been quietly accumulating for six years, about $43,000 worth, liquidated in a single afternoon because the market had dropped 11% over three weeks and his stomach couldn’t take it anymore. He told me it felt like the smart, responsible thing to do. Protect what he had. Wait for the dust to settle. Buy back in when things “calmed down.”

He never bought back in. The market recovered 19% over the next eight months. Marcus watched it happen from the sidelines, paralyzed by a fear that the next drop was always just around the corner.

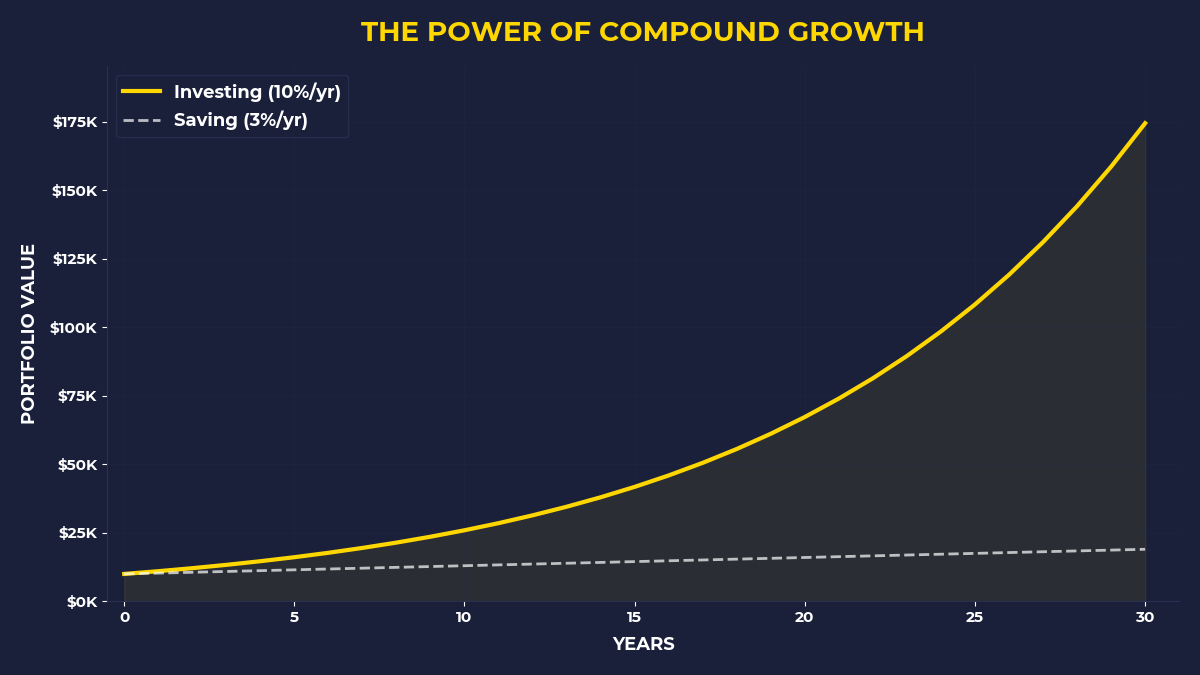

By December, his $43,000 would have been worth roughly $51,000. Instead, it was sitting in a savings account earning 0.4% annually, quietly losing ground to inflation every single day.

I Know Exactly What That Feels Like

I made a version of Marcus’s mistake when I was 29. Not with index funds — with a small stake in a dividend-paying REIT (that’s a real estate investment trust, basically a company that owns properties and pays you a cut of the rent). I’d put in $6,200. It dropped 18% in six weeks. I told myself I was being rational. I told myself I was “cutting my losses.”

What I was actually doing was letting a 200,000-year-old piece of brain circuitry — the part that evolved to help our ancestors run from predators — make decisions about 21st-century financial markets.

That’s the thing nobody tells you about money. The problem isn’t information. Marcus knew, intellectually, that markets recover. He’d read enough. He could explain dollar-cost averaging at a dinner party. The problem was that his brain was running software designed for a world where hesitation kept you alive, and in that world, a falling thing is a dangerous thing, and the correct response to danger is to get out.

Behavioral finance is just the formal name for studying why that happens. Why smart, educated, well-intentioned people make the same money mistakes over and over again. Not because they’re stupid. Because they’re human.

Here are the five traps I’ve watched destroy more wealth than any stock market crash ever could.

Trap 1: Your Brain Treats Losses Twice as Seriously as Gains

Psychologists call this loss aversion, and the research behind it is some of the most replicated in all of behavioral science. The short version: losing $100 feels roughly twice as painful as gaining $100 feels good. Which sounds like a minor quirk until you realize what it does to your investing behavior.

It means the moment a position turns red, your brain starts generating an anxiety signal that is physiologically disproportionate to the actual threat. Marcus’s $43,000 dropping to $38,300 felt — in his nervous system — like a catastrophe. Not a temporary fluctuation in the price of productive companies he owned pieces of. A catastrophe.

And so he sold. To make the feeling stop.

Here’s the reframe that changed how I think about this: a price drop is not a loss unless you sell. Before you hit the sell button, you own the same number of shares you owned yesterday. The underlying companies are still there, still generating revenue, still paying employees, still serving customers. The only thing that changed is the number some algorithm is currently willing to pay for your slice of them.

You didn’t lose anything. You just got an uncomfortable notification.

Trap 2: You Confuse a Familiar Story With a Safe Bet

Have you ever bought stock in a company just because you use their product and love it?

Most people have. It feels smart. You know the brand, you trust it, you see other people using it. That’s called familiarity bias, and it’s one of the sneakier traps because it disguises itself as due diligence.

I had a friend — Priya, 31, graphic designer in Chicago — who put $8,000 into a single streaming company in 2021 because she and everyone she knew was obsessed with it. She’d done “research.” She knew the subscriber numbers, she’d watched the CEO interviews, she felt genuinely connected to the business.

The stock dropped 75% between January and December 2022.

Loving a product tells you almost nothing about whether the equity is priced correctly. Those are two completely different questions. Capital doesn’t care about your feelings about a brand. Capital cares about demand — sustained, durable, hard-to-replicate demand — and whether you’re acquiring that demand at a price that makes sense.

Familiarity feels like knowledge. It isn’t.

Trap 3: You Wait for Certainty That Never Comes

This one is subtle. And it might be the most expensive trap of all.

After Marcus sold his position in February, I asked him when he planned to buy back in. He said, “When things stabilize.” I asked him what stabilize meant, exactly. He paused for a long time.

He didn’t have an answer. Because there is no answer. Markets never feel stable. There is always a reason to wait — an election, an inflation report, a geopolitical crisis, an interest rate decision, a tech earnings miss, a housing bubble rumor. The noise is infinite. The “right moment” never announces itself.

What Marcus was really doing was waiting for his anxiety to go away before he acted. But the anxiety doesn’t go away. It relocates. Once you sell and feel the temporary relief, the anxiety shifts to “what if it keeps going up without me?” — which is exactly what happened to him.

I remember sitting at my kitchen table in 2020, in late March, watching my brokerage app show numbers I’d never seen before. Everything was red. The news was apocalyptic. I had about $4,000 sitting in cash that I’d been meaning to invest for months. My brain was screaming at me to wait, that this wasn’t the bottom, that it would get worse. I sat there for three days, paralyzed.

I finally moved $3,200 into a broad market ETF on March 31st, 2020, feeling genuinely sick about it. By December of that year, that position was up 58%. Not because I was smart. Because I finally stopped waiting for certainty that was never going to arrive.

Trap 4: You Follow the Crowd Into the Expensive Seats

Look. This one is uncomfortable to talk about because it implicates all of us, including me.

The pattern is almost embarrassingly predictable: an asset class starts rising, people talk about it at dinner parties and on group chats, the rising price feels like confirmation that it’s a good idea, more people buy in, the price rises further, the story gets more compelling, even more people pile in — and then, somewhere near the top, the average person finally feels confident enough to participate.

That confidence arrives at exactly the wrong time.

This is herding behavior. And the cruel irony is that it feels like independent thinking. “I’ve been watching this for a while, I’ve done my homework, I feel good about this.” But what actually happened is that a rising price gradually dismantled your skepticism. The price movement was the argument. And now you’re in an expensive seat at a party that’s starting to wind down.

The counterintuitive move — the genuinely contrarian move — is to become interested when things are boring and ignored, and become cautious when everyone around you is excited. That is viscerally uncomfortable in both directions. Buying something nobody is talking about feels stupid. Staying cautious when your friends are making money feels even worse.

That discomfort is the price of entry. There is no version where you buy low without feeling like you might be making a terrible mistake.

Trap 5: You Optimize for Feeling Smart Instead of Building Equity

This is the trap that ties all the others together, and I say that as someone who spent years falling directly into it.

There’s a version of engaging with money that is really just a performance of financial competence. You read the reports. You follow the analysts. You have opinions about Fed policy and can explain what an inverted yield curve means. You make moves that you can justify to yourself and others. You feel like an investor.

But the actual question — the one that matters — isn’t “do I understand what’s happening in markets?” The actual question is: am I consistently acquiring equity in things that generate demand, and am I doing it in a way that lets compound growth do its work over time?

That’s it. That’s the whole game.

Warren Buffett didn’t build one of the largest fortunes in American history by having the most sophisticated macro views. He built it by buying pieces of businesses with durable demand — things people needed and kept needing — and then leaving those pieces alone long enough for the underlying economics to compound. The golf ball story is instructive here: as a kid, he found used golf balls near a course, cleaned them up, and sold them at $6 for a dozen. He didn’t spend the money. He rolled it into more assets. Then more. The genius wasn’t the golf balls. It was the loop — earn, buy something with demand, let it generate more, repeat.

The behavioral trap is spending your mental energy on sophisticated-sounding activity — market timing, sector rotation, following earnings calls — while the actual work, the boring, repetitive accumulation of equity in things that generate demand, goes undone.

Feeling smart is not the same as building capital. And for most of the people I know, it’s actively in competition with it.

What You Can Actually Do About This

If you’re someone who has watched their own reflection in Marcus’s story — someone who knows enough to know better but finds themselves selling at the bottom, waiting for certainty, following the crowd into expensive assets, or trading the performance of financial literacy for actual wealth-building — this section is for you.

The fix isn’t more information. You have enough information. The fix is structural.

You need systems that make the emotional mistakes harder to execute. Automatic monthly contributions that move before you see the money. A rule — written down, somewhere you’ll find it — that says “I do not sell during a decline of less than 30%, no matter what.” A second rule that says “when I feel excited about an asset everyone is talking about, I wait 30 days before buying.” Not because waiting is always right. Because excitement is a bad filter.

One more thing, and this is the hardest one: get genuinely clear on why you’re doing this.

Not “to retire comfortably.” That’s too vague to pull you through a 20% drawdown. I mean: what does your life actually look like when your assets generate enough cash flow that work becomes optional? What do you do on a Tuesday at 11am? Who do you call? What do you create? What does it feel like to not check the clock?

That image — specific, vivid, yours — is the only thing I’ve ever found that reliably overrides the panic signal when everything is falling and your brain is screaming at you to get out.

Capital is stored demand. Every share you hold is a small claim on the economic activity of real businesses serving real customers who will wake up tomorrow and still need what those businesses provide. Your job, the only job, is to keep accumulating those claims and not let your nervous system talk you out of them.

The One Thing To Remember

Your brain is not broken — it’s just running the wrong program for the environment you’re in. Loss aversion, herding, familiarity bias, the hunger for certainty: these were survival features, not bugs, for most of human history. They kept your ancestors alive. In a modern financial market, they will quietly transfer your wealth to the people who learned to recognize and override them.

Today: Write down the last financial decision you made that was driven by discomfort — selling during a dip, waiting for “clarity,” buying something because everyone was excited about it. Name the trap. Naming it is the first circuit-breaker.

This week: Set up one automatic recurring investment — even $75 a month — that moves on a fixed date without your involvement. Make the good behavior require zero willpower.

This month: Define your “why” in one specific sentence. Not “financial freedom.” Something like: “So that I can spend my Tuesdays writing / building / traveling / being present with my kids — without asking anyone’s permission.” Pin it somewhere you’ll see it when markets are ugly and your stomach is in knots. Because they will be. And you’ll need it.

🎬 Prefer watching? Check out the video version on YouTube: