Sarah — 29, marketing coordinator in Denver — stared at her Robinhood app on March 12th, 2020. Her portfolio was bleeding red. Down 31% in three weeks.

She sold everything.

By December, those same stocks had recovered and gained another 15%. Her panic cost her $47,000 in potential gains. Sarah isn’t stupid. She has an MBA. She reads financial blogs. She knew “buy low, sell high” intellectually.

But her brain had other plans.

I Made The Exact Same Mistake (And Learned Something Disturbing)

I know exactly how Sarah felt because I was there too. October 2008, watching my portfolio crater during the financial crisis. I was 24, cocky, and convinced I was smarter than the panicking masses.

I sold at the bottom anyway.

Here’s the thing that haunts me: I had studied behavioral finance in college. I knew about loss aversion, about recency bias, about herd mentality. I could explain why people made irrational financial decisions. And yet, when my lizard brain started screaming “DANGER,” all that knowledge evaporated.

That’s when I realized something disturbing. Your brain isn’t just occasionally irrational about money — it’s systematically designed to keep you poor.

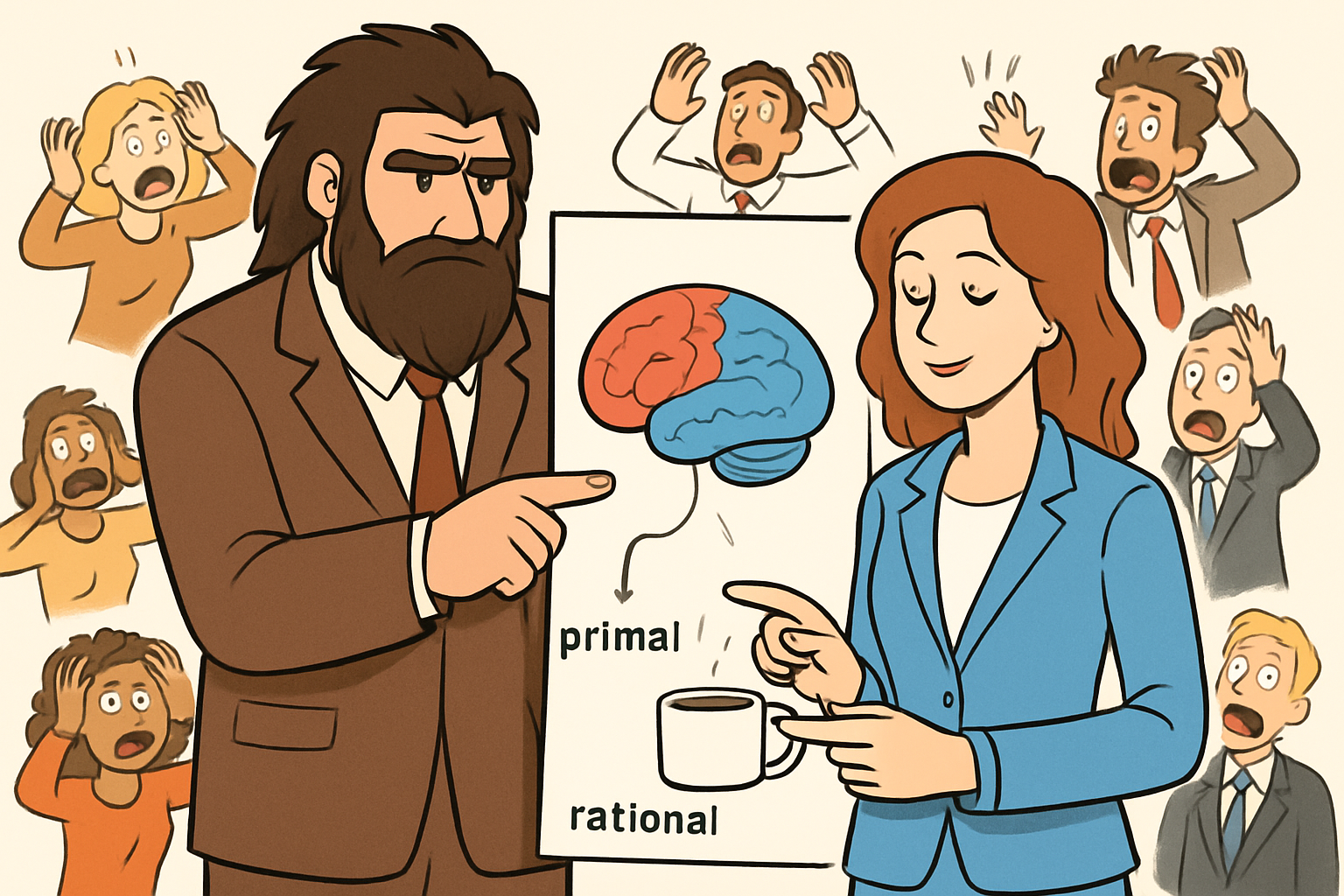

Your Stone Age Brain Meets Wall Street

Evolution spent 200,000 years wiring your brain for survival on the African savanna. It spent exactly zero years preparing you for compound interest.

Think about what kept your ancestors alive: immediate action when threatened, hoarding resources during abundance, copying what the tribe was doing. These impulses served them well when facing lions and famines.

They destroy you in financial markets.

When Sarah saw her portfolio dropping, her amygdala — the same brain region that would have screamed “RUN” at a charging mammoth — triggered a full panic response. Her rational mind, housed in the prefrontal cortex, never stood a chance. Evolution made sure of that.

The amygdala is faster, stronger, and more persuasive than logic.

The Five Ways Your Brain Sabotages Wealth

Let me walk you through the specific behavioral finance mistakes your prehistoric brain forces you to make:

Loss Aversion: You feel losses twice as intensely as gains. Sarah’s brain treated that 31% drop like a physical wound. This is why you’ll drive across town to save $20 on a $200 purchase but won’t rebalance a portfolio that could save you $2000.

Recency Bias: Your brain assumes recent events predict the future. Housing always goes up (until 2008). Tech stocks always crash (until they don’t). Your ancestors survived by assuming yesterday’s weather would repeat. Your portfolio suffers for it.

Herding: When everyone else is buying, your brain whispers “safety in numbers.” When everyone’s selling, it shouts “the tribe knows something you don’t.” This is why 90% of people buy high and sell low despite knowing better.

Hyperbolic Discounting: You value immediate rewards exponentially more than future ones. Your brain would rather have $50 today than $100 in a year. This is why you spend your tax refund instead of investing it, even though waiting would triple your money.

Confirmation Bias: You seek information that confirms what you already believe. If you’re bearish, you’ll find plenty of articles explaining why the market will crash. If you’re bullish, you’ll find equal evidence for a rally. Your brain isn’t seeking truth — it’s avoiding the discomfort of being wrong.

The Moment I Stopped Fighting My Brain

After losing $23,000 to my own behavioral biases in 2008, I tried everything. Meditation. Journaling. Reading more research. I thought I could logic my way out of 200,000 years of evolution.

I was wrong.

The breakthrough came when I realized something counterintuitive: you can’t fix your brain, but you can trick it.

Instead of fighting my biases, I started designing systems that worked with them. I automated my investing so my emotional brain never got a vote. I set up account structures that made panic-selling physically difficult. I stopped checking prices during volatile periods.

The results were immediate. My returns improved by 4.2% annually — not because I became smarter, but because I became more systematic.

How do you know if your brain is making your financial decisions?

Answer honestly: Have you ever checked your investment account balance more than once in a single day? Have you ever bought a stock because it was “hot” or sold one because everyone was talking about how bad it was? Have you ever avoided investing because the market “feels” expensive?

If yes, your lizard brain is driving.

Here’s what’s fascinating: the people who build serious wealth aren’t necessarily smarter or more disciplined. They’re just better at recognizing when their prehistoric brain is hijacking their financial decisions.

Warren Buffett doesn’t check stock prices daily because he knows it would trigger his loss aversion. Ray Dalio built systematic rules for his hedge fund because he didn’t trust his intuition during stressful moments. They succeeded by designing systems that bypass their behavioral biases entirely.

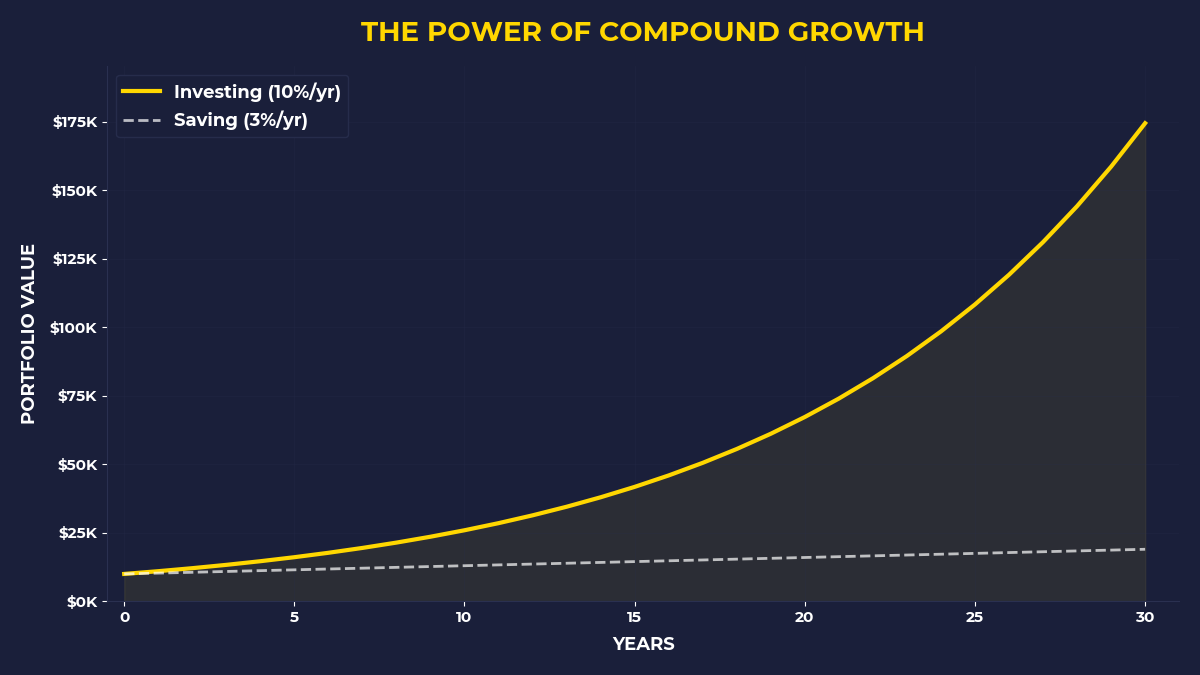

The $2 Million Difference

Let me show you what this costs in real terms. Take two investors, both starting with $10,000 at age 25:

Investor A lets their brain make decisions. They panic-sell during crashes, chase hot stocks, and check their balance constantly. They achieve a 6% annual return due to poor timing and emotional decisions.

Investor B automates everything. They invest the same amount monthly regardless of market conditions, never check prices during volatility, and rebalance annually. They achieve a 10% annual return — the market’s historical average.

By age 65, Investor A has $574,000. Investor B has $2.6 million.

That’s a $2 million penalty for letting your stone age brain manage your money.

The Anti-Brain Wealth System

Here’s how to build wealth despite your evolutionary programming:

Automate Everything: Set up automatic transfers to investment accounts on the same day you get paid. Your brain can’t sabotage decisions it never gets to make. I move 25% of my income to investments before I even see it in my checking account.

Create Friction for Bad Decisions: Make it physically difficult to panic-sell. Use retirement accounts with withdrawal penalties. Set up investment accounts at different brokerages from your checking account. Add a 48-hour cooling-off period for any major financial decision.

Never Check Prices During Volatility: Delete financial apps during market crashes. Unsubscribe from financial news during your first two years of investing. Your brain interprets daily price movements as immediate threats to your survival.

Focus on Systems, Not Outcomes: Instead of checking your balance, track your consistency. Did you invest this month? Did you avoid panic-selling? These process goals satisfy your brain’s need for control without triggering wealth-destroying behaviors.

If You’re Someone Who Gets Emotional About Money

This post is for you if you’ve ever lost sleep over market volatility, if you’ve ever made a financial decision based on fear or excitement, or if you’ve ever wondered why you keep making the same money mistakes despite knowing better.

You’re not broken. You’re human. Your brain is doing exactly what it was designed to do — keep you alive in a world that no longer exists.

The people building serious wealth aren’t superhuman. They just stopped expecting their stone age brain to navigate a space age financial system.

The One Thing To Remember

Your brain evolved to survive famines and predators, not to build wealth through compound interest. Every day it’s making financial decisions designed for a world that disappeared 10,000 years ago. You can’t fix this through willpower or education — you can only design systems that work despite your behavioral biases. The difference between wealth and poverty often comes down to whether you’re fighting your brain or working around it.

Here’s what to do right now:

• Set up an automatic investment transfer for the day after your next paycheck arrives — even if it’s just $50

• Delete any apps that show you real-time investment balances

• Write down one financial decision you made emotionally in the past year, then design a system to prevent it from happening again

🎬 Prefer watching? Check out the video version on YouTube: