The Safest Investment Strategy Is the One That Feels Most Dangerous

I used to think contrarian investing meant buying beaten-down stocks while everyone else was selling.

That’s what the books taught me. Find the unloved sectors. Buy when there’s blood in the streets. Wait for the crowd to panic, then swoop in like some financial vulture. I tried it during the March 2020 crash, picking up airline stocks and cruise lines while everyone was screaming about the end of travel.

Some of those trades worked. Most didn’t.

Here’s what I discovered after losing real money: 97% of people think contrarian investing is about stock selection. They’re focused on the wrong end of the equation. The real contrarian move isn’t what you buy — it’s fighting the primitive wiring that keeps you from building capital in the first place.

Your Brain Is Running Ancient Code in Modern Markets

Think about this for a moment. Your monthly paycheck hits your account on Friday. By Sunday night, you’ve already allocated most of it to bills, groceries, that subscription you forgot to cancel, and maybe dinner out because you “deserve it” after working all week.

Sound familiar?

You just demonstrated the exact opposite of contrarian thinking. You paid everyone else first — your landlord, the grocery store shareholders, Netflix executives, restaurant owners. You sent your cash flow directly to capital owners while keeping none for yourself.

This isn’t a budgeting problem. It’s a wiring problem.

Your brain runs on loss aversion, the primitive instinct that makes potential losses feel twice as painful as equivalent gains feel good. When you think about investing your grocery money instead of spending it, your amygdala fires warning signals: “What if you run out of food? What if the market crashes? What if, what if, what if…”

The truly contrarian move is doing the exact opposite of what this ancient code demands.

What Warren Buffett Understood at Age 13

When Buffett was a kid collecting golf balls at the local course, he wasn’t thinking like a worker. Workers ask: “How can I make more money doing this?”

Buffett asked: “How can I buy assets that make money without me?”

That’s the question that separates capital owners from everyone else. But here’s where it gets interesting — and where most people’s contrarian investing psychology breaks down completely.

After collecting enough golf balls to buy a pinball machine, Buffett didn’t celebrate by spending the money. He didn’t upgrade his bike or buy better golf ball collection equipment. He bought the machine and put it in a barbershop, where other people fed it quarters while he was at school.

The contrarian move wasn’t buying the pinball machine. It was resisting the immediate gratification of spending his hard-earned money on himself.

Why Your Emergency Fund Is Training You to Stay Poor

Let me share something uncomfortable. The conventional wisdom about emergency funds — save 3-6 months of expenses in a savings account — is secretly training you to think like a worker, not an owner.

Here’s the logic they teach you: Keep cash available because emergencies happen. Job loss, medical bills, car repairs — life is unpredictable, so you need liquid money as insurance.

Sounds reasonable, right?

But look at what this actually does to your brain. Every time you accumulate money, your first instinct becomes: “Better keep this safe in case something goes wrong.” You’re literally programming yourself to hoard cash instead of converting it to assets.

The contrarian move? Use that emergency fund to buy your first piece of capital.

I know, I know. This feels dangerous. Your loss aversion is screaming right now. “What if I lose my job and the market crashes at the same time? What if I need the money and it’s tied up in stocks?”

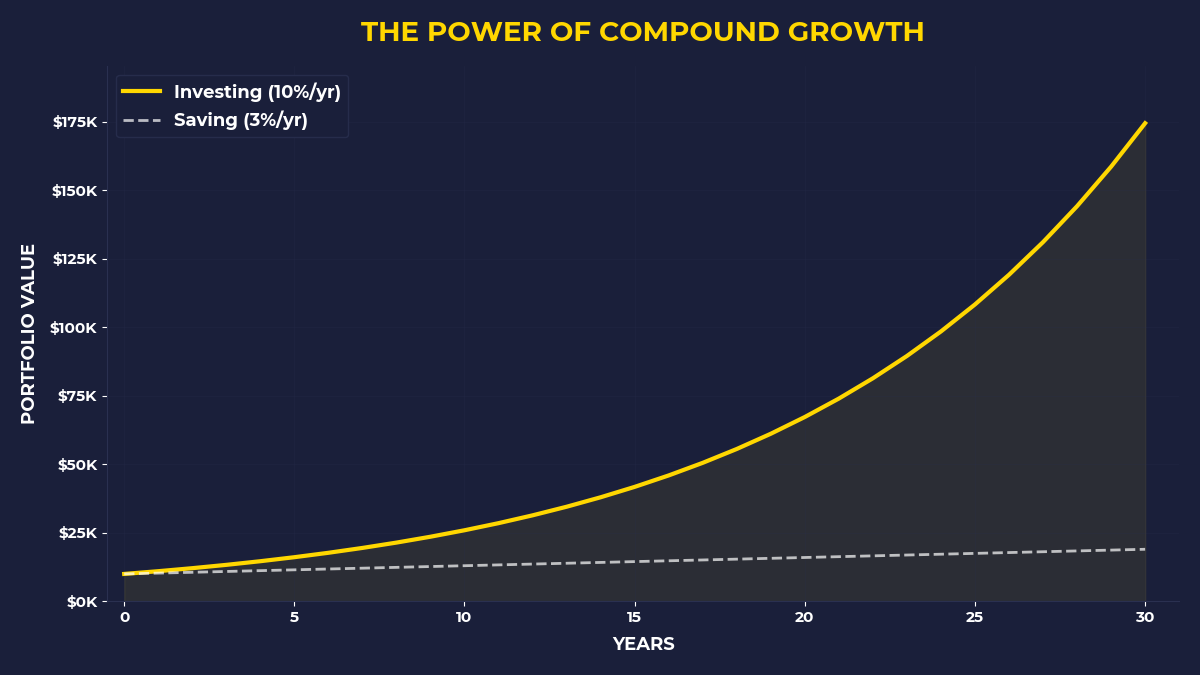

Here’s what happened when I finally made this move in 2019. I took $15,000 I’d been keeping “safe” in a savings account earning 0.5% and bought shares in a boring utility company and an S&P 500 index fund. Six months later, I did lose my job. But instead of panicking and selling, I picked up freelance work and lived lean for a few months.

Those investments? They’re worth $23,000 today. My “emergency fund” would be worth $15,200.

The Real Contrarian Edge Is Behavioral

Warren Buffett’s famous advice — “Be fearful when others are greedy, and greedy when others are fearful” — isn’t really about market timing. It’s about recognizing when your primitive brain is making decisions for you.

During the 2008 financial crisis, the S&P 500 dropped 57% between October 2007 and March 2009. Everyone knew stocks were “cheap.” Everyone knew this was the buying opportunity of a lifetime. Everyone knew the market would eventually recover.

And yet, equity mutual funds saw net outflows of $234 billion in 2008 and 2009 combined.

Why? Because knowing and doing are separated by millions of years of evolution. When your tribe is running from the tiger, the guy who stops to think about whether this is actually the best decision gets eaten. Fear overrides logic because fear kept your ancestors alive.

The contrarian investor recognizes this pattern and acts anyway. Not because they’re brave — because they understand their brain is running code designed for a world that no longer exists.

What Most People Miss About Capital Formation

Here’s the thing nobody talks about in those contrarian investing strategy guides: the hardest contrarian move isn’t buying unpopular stocks. It’s choosing to build capital instead of consuming it.

Every month, you make a choice. Send your paycheck to other people’s assets (rent, groceries, entertainment) or use it to buy your own assets first.

Most people think they can’t afford to invest. They’re wrong — they can’t afford not to.

Let me show you what I mean. The median American household spends $3,526 per month on housing, $4,942 on transportation, and $4,464 on food according to 2022 Bureau of Labor Statistics data. That’s $12,932 going directly to capital owners every single month.

But ask that same household to invest $500 per month in index funds? “Too risky. We can’t afford it.”

This is loss aversion in action. The guaranteed loss of your capital to other people feels safer than the potential loss from market volatility.

The Capital Question That Changes Everything

I learned this from studying how wealth actually gets built. Rich families don’t ask their kids: “What do you want to be when you grow up?” They ask: “What do you want to own?”

That question rewires everything.

Instead of thinking about careers and salaries and working harder, you start thinking about systems and cash flows and leverage. Instead of asking “How can I make more money?” you ask “How can I buy assets that make money?”

The Korean entrepreneur who taught me this principle put it perfectly: most people spend their entire lives answering the wrong question. They optimize for “What should I do?” when they should be optimizing for “What should I buy?”

What The Primal Investor Takes Away

Real contrarian investing starts with your behavior, not your stock picks. Your brain is wired to keep you consuming instead of accumulating, spending instead of owning. The contrarian edge comes from recognizing this programming and acting against it systematically.

• Pay yourself first, literally — invest before you pay bills, not after

• Question every monthly payment that doesn’t build equity in your name

• Convert emergency funds into income-producing assets, not savings accounts

• Ask “What should I buy?” instead of “What should I do?” for every financial decision

• Recognize fear as information, not instruction — when investing feels scary, that’s often the signal

• Focus on buying demand, not picking winners — own pieces of systems people can’t stop using

The crowd will always choose safety over growth, consumption over capital, and wages over equity. That’s not a bug in human psychology — it’s a feature you can exploit. The real contrarian move is becoming the kind of person who builds wealth while others build other people’s wealth.

🎬 Prefer watching? Check out the video version on YouTube: