Sarah — 28, marketing coordinator in Denver — earned $67,000 last year and saved exactly $1,200. She read three investing books, listened to four finance podcasts, and spent weekends researching the “best” index funds. She knew her expense ratios, understood dollar-cost averaging, and could explain compound interest to anyone who’d listen.

She also lived paycheck to paycheck.

Every month, Sarah would get paid on the 15th. By the 18th, her rent check cleared. By the 22nd, her car payment, insurance, utilities, and credit cards had taken their cuts. What remained went to groceries, gas, and the occasional dinner out. If anything was left — maybe $100 on a good month — she’d move it to her high-yield savings account and feel responsible.

I Used To Think Like Sarah

I know exactly how Sarah felt because I was there too. At 29, I had what everyone would call a “solid investment philosophy.” I believed in low fees, broad diversification, and time in the market. I had spreadsheets tracking my asset allocation and rebalancing schedules.

I also had $3,400 in my investment account after two years of “consistent” investing.

Here’s what I didn’t understand then: **My investment philosophy was actually someone else’s wealth plan.** Every month, I was sending my paycheck to capital owners — my landlord, Toyota Motor Credit, Xcel Energy, Whole Foods — and then investing whatever scraps remained. I was paying everyone else first, then trying to build wealth with the leftovers.

The breakthrough came when my friend Marcus — 31, software engineer — told me something that sounded completely backwards. “I invest before I pay my bills,” he said. “Even if it means scrambling to cover rent.”

That seemed insane. Wasn’t that exactly what responsible people don’t do?

The Question That Changes Everything

Marcus explained it this way: “Most people ask ‘What should I do to get rich?’ But rich people ask ‘What should I buy to get rich?'” The difference, he said, wasn’t just semantic. It was the difference between working harder and owning more.

Think about Warren Buffett picking up golf balls as a kid. He didn’t just work harder to find more golf balls. He hired other kids to find them while he focused on the buying and selling system. When demand for clean golf balls existed, Warren captured that demand by owning the supply chain.

Or consider the story of Harry Larson, who saw people using a coin-operated scale at a drugstore in the 1930s. Instead of asking “How can I work harder?” he asked “What can I buy?” He bought three scales, then used the cash flow from those scales to buy 70 more scales. Harry wasn’t working 70 times harder — he was owning 70 times more demand.

Here’s the thing most people miss about investment philosophy: **Capital isn’t money sitting in your bank account. Capital is stored demand.** When people need what you own, you have capital.

Why Your Bills Reveal Your Real Investment Philosophy

Want to see your actual investment philosophy in action? Look at your last three months of expenses.

Your rent check goes to someone who owns real estate equity. Your car payment goes to someone who owns automotive financing equity. Your grocery bill goes to someone who owns food distribution equity. Your Netflix subscription goes to someone who owns media content equity. Even your morning coffee — $4.50 at Starbucks — flows to someone who owns coffee retail equity.

Every day, you’re sending cash to capital owners.

Your “investment philosophy” might say you believe in index funds and dollar-cost averaging. But your actual behavior says you believe in making other people rich first, then hoping there’s enough left over to make yourself rich later.

This is backwards.

The Capital Owner’s Approach

I started changing my approach in small ways. Instead of paying all my bills first, I began moving money to investments immediately after my paycheck cleared. Not the maximum I could afford — just $200 the first month.

Then I had to scramble to pay rent.

It was uncomfortable. It was stressful. It was also the first time in my adult life that I prioritized building capital over satisfying capital owners’ demands.

Something interesting happened. When I knew I had to cover that $200 investment plus all my regular expenses, I found ways to earn extra money. I took on freelance projects. I sold stuff I didn’t need. I became more creative about generating income because I’d committed to capital ownership first.

Within six months, that discomfort had pushed my monthly investment up to $800. Within a year, I was regularly investing $1,200 per month — more than Sarah’s entire annual savings — while earning roughly the same income.

The difference wasn’t my investment philosophy about which funds to buy. The difference was my capital ownership philosophy about when to buy them.

What Demand Are You Missing?

Here’s what Sarah didn’t understand about building wealth: **The goal isn’t to work harder for money. The goal is to own pieces of systems where other people’s work creates cash flow for you.**

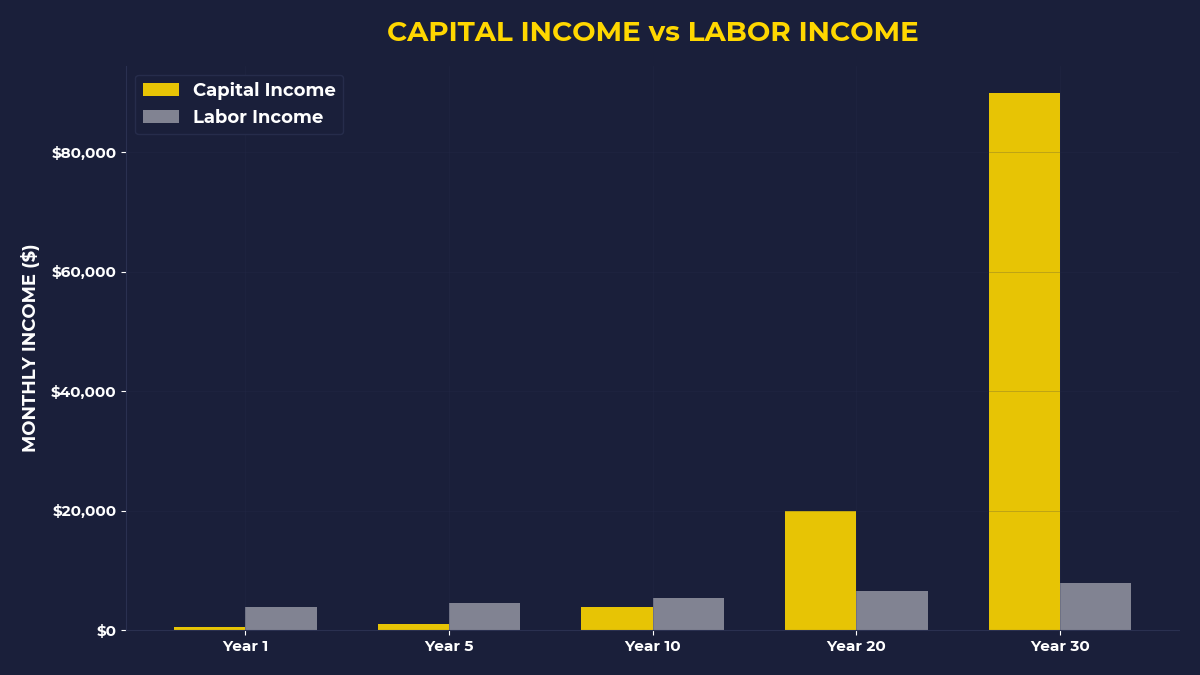

When you buy shares of Apple, thousands of Apple employees work to make that stock more valuable. When you buy a rental property, your tenant’s work pays your mortgage. When you buy an S&P 500 index fund, you’re owning tiny pieces of 500 companies where millions of people work to generate profits that flow to you.

This is leverage. Not the scary kind with borrowed money — the powerful kind where your capital works while you sleep.

But here’s the part most people miss: you can only access this leverage by prioritizing capital ownership over capital owners’ demands.

The Uncomfortable Truth About Emergency Funds

Most financial advice tells you to save three to six months of expenses before investing. This sounds responsible, but it’s actually training you to stay poor.

Let me be honest: I kept a $15,000 emergency fund for three years while my investment account barely grew. That $15,000 earned me about $150 per year in a high-yield savings account. If I’d invested that same money in an S&P 500 index fund during those three years, it would have grown to roughly $28,000.

I prioritized feeling safe over building capital. Meanwhile, capital owners were getting richer off my monthly bill payments.

Here’s a better approach: Keep a small emergency buffer — maybe $2,000 — and put everything else into equity ownership. If a real emergency happens, you can sell investments. Yes, you might sell at a loss sometimes. But you’ll also capture years of compound growth that your “safe” emergency fund never could have generated.

The One Thing To Remember

**Your investment philosophy isn’t about which assets to buy — it’s about who gets your money first.** Capital owners have trained you to pay them first, then invest whatever’s left over. This system keeps them rich and keeps you scrambling. The moment you flip this priority — putting capital ownership before capital owners’ demands — everything changes. You stop being someone who sends cash to equity owners and start becoming someone who receives cash from equity ownership.

Here’s what to do this month:

- Move money to investments the same day you get paid, before paying any bills. Start with whatever makes you slightly uncomfortable — maybe $100, maybe $500.

- List your top five monthly expenses and research owning equity in those companies or sectors instead of just being their customer.

- Replace the question “How can I afford this investment?” with “How can I afford not to own this demand?”

🎬 Prefer watching? Check out the video version on YouTube:

👉 https://www.youtube.com/@PrimalContrarian

Subscribe for daily insights on capital, wealth, and contrarian thinking.