The Paradox of Brilliant Poverty

I know engineers earning $200,000 who live paycheck to paycheck. I know doctors who postpone retirement because they can’t afford it. I know brilliant analysts who can predict market movements but somehow never build lasting wealth.

These aren’t dumb people making dumb decisions.

They’re asking the wrong question entirely. While everyone else obsesses over “What should I do to make money?” — the question that keeps 97% of people financially stuck — capital owners ask something completely different: “What should I buy?”

That shift in questioning isn’t semantic. It’s the difference between renting your intelligence to others and owning assets that work while you sleep. Between trading time for money and buying time with money.

Most smart people never make this shift. They optimize their careers, not their capital structure.

I Used to Think Intelligence Guaranteed Wealth

When I started investing at 23, I was certain my analytical skills would translate into financial success. I read every financial statement, memorized ratios, built complex models. I was working 70-hour weeks at a hedge fund, convinced that harder work and smarter analysis were the keys to wealth.

Look, I know how this sounds coming from someone who eventually figured it out. But back then, I was making the same mistake that keeps brilliant people poor: I was optimizing for income, not capital.

I remember the moment this became clear. A maintenance worker in our building — couldn’t have finished high school — mentioned he owned three rental properties. Meanwhile, I was pulling all-nighters analyzing biotech companies and living in a studio apartment because Manhattan rent ate 40% of my salary.

He understood something I didn’t: Capital isn’t about being smart. It’s about owning demand.

What Capital Actually Is (Not What You Think)

Here’s what I learned that changed everything: Capital isn’t money sitting in your account. Capital is stored demand — the structural ability to capture value from what people want, need, or can’t live without.

When you pay rent, that’s your demand flowing to someone’s capital. When you buy coffee, stream Netflix, or fill your gas tank — that’s your cash flow transferring to capital owners. Every monthly bill you pay is essentially an invoice from someone who figured out how to position themselves between you and something you need.

Think about Warren Buffett’s childhood golf ball business. He didn’t become wealthy because he was the smartest kid in Omaha. He became wealthy because he positioned himself between golfers and their demand for golf balls. He owned the supply of what people wanted.

The maintenance worker understood this instinctively. People need housing. Housing generates cash flow. Own enough housing, and other people’s rent payments fund your freedom.

Smart people miss this because they’re trained to solve problems with intelligence, not ownership.

Why Your Brain Sabotages Your Wealth

There’s a primitive instinct at work here — what psychologists call “reciprocity bias.” We’re wired to believe that if we give value, we’ll receive value in return. Work hard, get paid well. Be smart, get rewarded. Solve problems, build wealth.

This instinct served our ancestors well in small tribes where reputation mattered and relationships were everything. But in modern capitalism, reciprocity bias becomes a wealth trap.

You can be the most valuable employee at your company and still struggle financially. Why? Because you’re trading your intelligence for income instead of using your intelligence to buy assets.

The company you work for? It’s capital. The building you work in? Capital. The software you use? Capital. The brand that customers trust? Capital. You’re surrounded by capital that generates wealth for its owners while you generate income for yourself.

The Question That Changes Everything

What should I buy instead of what should I do?

This question is the great divider. It separates capital owners from wage earners, wealth builders from income optimizers, people who retire early from people who work until they die.

When young Warren Buffett found those golf balls, he could have focused on becoming the best golf ball finder in Omaha. He could have optimized his technique, worked longer hours, found more balls per day. That’s the “what should I do” mindset.

Instead, he asked: “What should I buy with this money?” He bought pinball machines. Then farm land. Then stock in companies. Each purchase generated cash flow that funded the next purchase. That’s compound capital formation.

The maintenance worker I mentioned? Same principle. His first rental property generated enough cash flow to help finance the second. The second helped finance the third. While I was getting smarter at analyzing companies, he was getting richer by owning them.

Why Creative Work Builds Capital (While Repetitive Work Burns Time)

Here’s something most people never consider: humans are naturally creative beings. We’re designed to build, create, and own things. But when you don’t have capital, almost all your creative energy gets consumed by repetitive work — work that serves someone else’s creative vision.

I learned this the hard way during my hedge fund years. I was incredibly good at financial analysis. I could spot value, identify trends, build models that predicted outcomes. But all that creativity was being channeled into making other people wealthy. I was the architect, but I didn’t own the building.

Capital changes this dynamic completely. When you own assets that generate cash flow, you free up your creative energy for your own projects. You can take risks, experiment, build something meaningful. You can say no to work that doesn’t align with your values.

This is why entrepreneurs often seem more fulfilled than high-paid employees. It’s not just about money — it’s about creative ownership.

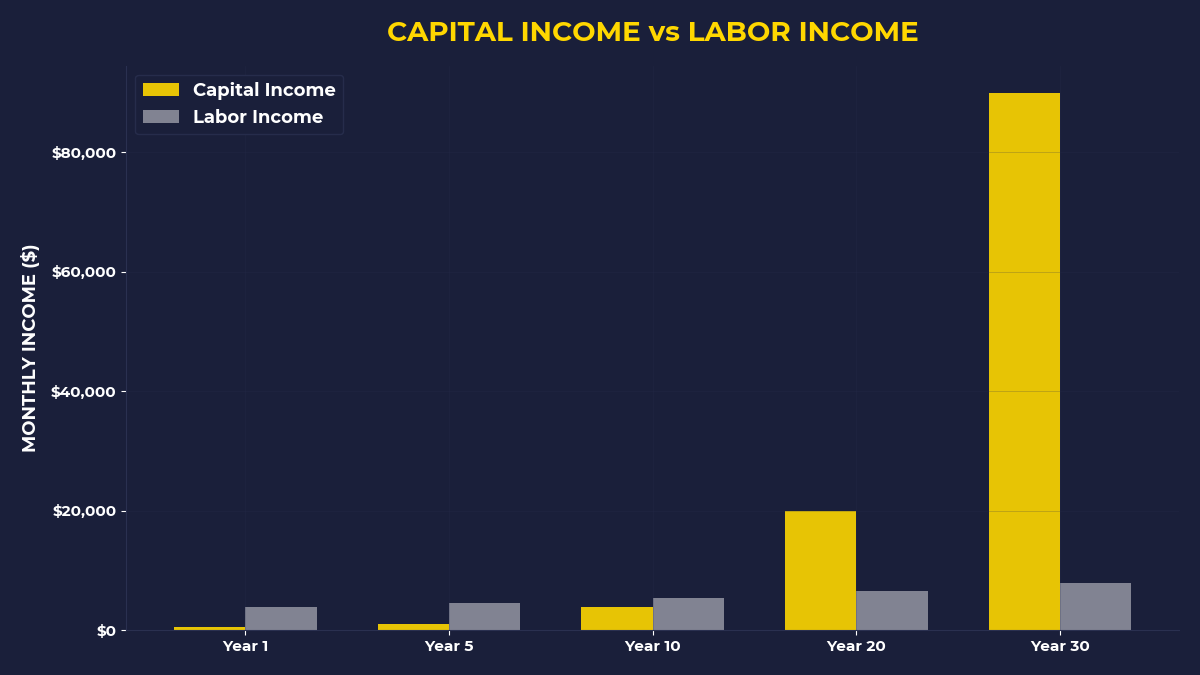

The Compound Capital System Most People Never Build

Want to know the real difference between smart people who stay poor and smart people who build wealth? The wealthy ones build systems that buy more assets automatically.

Consider this: In 1973, Harry Larson noticed people using coin-operated scales at his local drugstore. Instead of thinking “I should get a job servicing scales,” he thought “I should buy scales.” He invested $175 in his first machine, which generated $20 monthly. But here’s the crucial part — he used that $20 to buy another scale, then another.

Within a few years, Larson owned 70 scales generating $1,750 monthly in 1970s dollars. He didn’t just buy one asset and stop. He built a system where each asset funded the purchase of the next asset.

This is what economists call “capital accumulation,” but I prefer to think of it as momentum. Once you start buying assets instead of spending on consumption, each purchase makes the next purchase easier.

If You’re Still Trading Intelligence for Income

Look, I get it. You’re probably thinking: “This sounds great, but I don’t have capital to buy assets.” You’re making good money, but it all goes to bills, taxes, and lifestyle. There’s nothing left to invest.

Here’s the thing: that feeling is exactly what keeps smart people poor forever.

Robert Kiyosaki tells a story that stuck with me. When he was broke and living in a friend’s garage, facing overwhelming bills, he made a decision that seemed insane: he paid himself first. Before paying any bills, he bought assets. Then — and only then — he figured out how to pay the bills.

This forced him to find additional income sources, take on weekend work, be creative about money. But the key was this: his asset purchases weren’t optional. His bills became the variable expense.

Most people do the opposite. They pay all their bills first, then invest whatever’s left over. Which is usually nothing.

The Leverage That Smart People Miss

Even if you’re committed to buying assets, you can still think too small. The maintenance worker didn’t just buy one rental property and call it good. He bought three. The scale owner didn’t buy one machine — he bought 70.

This isn’t about greed. It’s about leverage — using systems and other people’s work to multiply your capital’s impact.

If you’re a high-income professional, you actually have an advantage here. Your income can fund asset purchases faster than someone making minimum wage. But only if you resist the lifestyle inflation that typically accompanies higher income.

Instead of upgrading your car, buy dividend stocks. Instead of a bigger apartment, buy REITs. Instead of expensive vacations, buy index funds. Use your intelligence to optimize your asset purchases, not your consumption.

What The Primal Investor Takes Away

• Question shift: Ask “What should I buy?” instead of “What should I do?” This single change redirects your intelligence toward capital formation instead of income optimization.

• Pay yourself first: Before paying bills, buy assets. Force yourself to find creative solutions for bills rather than creative excuses for not investing.

• Build momentum: Use cash flow from early assets to fund later asset purchases. Each investment should make the next investment easier, not harder.

• Think systems, not transactions: Don’t just buy assets — build systems that automatically reinvest returns into more assets. Compound capital formation is the goal.

• Leverage intelligence: Your analytical skills should help you buy better assets, not just earn higher wages. Intelligence applied to capital beats intelligence applied to labor every time.

The smartest person in the room is rarely the wealthiest. But the smartest person who consistently asks “What should I buy?” usually becomes both.

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.