Here’s what I thought capital was when I started investing: money in my checking account earning 0.02% interest. Maybe some bonds. Definitely my 401k contributions going to index funds I couldn’t pronounce.

I was spectacularly wrong.

Capital isn’t the cash sitting in your account waiting for you to “put it to work.” Capital is stored demand — the economic right to say yes to rare asymmetric opportunities while everyone else scrambles for wages. It’s the difference between receiving invoices and sending them.

Most people confuse having money with owning capital their entire working lives. They optimize savings rates and emergency funds while the actual capital accumulates in someone else’s account. Every month, they send their paychecks to capital owners through rent, subscriptions, car payments, and grocery bills. Then they wonder why building wealth feels impossible.

The brutal truth? Your current understanding of capital theory is probably making everyone else rich except you.

Why Famous Singers Understand Capital Better Than Most Investors

I used to wonder why celebrities made millions while hardworking people struggled financially. Sure, they had talent, but plenty of talented people never got rich. What was the real difference?

The answer hit me when I stopped thinking about their “work” and started thinking about their capital structure.

A famous singer doesn’t just perform songs. They own intellectual property that generates royalties while they sleep. Their brand creates sustained demand that transforms into recurring cash flows. One hit song can produce income for decades through streaming, licensing, and covers by other artists.

Compare this to a construction worker who might be more skilled, more dedicated, and work longer hours. The worker trades time for wages. The singer owns demand.

Here’s the key insight: capital equals stored demand, not stored money.

When thousands of people want to hear a particular song, that demand gets stored in streaming platforms, radio stations, and licensing deals. The singer owns a piece of that demand structure. The construction worker owns none of the houses he builds.

This explains why Warren Buffett’s net worth grew from $1 million in 1962 to over $100 billion today while earning a $100,000 salary from Berkshire Hathaway. His capital — ownership stakes in businesses with sustainable demand — compounded at roughly 20% annually for six decades. His wages stayed flat by choice.

Your Monthly Bills Are Invoices From Capital Owners

Look at your bank statement from last month.

How many charges represent payments to capital owners versus payments for your own capital accumulation?

Rent or mortgage: payment to real estate capital owners. Car payment: payment to automotive capital owners. Netflix, Spotify, Amazon Prime: payments to platform capital owners. Groceries: payments to retail and consumer goods capital owners. Insurance: payments to financial capital owners.

I remember sitting in my first apartment after college, looking at my budget spreadsheet. Eighty-seven percent of my income went directly to capital owners before I had any choice in the matter. The remaining 13% got split between food, gas, and whatever was left for “investing.”

This is the opposite of capital theory. I was optimizing my role as a cash flow generator for other people’s capital while barely participating in capital accumulation myself.

The real insight came when I flipped the question: instead of asking “How can I afford these payments?” I started asking “How can I become the person receiving these payments?”

Why Most People Think Capital Is Money (And Stay Poor Because Of It)

The average American thinks capital means having $10,000 in their savings account earning 4.5% annually.

Wrong category entirely.

That’s just stored money losing purchasing power to inflation. Capital is stored demand — ownership of structures that capture ongoing human needs and convert them into cash flows.

Consider Warren Buffett’s childhood golf ball business. Young Warren would collect lost golf balls from water hazards and woods around local courses, clean them up, and sell them in packages of twelve for six dollars. The business worked because golfers consistently demanded replacement balls.

But here’s what made it capital instead of just labor: Buffett eventually hired other kids to find and clean the balls while he focused on the sales system. The demand for golf balls was stored in his business structure, generating cash flows whether he personally worked or not.

When Buffett used those profits to buy pinball machines for barbershops, he created another demand-storage mechanism. Barbershop customers wanted entertainment while waiting. The machines captured that demand automatically.

By age 16, Buffett owned multiple paper routes and farmland that produced income independent of his daily labor. He understood that capital meant owning demand, not accumulating money.

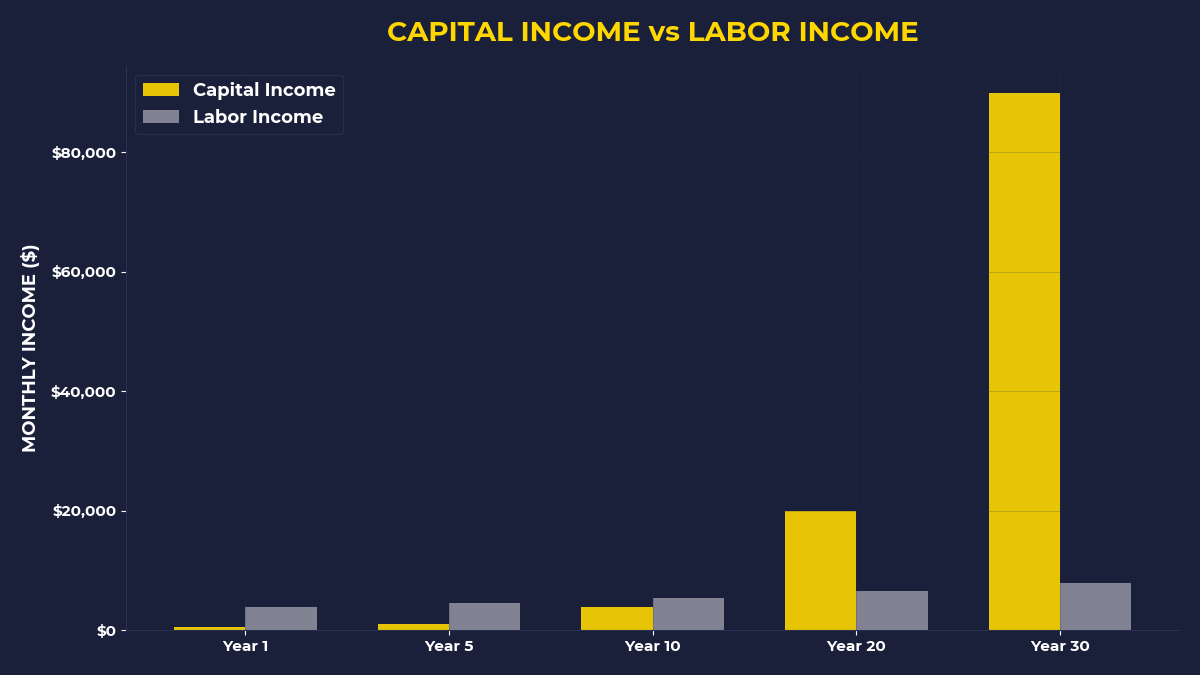

The Compound Interest Mistake Everyone Makes

Here’s where most capital theory explanations go wrong: they focus on compound interest instead of compound ownership.

Einstein allegedly called compound interest the eighth wonder of the world. Fine. But compound interest on what?

If you compound interest on savings accounts or bonds, you’re compounding at rates that barely keep pace with inflation. If you compound ownership of demand-generating assets, you’re compounding actual wealth.

Buffett’s golf ball story illustrates true compounding. He didn’t just save the six dollars from each sale. He used those cash flows to buy more demand-capturing assets: more pinball machines, paper routes, and eventually farmland. Each asset generated cash flows that purchased additional assets.

This is why the advice to “pay yourself first” only works if you understand what “paying yourself” actually means.

Most people interpret this as contributing to retirement accounts or building emergency funds. Better than nothing, but still missing the point.

Paying yourself first means buying ownership stakes in demand-generating structures before paying anyone else’s capital owners. It means asking “What should I buy?” instead of “What should I save?”

Why AI Changes Everything About Capital Theory

The artificial intelligence revolution isn’t creating better tools for workers. It’s creating better tools for capital owners.

Think about what happened when Netflix introduced recommendation algorithms in 2006. The technology didn’t help video store workers compete more effectively. It helped Netflix capture more demand by making their platform stickier. Blockbuster filed for bankruptcy in 2010.

Today’s AI follows the same pattern. Large language models help software companies build better products faster. Computer vision helps manufacturers reduce labor costs. Predictive analytics help retailers optimize inventory and pricing.

None of these improvements increase wages. They increase the value of owning the companies that deploy them.

If you’re accumulating capital in businesses that benefit from AI deployment, the technology amplifies your wealth. If you’re selling labor to businesses that deploy AI, the technology reduces your leverage.

This creates a critical fork in capital theory for our generation. Understanding AI as a capital multiplier versus a job threat determines which side of the wealth transfer you end up on.

The Question That Separates Capital Owners From Everyone Else

I spent my first five years out of college asking the wrong question about money.

Instead of “What should I do to earn more?” I should have asked “What should I buy to own more?”

The first question leads to career optimization, skill building, and salary negotiation. All valuable, but fundamentally limited by the hours in your day and the energy in your body.

The second question leads to capital accumulation. It forces you to think like someone who receives payments instead of someone who makes payments.

When Buffett’s friend Harry Lason saw a coin-operated scale in a drugstore and noticed seven people use it in fifteen minutes, he didn’t ask “How can I get a job in the scale industry?” He asked “How can I buy my own scales?”

Lason withdrew $175 from his bank account and bought three scales to place in different locations. Within a month, he was earning $98 in monthly passive income — more than many full-time workers earned in 1930.

The insight that impressed Buffett wasn’t the income itself. It was Lason’s next move: he used the cash flows from the first three scales to buy sixty-seven additional scales. He compounded ownership instead of compounding savings.

Why Your Emergency Fund Keeps You Poor

Here’s an uncomfortable truth about emergency funds: they train you to think like someone who expects emergencies instead of someone who creates opportunities.

The standard advice suggests keeping three to six months of expenses in a high-yield savings account. This sounds responsible, but it reveals a fundamentally defensive mindset about capital allocation.

Real capital theory works differently. Instead of preparing for emergencies, you prepare for asymmetric opportunities. Instead of storing money for potential problems, you store optionality for potential breakthroughs.

Consider what happens during market crashes. In March 2009, the S&P 500 hit its financial crisis low after falling 57% from its October 2007 peak. People with emergency funds felt secure about their cash positions. People with capital allocation skills bought assets at generational discounts.

The emergency fund holders preserved their purchasing power. The capital accumulators multiplied their purchasing power. The S&P 500 gained 250% over the following four years.

This doesn’t mean living paycheck to paycheck or taking reckless risks. It means reframing your relationship with cash reserves. Emergency funds represent defensive capital allocation. Opportunity funds represent offensive capital allocation.

What The Primal Investor Takes Away

Capital theory isn’t about having money — it’s about owning demand. The sophisticated investor focuses on four key distinctions that separate capital owners from everyone else:

• Replace savings goals with ownership goals. Instead of targeting account balances, target ownership percentages of demand-generating assets. Track your monthly capital purchases, not your monthly savings rate.

• Ask “What should I buy?” before “What should I do?” Every financial decision starts with this question. Career moves, side projects, and investment choices all flow from ownership thinking instead of labor thinking.

• Compound ownership, not just interest. Use cash flows from existing capital to purchase additional capital. Think like Buffett buying scales with scale profits, not like savers earning 4% on cash.

• Treat bills as invoices from your future competition. Every payment to someone else’s capital structure teaches you what demand looks like. Study where your money goes to understand what demand you could capture.

Your bank account balance reveals nothing about your capital position. Your ownership stakes reveal everything. The goal isn’t accumulating money — it’s accumulating the right to say yes when everyone else has to say no.

🎬 Prefer watching? Check out the video version on YouTube:

")