The most dangerous financial advisor in your life sits between your ears. Your brain — sculpted over 300,000 years to survive in small hunting groups — is spectacularly unfit for building wealth in modern markets. Every day, it whispers ancient survival code that was brilliant for avoiding lions but is ruinous for owning capital.

I learned this the expensive way.

When My Caveman Brain Cost Me Real Money

In March 2020, I watched my portfolio drop 31% in three weeks. The fear felt physical. My amygdala — the walnut-sized alarm system that kept my ancestors alive — was screaming: danger, escape, sell everything now. The pain of watching numbers fall triggered the exact neural pathways that once made humans run from predators.

I held. Barely.

But here’s what haunts me: 89% of retail investors didn’t. They sold at the bottom, locking in losses that took years to recover. Their primitive brains hijacked rational thought and executed a survival strategy that was perfect for the African savannah but devastating for compound returns. The same mental software that once saved lives now systematically destroys wealth.

Your brain doesn’t know the difference between a portfolio drawdown and a charging mammoth. Both trigger identical fight-or-flight responses that made evolutionary sense 50,000 years ago but cost you money today. This isn’t a character flaw — it’s a design feature of human psychology that capital markets exploit ruthlessly.

The Four Primitive Programs Running Your Financial Life

Behavioral finance research reveals that most financial decisions aren’t rational calculations. They’re emotional reflexes powered by ancient code that runs automatically, below conscious awareness. Here are the four programs most likely costing you capital right now:

Loss Aversion: Your brain treats losing $1,000 as roughly twice as painful as gaining $1,000 feels good. This asymmetry made evolutionary sense — losing food or shelter could mean death, while extra resources provided diminishing survival benefit. In markets, this translates to holding losing positions too long (hoping to break even) while selling winners too early (locking in gains before they disappear). Kahneman and Tversky documented this bias in 1979, but traders still exhibit it daily.

Recency Bias: Your brain assumes recent events predict future patterns. If the last three hunts were successful, the next probably will be too. If the last three failed, abandon this territory. Applied to investing, this means buying after bull markets (when prices are high) and selling after bear markets (when they’re low). The pattern is so predictable that fund flow data shows retail investors consistently buy high and sell low, missing most long-term returns.

Herding Instinct: For 99% of human history, going against the tribe meant death. Your ancestors survived by copying what everyone else was doing — if the group ran, you ran. Today, this same instinct makes you buy when “everyone” is buying (tops) and sell when “everyone” is selling (bottoms). The dot-com bubble of 2000 and the housing bubble of 2007 weren’t rational valuations — they were mass herding events that enriched contrarian investors while devastating followers.

Present Bias: Your brain heavily discounts future rewards in favor of immediate gratification. A bird in the hand was literally worth two in the bush when survival was uncertain. This bias makes you spend today’s income on consumption rather than investing in future cash flows. It’s why 76% of Americans live paycheck to paycheck despite having access to the greatest wealth-building markets in history.

Why Smart People Make Dumb Money Decisions

Here’s the cruel irony: intelligence doesn’t protect you from behavioral finance traps. Sometimes it makes them worse.

I know PhD economists who panic-sold in March 2020. I know software engineers earning $300,000 who have zero equity because they “can’t afford” to invest. I know lawyers who’ve read every investing book but still chase last year’s hot stocks. Intelligence amplifies rationalization — smart people are better at creating logical-sounding explanations for emotional decisions.

The problem isn’t lack of information. It’s that your primitive brain processes market information through survival filters that worked for hunting and gathering but fail spectacularly for capital allocation. When Tesla stock drops 20%, your brain doesn’t see a potential opportunity — it sees threat, danger, loss. The same neural circuits that once detected rustling bushes now interpret red numbers as existential risk.

Smart money understands this. While retail investors panic-sell during corrections, institutional capital systematically buys the dips. Warren Buffett’s famous advice to “be greedy when others are fearful” isn’t folksy wisdom — it’s a behavioral finance strategy that exploits predictable human psychology.

The Wealth Transfer Hidden in Plain Sight

What looks like market volatility is actually a massive wealth transfer from emotional to rational actors. Every market cycle, the same pattern repeats:

Phase 1: Prices rise. Greed (the psychological drive to acquire more resources) kicks in. Retail investors buy, chasing returns.

Phase 2: Prices peak. Smart money sells to emotional buyers at inflated prices.

Phase 3: Prices fall. Fear (the drive to avoid loss) dominates. Retail investors sell at losses to smart money at discounted prices.

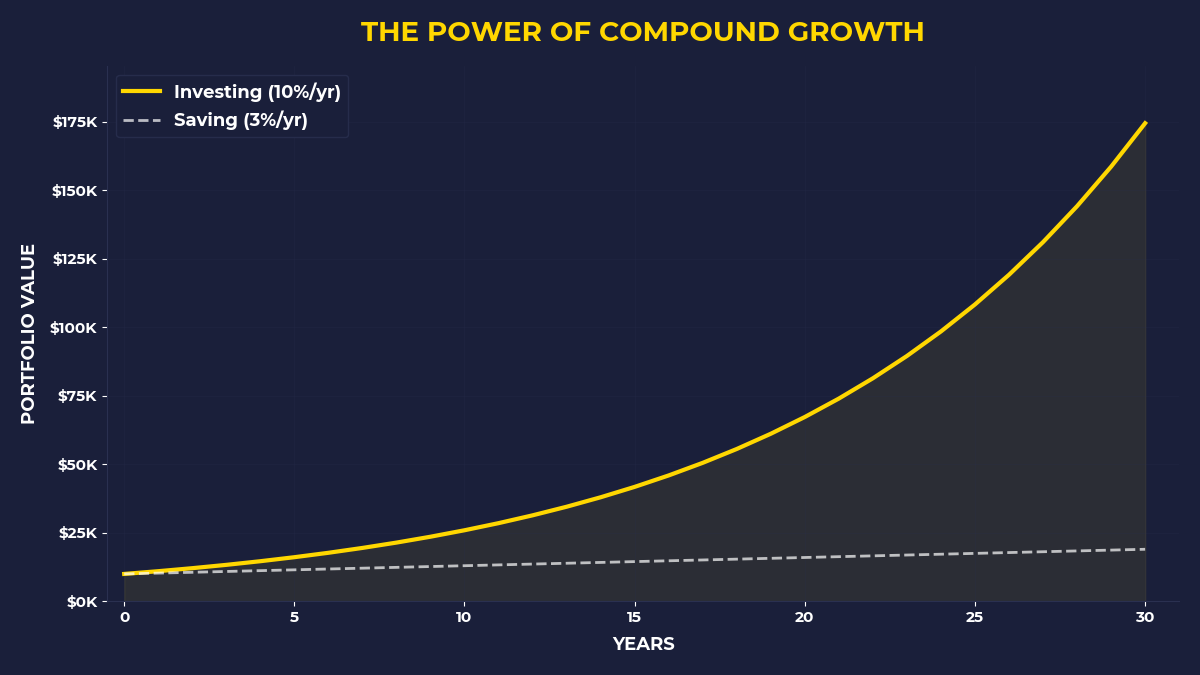

Between 1999 and 2018, the S&P 500 returned 5.6% annually. But the average equity investor earned just 3.9% — a 1.7% annual gap caused entirely by behavioral mistakes. Over 20 years, that gap cost the typical investor $400,000 in forgone wealth. Your primitive brain literally costs you decades of financial freedom.

How do you debug 300,000 years of evolution?

You can’t eliminate these instincts — they’re hardwired. But you can build systems that work with your psychology rather than against it. The key is accepting that you’re not rational and designing around that reality.

Automate Everything: Remove emotions from the equation. Set up automatic transfers from checking to investment accounts on payday. Your present bias wants to spend first and invest later (which never happens). Automation forces the opposite sequence. I automatically invest 30% of every paycheck before I see the money, eliminating the temptation to “just this once” skip investing.

Think in Systems, Not Outcomes: Your brain fixates on daily portfolio changes because it evolved to detect immediate threats. Force yourself to think in decades, not days. I check my brokerage account quarterly, not daily. The less frequently you look, the less your primitive brain can interfere with long-term wealth building.

Embrace Productive Paranoia: Channel your natural loss aversion into defensive investing. Instead of trying to pick winners, focus on not losing. Own businesses with wide moats, pricing power, and diversified revenue streams. Your paranoid brain is actually useful here — it helps you spot real risks that optimistic investors miss.

Pre-Commit to Contrarian Actions: Write down what you’ll do during the next market crash before it happens. “When the market drops 20%, I will invest an additional $10,000.” When fear hits, you’ll have rational instructions to follow instead of emotional impulses. Ulysses bound himself to the mast because he knew he’d be tempted by the sirens. You need similar preparation for market volatility.

The Capital Owner’s Advantage

Once you understand behavioral finance, you realize that capital markets are primarily wealth transfer mechanisms from emotional to rational actors. Most participants are running Stone Age software in an Information Age system, creating persistent inefficiencies that prepared investors can exploit.

But here’s the deeper insight: your primitive instincts don’t just hurt your investment returns — they prevent you from becoming a capital owner in the first place. Fear of risk keeps you in “safe” savings accounts earning 0.5% while inflation runs 3%. Present bias makes you buy consumer goods instead of income-producing assets. Herding behavior leads you to follow conventional career advice that trades time for money rather than building equity.

The wealthy understand something most people never grasp: capital ownership is the only reliable path to financial freedom because it removes your primitive brain from the wealth equation. When you own assets that generate cash flows, you’re no longer dependent on daily emotional decisions about money. The businesses work, the dividends arrive, the compound returns accumulate — regardless of how you feel.

What The Primal Investor Takes Away

• Your brain is hardwired with survival instincts that systematically destroy wealth in modern markets — accept this reality instead of fighting it

• Automate investments to bypass present bias, check portfolios quarterly to avoid recency bias, and pre-commit to contrarian actions during market stress

• Focus on becoming a capital owner rather than optimizing investment returns — ownership removes your emotional brain from wealth-building decisions

• Use your natural paranoia productively by buying defensive assets with wide moats rather than chasing high-growth speculation

• Recognize that market volatility is primarily a wealth transfer from emotional to rational actors — position yourself on the receiving end

Your primitive brain will never be your ally in building wealth. But once you stop fighting evolution and start designing around it, those ancient instincts become someone else’s expensive mistake and your systematic advantage.

🎬 Prefer watching? Check out the video version on YouTube: