Marcus — 29, software developer in Portland — called me last Tuesday with a question that made my stomach drop. “I’ve been reading about contrarian investing,” he said. “Should I buy some beaten-down tech stocks while everyone’s panicking?”

I knew Marcus was about to make the same mistake I made seven years ago.

The Contrarian Trap That Keeps You Poor

Here’s the thing. When most people hear “contrarian investing,” they think it means buying what everyone else is selling. GameStop when it’s crashing. Netflix after a bad quarter. Some obscure cryptocurrency that financial Twitter is dunking on.

I thought the same thing when I was 28.

I remember sitting in my apartment in Chicago, scrolling through finance blogs, feeling like I’d cracked the code. While everyone was selling energy stocks in 2016, I’d buy them. While everyone was avoiding retail after Amazon killed everything, I’d find the survivors. I was going to be the guy who zagged when everyone else zigged.

Six months later, I was down 23% while the S&P 500 was up 11%.

The problem wasn’t my stock picks. The problem was my definition of contrarian.

What Real Contrarian Investing Actually Looks Like

Real contrarian investing isn’t about buying different stocks. It’s about making a fundamentally different choice with your money before you ever think about stocks.

Let me tell you about Sarah — 31, marketing manager in Austin — who figured this out before I did.

Sarah made $67,000 a year. Every month, like clockwork, her paycheck disappeared into the same places: rent ($1,400), car payment ($320), insurance ($180), groceries ($400), phone bill ($85), streaming services ($47), gym membership ($49). The usual parade of bills that everyone accepts as normal.

But Sarah did something that 97% of people never do. She flipped the order.

On payday, before paying a single bill, Sarah moved $300 into her brokerage account. Not after rent. Not after groceries. First. Before anything else touched her paycheck.

Her landlord could wait three days for rent. Her credit card company could wait a week. But her future self got paid immediately, every single month, no exceptions.

That’s contrarian investing.

Why Everyone Else Gets Your Money First

Think about your last paycheck. Where did it go?

Your landlord got their cut. Your car loan company got theirs. Your insurance company, your phone company, your grocery store, your streaming services — they all got paid before you did.

You worked 40 hours that week, but a dozen different capital owners got your money before you got to keep any of it.

This is the opposite of contrarian thinking. This is following the crowd in the most expensive way possible.

The crowd pays everyone else first and invests whatever’s left over. The contrarian investor pays themselves first and figures out the bills later.

Wild, right?

The Question That Changes Everything

Here’s what I learned after losing money on those “contrarian” stock picks: the real question isn’t “what stocks should I buy when everyone else is selling?”

The real question is: “what should I buy instead of paying bills?”

When Sarah moved that $300 first, she wasn’t just buying index funds. She was buying herself out of the cycle that keeps 97% of people sending their paychecks to capital owners for their entire working lives.

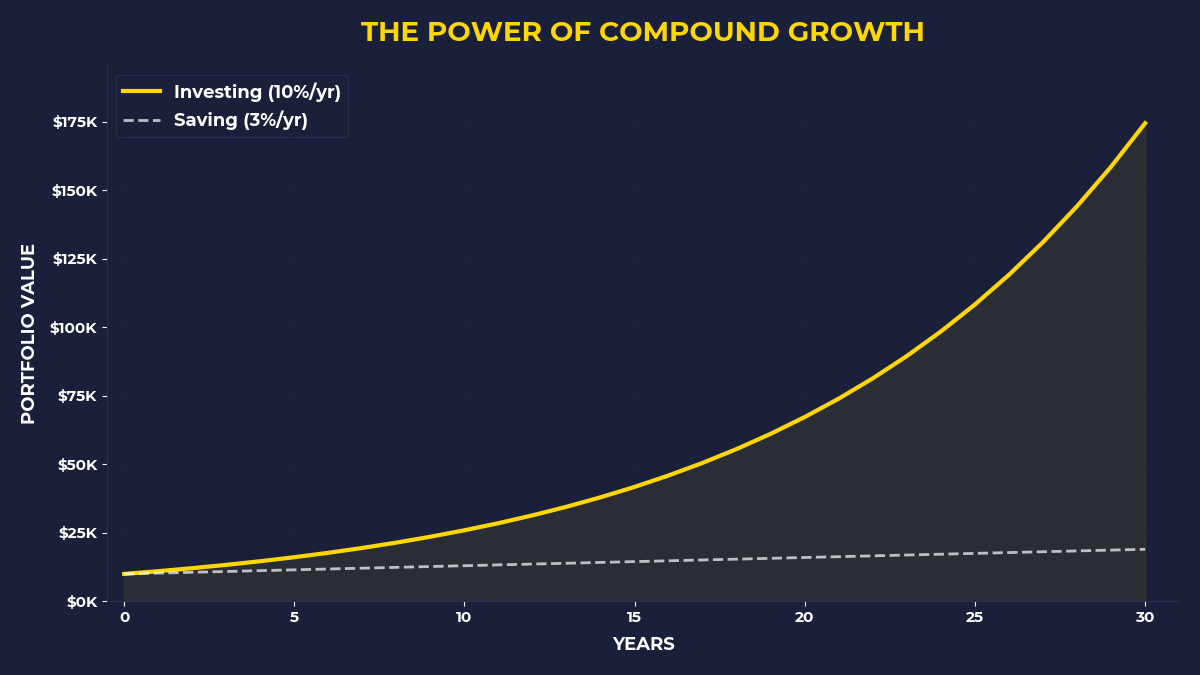

Every month, that $300 went to work for her instead of for someone else. After two years, she owned $8,100 in assets that were growing. Her rent payments? Still $1,400 a month, still making her landlord richer.

The math is brutal when you see it clearly.

Why This Feels Impossible (And Why You Should Do It Anyway)

Look, I know what you’re thinking. “I can barely cover my bills now. How am I supposed to invest first?”

I had the same thought. The same fear.

But here’s what happened when Sarah started paying herself first: she got creative with everything else. She found a cheaper phone plan. She canceled two streaming services she barely used. She bought groceries at Aldi instead of Whole Foods.

When your investments come first, you optimize your expenses. When your expenses come first, you rationalize why you can’t invest.

That’s the difference between contrarian thinking and crowd thinking.

The crowd says: “I’ll invest when I have more money.”

The contrarian says: “I’ll have more money when I start investing.”

The Real Contrarian Move in 2024

The most contrarian thing you can do right now isn’t buying some stock that everyone hates. It’s buying assets while everyone else is paying bills.

While your coworkers are stressed about their car payments, you’re building equity in companies that make cars.

While your friends are complaining about their rent, you’re owning pieces of the companies that build apartment complexes.

While everyone else is sending their money to capital owners, you’re becoming a capital owner.

That’s the real contrarian investment strategy.

If You’re Someone Who Actually Wants to Build Wealth

This post isn’t for people who want to feel smart by picking stocks that might go up. This is for people who are tired of working their entire lives and having nothing to show for it except a pile of bills.

If you’re someone who looks at your bank account and wonders where all your money goes, this is for you.

If you’re someone who wants to own something instead of just paying for everything, this is for you.

If you’re someone who’s ready to stop following the crowd straight into financial mediocrity, this is definitely for you.

The One Thing to Remember

Contrarian investing isn’t about being different with your stock picks. It’s about being different with your priorities. The crowd pays bills first and invests the leftovers. The contrarian invests first and figures out the bills later. This single decision — who gets your money first — determines whether you spend your life making other people rich or building your own wealth.

Here’s what you can do today:

• Set up an automatic transfer from your checking to your investment account for the day after you get paid, before any bills come out

• Start with whatever amount makes you slightly uncomfortable — if $100 feels safe, make it $150

• Buy a broad market index fund like VTI or VOO with that money every month, no matter what the market is doing

🎬 Prefer watching? Check out the video version on YouTube: