My neighbor Jake — 29, software engineer, $95,000 salary — knocked on my door last Tuesday night holding a stack of self-help books. “I’ve read twelve of these things this year,” he said, dropping them on my kitchen table. “Morning routines, productivity hacks, networking strategies. I’m doing everything they tell me to do. So why am I still broke every month?”

I picked up one of the books. The 7 Habits of Highly Effective People. Another one: Atomic Habits. A third: How to Win Friends and Influence People. All classics. All focused on the same thing.

What to do.

Jake had been asking himself the wrong question for years. And so had I, until I figured out what the 3% of people who actually build capital ask instead.

I Was Asking the Wrong Question Too

I know exactly how Jake felt because I was there too. When I was 26, fresh out of college, I had a decent job and a head full of advice about doing things. Work harder. Network more. Learn new skills. Get certifications. Wake up at 5 AM. Meal prep on Sundays.

Here’s the thing.

I followed all of it. I was productive as hell. I networked until my business card collection could wallpaper a small bathroom. I learned Python, took a finance course, read every business biography I could find.

And at the end of two years of relentless self-optimization, you know what I had to show for it? A slightly higher salary and the exact same financial stress. Every month, the same cycle: paycheck comes in, bills go out, scramble to save whatever’s left.

The breakthrough came when I was sitting in a coffee shop, overhearing a conversation between two guys at the next table. One was complaining about his rent going up $200. The other guy — quiet, maybe 40, wearing a simple t-shirt — said something that stopped me cold:

“I stopped asking what I should do about money problems. Now I ask what I should buy.”

The Question 97% of People Never Ask

What should I buy?

Not what should I do. Not how can I work harder. Not what skills should I develop.

What should I buy.

Think about that for a second. When was the last time someone gave you financial advice that started with “buy this” instead of “do this”? When was the last time you walked into a bookstore and saw a title like “What Rich People Buy While Poor People Work Harder”?

Never.

Because our entire culture is built around the mythology of doing. Work harder. Be more productive. Optimize your morning routine. Learn more skills. The assumption is always the same: if you’re not getting ahead financially, you’re not doing enough.

But here’s what I learned from that guy in the coffee shop, and from every wealthy person I’ve studied since: capital owners don’t primarily think about what to do. They think about what to buy.

Why Warren Buffett Picked Up Golf Balls

Warren Buffett’s first business wasn’t analyzing financial statements or reading annual reports. When he was a kid, he collected lost golf balls from the rough at the local country club. Dirty work. Dangerous work, sometimes — those balls ended up in ponds and thick brush.

He’d clean them up and sell them by the dozen for $6. Good money for a kid in the 1940s.

But here’s the part that matters: Buffett didn’t just keep doing this forever. He took the money from selling golf balls and bought something. First, it was pinball machines that he placed in barbershops. Then, shares of stock. Then, entire businesses.

At every step, he asked: “What should I buy with this money?”

Not “How can I find more golf balls?” Not “How can I clean them faster?” Not “Should I wake up earlier to beat the other kids to the golf course?”

What should I buy.

Every dollar that came in from his labor went toward purchasing something that would generate cash flow without requiring more of his time.

The Weight Scale That Changed a Life

I came across another story that hammered this point home. A guy named Harry Larson was in a drugstore when someone asked him how much he weighed. He looked around, spotted a coin-operated scale, dropped in a penny, and stepped on.

Over the next few minutes, seven more people used that scale.

Harry got curious. He asked the store owner about it. The owner explained that he rented the scale from a company and kept 25% of the revenue — about $20 per month from this one machine.

Most people would have walked away thinking “interesting business model” and gone on with their day. Harry walked out, went to his bank, withdrew $175, and bought three weight scales for rental.

Within a month, he was earning $98. But here’s the kicker: he took that $98 and bought more scales. Then more. Eventually, he owned 70 scales generating $1,750 per month.

Same question. What should I buy.

What About You?

I can already hear the objections. “I’m not Warren Buffett. I don’t have capital to buy rental scales. I’m just trying to pay my bills.”

Look.

That’s exactly the mindset that keeps 97% of people trapped. You’re thinking about what you should do to pay bills instead of what you should buy to generate the cash flow that pays bills.

Let me tell you about my friend Sarah — 31, marketing manager, $68,000 salary. Two years ago, she was in the same spot as Jake. Paycheck to paycheck, despite doing everything “right.” Reading productivity books, taking online courses, networking like crazy.

Then she shifted the question. Instead of asking “What should I do to make more money?” she started asking “What should I buy to make money work for me?”

Her first answer was simple: shares of an S&P 500 index fund. Every month, before paying a single bill, she bought $300 worth. Even when it meant scrambling to cover rent. Especially then.

Why before bills? Because paying bills first trains your brain to think like an employee. Capital owners pay themselves first, then figure out how to cover expenses.

After six months of this, something interesting happened. Sarah started a side business — not because she needed extra work, but because she needed extra money to buy more assets. She freelanced on weekends, not to pay bills, but to buy more index funds.

Today, her investment portfolio generates about $800 per month in dividends and appreciation. Still not enough to retire, but enough to change how she thinks about money. She’s not working to pay bills anymore. She’s working to buy things that pay bills for her.

The Laundromat Test

Here’s how you can tell the difference between the two mindsets. Imagine you want to start a laundromat.

The “what should I do” person thinks: “I’ll rent a space, buy some machines, and run it myself. I’ll work hard, provide great customer service, maybe stay open late to beat the competition.”

The “what should I buy” person thinks: “I’ll buy a location with existing foot traffic, lease commercial-grade machines that require minimal maintenance, hire someone to manage day-to-day operations, and use the cash flow to buy a second location.”

Same business. Completely different approach. The first person bought themselves a job. The second person bought a cash-generating asset.

The first person is thinking about what to do. The second is thinking about what to buy.

Wild, right?

Your Next $100

If you’re someone who’s tired of reading about morning routines and productivity hacks while your bank account stays the same, this shift changes everything. You stop asking “How can I work harder?” and start asking “What can I buy with my next $100 that will work harder than I ever could?”

Maybe it’s shares of a dividend-paying stock. Maybe it’s equipment for a side business. Maybe it’s a small rental property down payment. Maybe it’s a digital course you can sell while you sleep.

The specific answer matters less than asking the right question.

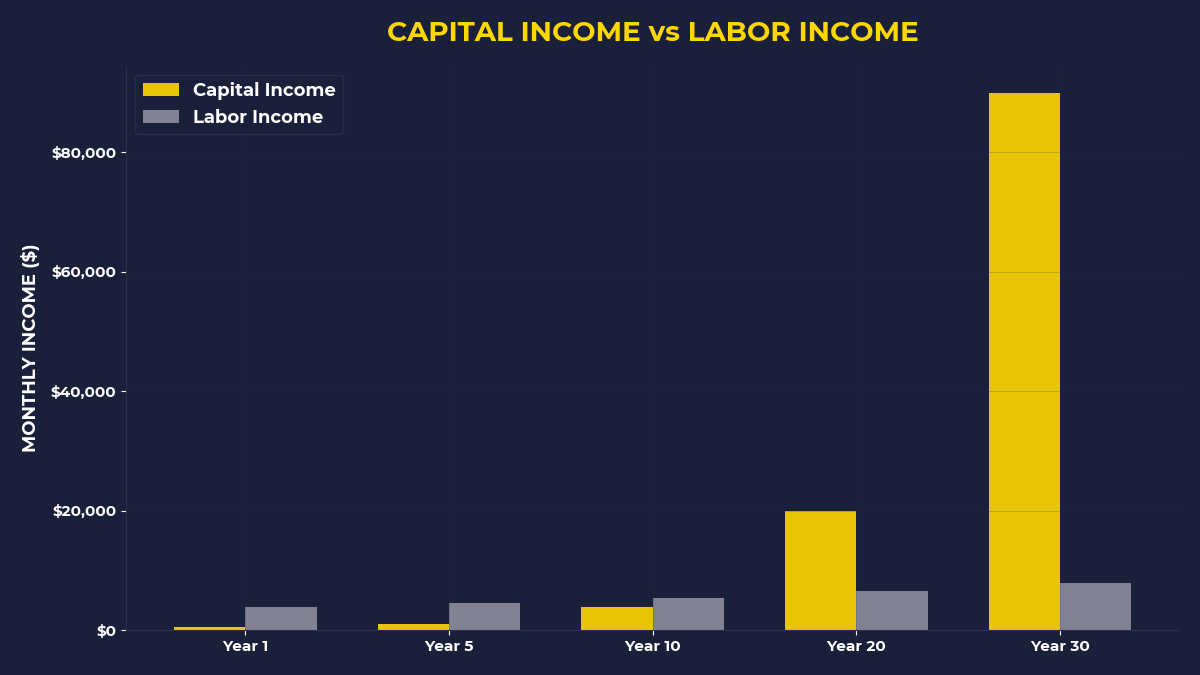

Because here’s the truth that 97% of people never figure out: your labor has a ceiling. There are only 24 hours in a day. Your energy is finite. Your skills have limits.

But capital has no ceiling. Money working for you doesn’t get tired. It doesn’t need coffee breaks. It doesn’t call in sick. It works nights, weekends, and holidays. And when you buy the right things, they buy more things, which buy more things.

That’s compound growth. That’s time freedom. That’s the difference between working for money and having money work for you.

The One Thing To Remember

Every successful investor I know made the same mental shift. They stopped optimizing their behavior and started optimizing their purchases. They stopped asking “What should I do?” and started asking “What should I buy?” Because in a capitalist economy, ownership is the only path to freedom. Everything else is just expensive labor dressed up as a career.

Here’s what you can do today:

• Before you pay your next bill, buy $50 worth of an index fund or dividend stock — even if it means scrambling to cover expenses

• Write down three things you could buy (not do) in the next six months that might generate cash flow

• Ask yourself this question every time you’re tempted to buy a productivity course: “What could I buy instead that would make money while I sleep?”

🎬 Prefer watching? Check out the video version on YouTube: