Marcus — 29, marketing coordinator in Denver — stared at his checking account balance on a Tuesday morning in March. $47.83. Rent was due in six days.

His buddy Jake had just texted him about Tesla hitting $300. “Should’ve bought when I told you at $180, man. Easy money.” Marcus felt that familiar punch in the gut. Another missed opportunity. Another reminder that he was always too broke to invest when the smart money was moving.

Here’s what Marcus didn’t know: He was thinking about wealth building completely backwards. And so was Jake.

The crowd — including most financial advisors — tells you to invest your “extra” money. Build an emergency fund first. Pay off debt. Then, when you’re comfortable, start buying assets.

This is precisely why 97% of people never own capital that pays them back.

I Learned This the Expensive Way

I was 26 when I figured out I’d been asking the wrong question my entire adult life. I kept asking, “How do I make more money?” when I should have been asking, “What should I buy?”

Look, I get it. When you’re living paycheck to paycheck, buying stocks feels insane. I remember sitting in my studio apartment — rent was $1,200, I was making $3,400 after taxes — calculating whether I could afford a $50 investment. The math felt impossible.

But then I noticed something that changed everything.

Every month, I sent money to capital owners before I even saw my paycheck. My landlord got $1,200. Netflix got $15. Spotify got $10. My car payment was $340. Insurance, phone, groceries, coffee — I was sending cash to someone else’s capital 30+ times per month.

I was funding everyone else’s wealth while staying broke myself.

That’s when I realized: The crowd has it backwards. They wait until they’re financially comfortable to start buying assets. But capital owners? They buy assets first, then figure out how to pay the bills.

Why Your Broke Friends Will Stay Broke

Think about Marcus again. His instinct — the crowd’s instinct — is to wait. “I’ll start investing when I have my emergency fund. When I pay off my credit cards. When I get that promotion.”

This is exactly the thinking that keeps people poor forever.

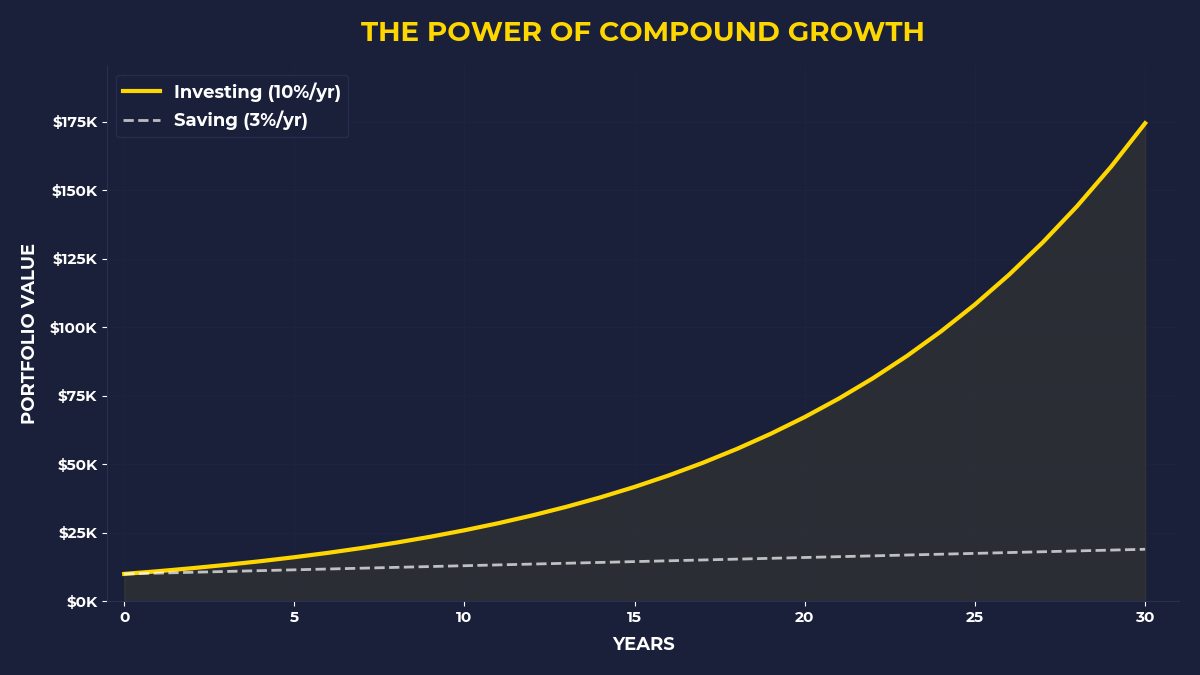

Warren Buffett started buying assets when he was 11 years old, selling golf balls he found in ponds for 6 cents each. He didn’t wait until he had a stable income or a safety net. He saw demand, bought the supply, and immediately started compound interest working in his favor.

The crowd waits for permission to build wealth. Contrarians take action when it’s uncomfortable.

Here’s what I mean by contrarian investing: It’s not buying when stocks are down (though that’s part of it). It’s buying when YOU are down — financially speaking. When every fiber of your conventional wisdom says “you can’t afford this.”

Because here’s the brutal truth: If you only invest your “extra” money, you’ll never have capital that matters.

The $50 Experiment That Broke My Brain

Let me tell you about the month I decided to test this contrarian approach. It was February 2019. I had about $200 in checking after paying all my bills.

Instead of saving that $200 for “emergencies,” I bought $150 worth of Apple stock. Left myself with $50 for the month.

Wild, right?

I ate ramen for three weeks. I walked to work instead of taking Uber. I cancelled a dinner with friends. I was genuinely uncomfortable.

But something interesting happened. Having only $50 forced me to find ways to make more money that month. I picked up a freelance writing gig. I sold some old furniture. I dog-sat for a neighbor. By the end of February, I’d actually made more money than usual — because I HAD to.

The crowd would call this financially irresponsible. I call it the difference between staying poor and building capital.

Why Everyone Gets Your Money Before You Do

Here’s a thought experiment. Look at your bank statement from last month. Count how many times money left your account and went to someone who owns capital.

Your rent or mortgage payment? Goes to someone who owns real estate.

Your Netflix subscription? Goes to shareholders of Netflix.

Your coffee runs, grocery bills, gas purchases? All flowing to people who own the companies that provide these things.

The average person sends cash to capital owners 40-50 times per month. Before keeping any meaningful amount for themselves.

Now count how many times you bought assets that will pay YOU back.

For most people, that number is zero.

What Real Contrarian Investing Actually Looks Like

Forget everything you’ve heard about contrarian investing being some complex strategy about market timing. Real contrarian investing is simpler and more uncomfortable than that.

It means buying assets BEFORE you feel ready. Before you have an emergency fund. Before you’ve paid off all your debt. Before it feels safe.

Robert Kiyosaki — love him or hate him — tells a story about living in a friend’s garage after his business failed. He was getting bills he couldn’t pay, pressure from creditors, the whole disaster. What did he do? He took every dollar that came in and invested it first. Then figured out how to pay the bills.

The crowd would call this insane. But this is exactly how you switch from being someone who pays capital owners to being someone who gets paid by capital.

Here’s the psychological shift: Instead of “I can’t afford to invest,” start thinking “I can’t afford NOT to invest.”

Because every month you wait is another month sending your paycheck to people who already own assets.

The One Question That Separates Builders From Renters

Are you someone who’s tired of watching your money disappear into other people’s capital every month? Someone who’s ready to stop asking permission to build wealth?

Then you need to start asking the question that separates the crowd from the contrarians: “What should I buy this month?”

Not “What should I do to make more money.” Not “How can I save more.” What should I buy?

Because wealth isn’t built by working harder or saving more aggressively. It’s built by owning things that other people pay to use.

The crowd saves first, then invests their leftover comfort money. Contrarians invest first, then figure out how to cover the bills with everything else.

It’s uncomfortable. It’s counterintuitive. It goes against every piece of conventional financial wisdom you’ve ever heard.

And it’s exactly why it works.

The One Thing To Remember

Building wealth isn’t about having extra money to invest. It’s about buying assets before you feel ready, then forcing yourself to solve the cash flow problem. The crowd waits for permission to build wealth and stays broke forever. Contrarians buy assets when they’re uncomfortable and let compound interest solve their problems over time. Every month you wait is another month paying rent on someone else’s capital instead of collecting rent on your own.

Before paying any bill this month, buy $50 worth of an index fund — even if it means scrambling to cover expenses

Count how many times you paid capital owners last month vs. how many times you bought assets (the ratio will shock you)

Ask “What should I buy?” instead of “What should I do?” — this single question shift separates builders from renters

🎬 Prefer watching? Check out the video version on YouTube: