The Morning David Counted His Bills

David Martinez — 29, marketing coordinator in Denver — spread his monthly bills across his kitchen table like evidence in a crime scene. Rent: $1,650. Car payment: $389. Phone: $85. Gym: $49. Netflix, Spotify, groceries, insurance, utilities. The stack kept growing.

He earned $4,200 a month after taxes.

By the time he finished counting, $3,847 was already spoken for before he’d even seen his paycheck. What bothered him wasn’t the math — it was the realization that every single one of these payments was flowing to someone who owned something he needed.

I Used To Think Bills Were Just Life

I know exactly how David felt because I spent my twenties doing the same calculation every month. Same spreadsheet, same sinking feeling, same acceptance that “this is just how money works.”

I remember sitting in my apartment in 2018, looking at my bank account after all my monthly bills cleared. $247 left. For an entire month. I earned decent money as a project manager, but somehow I never had any.

Here’s what I didn’t understand then: Those bills weren’t just expenses. They were invoices from capital owners.

Every month, I was sending my cash directly to people who owned what I needed to survive. My landlord owned the building. Toyota Financial owned my car loan. Verizon owned the cell towers. The gym owner had real estate and equipment.

I owned nothing that anyone else needed.

What Your Bills Actually Reveal

Look at David’s monthly expenses again, but this time ask a different question: Who owns what?

His $1,650 rent payment goes to someone who owns real estate in a location people want to live. His car payment goes to a bank that owns the loan secured by an asset. His phone bill goes to a company that owns infrastructure millions of people need daily.

Every bill David pays represents stored demand. Someone figured out what people would need repeatedly, acquired the thing that generates that demand, and now collects payment for it.

This is what capital actually is — not money sitting in a bank account, but ownership of things that create ongoing demand.

Think about that gym membership. The owner bought equipment once. David pays $49 every single month to use it. Multiply David by 800 other members, and that’s $39,200 in monthly recurring revenue from equipment the owner bought years ago.

The Question That Changes Everything

What would happen if David flipped the script?

Instead of asking “How do I afford all these bills?” what if he asked “How do I own things that generate bills for other people?”

I started asking myself this question in 2019 after a conversation with my friend Sarah, who owns three rental properties in Austin. She mentioned that her tenants’ rent payments cover all three mortgages plus $1,400 in monthly profit.

“Wait,” I said. “You mean other people are paying for your real estate?”

“Every month,” she said. “While I sleep.”

That conversation broke something open in my brain.

The Warren Buffett Golf Ball Strategy

Warren Buffett figured this out when he was 11 years old. He found lost golf balls around local courses, cleaned them up, and sold them back to golfers for 6 cents each. Simple arbitrage — find demand, meet demand, collect payment.

But here’s the part most people miss: Buffett didn’t just find golf balls forever. He used his profits to buy assets that generated income without his daily labor. First a pinball machine he placed in a barbershop. Then more pinball machines. Then other businesses.

Each purchase gave him a slice of someone else’s recurring demand.

By age 16, he owned paper routes that other kids worked for him. He was collecting payment from customers while other people did the delivery. The demand was stored in his ownership structure.

Why Most People Never Make The Switch

David earns $50,400 a year. But $46,164 of it goes to bills — to other people’s capital. He’s left with $4,236 to live on, let alone invest.

This is the trap.

Most financial advice tells people like David to “invest 10% of your income.” But when 92% of your income is already committed to paying capital owners, where’s the 10% supposed to come from?

The conventional approach doesn’t work because it ignores the fundamental structure: You’re sending nearly all your money to people who own things before you can even think about owning things yourself.

The Capital-First Strategy

Here’s what I learned from studying people who actually build wealth: They pay themselves first. Not “save money first” — pay themselves first.

Robert Kiyosaki talks about this in his books. Even when he was broke and living in a friend’s garage, he forced himself to invest in assets before paying bills. When he couldn’t cover everything, he worked extra jobs to make up the difference.

This sounds crazy until you understand the psychology: When you pay bills first, you’re training yourself to prioritize other people’s capital over your own. When you invest first, you’re training yourself to think like a capital owner.

I started doing this in 2020. Before I paid rent, utilities, or anything else, I moved $400 into my brokerage account. Even when it meant eating ramen for two weeks.

Especially then.

What David Should Actually Do

If David wants to break the cycle, he needs to start thinking like Harry Lassen.

Lassen was mentioned in a book that influenced young Buffett. He noticed people using a coin-operated scale at a drugstore — seven people in just a few minutes. He asked the store owner about it and learned the scale generated $20 a month in profit.

Lassen bought his own scale for $175. Soon it was generating $98 monthly. But here’s the key: He used that $98 to buy more scales. Eventually he owned 70 scales across the city, generating $1,750 per month.

Same principle, different era.

David could start by asking: “What do people in my neighborhood need repeatedly?” Food, laundry, parking, storage, WiFi, entertainment. Instead of just consuming these things, how could he own a piece of them?

Maybe he can’t buy a rental property yet. But he could buy shares in REITs that own thousands of rental properties. Maybe he can’t start a subscription business. But he could own shares in companies that run subscription businesses.

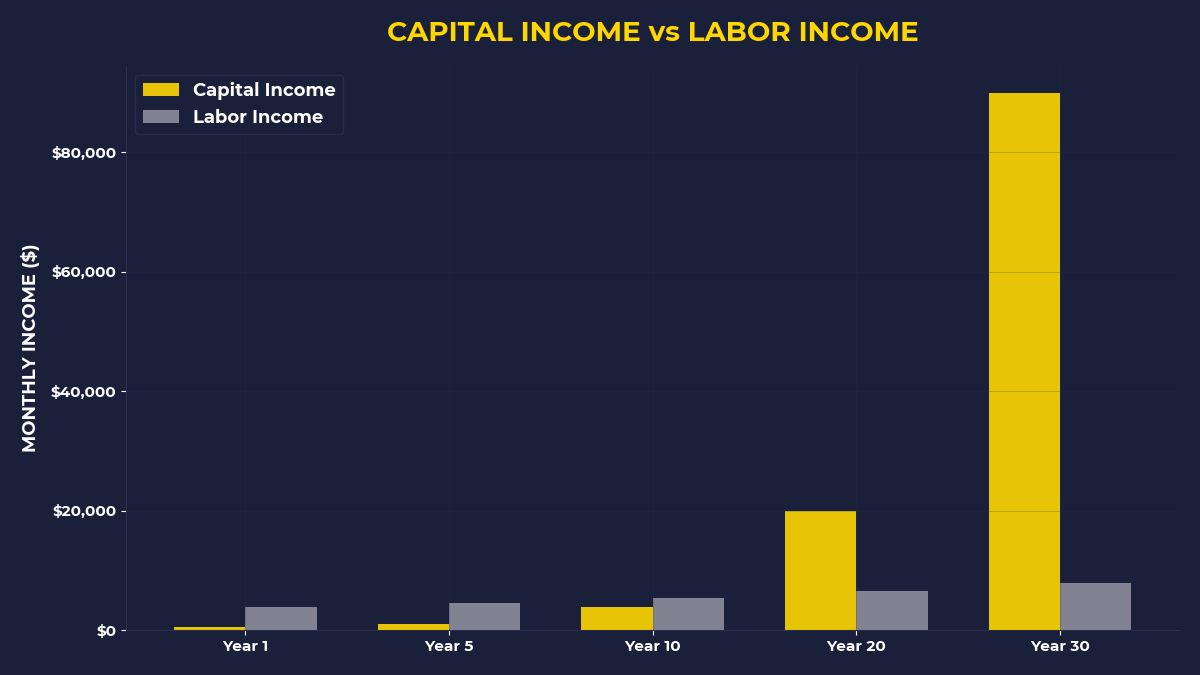

The Compound Effect of Ownership

Here’s what happens when you flip from bill-payer to capital owner:

Year 1: You own $4,800 in assets (that $400 monthly investment). Your bills stay the same, but now you’re getting dividends.

Year 3: You own $15,600 in assets. The dividends help cover some bills.

Year 7: You own $38,400 in assets. The cash flow from your ownership starts replacing your salary.

Year 12: You own $89,000 in assets. The income from things you own exceeds what you earn from work.

This isn’t about becoming a millionaire. It’s about switching sides in the capital game.

If You’re Still Paying Everyone Else First

Look, I get it. When you’re living paycheck to paycheck, investing feels impossible. When rent is due and your account is low, buying stocks feels irresponsible.

But here’s what I learned the hard way: As long as you prioritize bills over ownership, you’ll always be in the same position next month, and next year.

The system is designed to keep you sending money to capital owners forever.

The only way out is to start owning capital yourself, even if it’s uncomfortable at first.

The One Thing To Remember

Your monthly bills are a perfect map of where capital creates value in your life. Every payment you make represents someone who figured out how to own what you need. The goal isn’t to eliminate bills — it’s to start collecting them from other people. Capital is stored demand, and demand is everywhere around you.

• Before you pay any bill this month, invest $50 in something that generates income for others (even an S&P 500 index fund)

• List your three biggest monthly payments and research who profits from them

• Ask “What could I own?” instead of “What should I do?” for the next 30 days

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.