Your Ancestors Never Had to Choose Between NVIDIA and Treasury Bills

Your brain evolved to survive on the African savanna 200,000 years ago. It’s optimized for avoiding lions, hoarding berries, and following the tribe to safety. Every financial decision you make today gets filtered through that ancient operating system.

This is why 89% of retail investors underperformed the S&P 500 between 1999 and 2018, according to DALBAR’s annual study. Their brains were running Stone Age code in Silicon Valley markets.

I learned this the hard way in March 2020. While the market crashed 35% in five weeks, I watched my portfolio bleed red and felt that familiar tightening in my chest. My rational mind knew this was a buying opportunity. My limbic system screamed “DANGER” and begged me to sell everything and hide in cash.

I did exactly what 50 million years of evolution programmed me to do: I panicked.

The Tribe Is Always Wrong About Money

Here’s what nobody tells you about behavioral finance: your brain didn’t evolve to build wealth. It evolved to keep you alive long enough to reproduce. Those are completely different optimization functions.

When food was scarce, hoarding calories made sense. When predators lurked everywhere, following the group meant survival. When winter was coming, loss aversion kept you from gambling away your stored nuts.

These instincts served us well for millennia. Today, they’re financial suicide.

Consider herd behavior — our tendency to follow the crowd. In prehistoric times, if everyone ran in the same direction, you’d better run too. The one guy who stayed behind to “think contrarian” became lunch.

In markets, herd behavior creates bubbles and crashes. It made otherwise rational people bid tulip bulbs to the price of houses in 1637. It drove the NASDAQ up 400% between 1995 and 2000, then down 78% over the next two years. It convinced millions of Americans that housing prices only go up — until they went down 30% between 2006 and 2012.

Your brain still thinks following the crowd is survival. In markets, it’s wealth destruction.

Why Fear Sells Your Best Assets at the Worst Times

Let me tell you about loss aversion — the psychological principle that explains why you’re probably poor.

Studies show humans feel the pain of losing $100 twice as intensely as the pleasure of gaining $100. This made perfect sense when losing your winter food cache meant death. Losing half your berries was catastrophic. Finding extra berries was just nice.

In investing, loss aversion makes you do catastrophically stupid things.

During the 2008 financial crisis, individual investors withdrew $321 billion from equity funds between October 2007 and April 2009. They sold at the bottom. The S&P 500 hit its low of 676 on March 9, 2009, then rallied 69% by year-end.

Those panicked sellers locked in permanent losses to escape temporary pain. Their Stone Age brains couldn’t distinguish between “portfolio down 40%” and “saber-tooth tiger approaching.”

I did this myself in my early investing years. I bought shares of a small biotech company at $34. When it dropped to $28, that 18% loss felt like physical pain. I sold, telling myself I was “preserving capital.”

The stock hit $127 eighteen months later.

My ancient brain had optimized for avoiding immediate danger, not building long-term wealth.

The Recency Bias That Keeps You Poor Forever

Your brain has another bug: it weights recent events far more heavily than distant ones. This is called recency bias.

When the last three mushrooms you ate were poisonous, avoiding mushrooms made sense. When the last three times you wandered from camp you nearly died, staying close to the group was smart.

In markets, recency bias destroys wealth systematically.

After the dot-com crash of 2000-2002, investors fled stocks for “safer” investments. Money poured into real estate and bonds. By 2007, stock allocations in 401(k) plans had dropped to historic lows.

Then stocks returned 10.7% annually for the next decade while bonds returned 2.3%.

The recent pain of the crash convinced millions of investors to avoid the asset class that would have made them wealthy. Their brains couldn’t separate “stocks crashed recently” from “stocks are permanently dangerous.”

Think about it. Your brain gives infinitely more weight to what happened yesterday than what happened over the past century. The S&P 500 has returned an average of 10% annually since 1926, despite multiple wars, depressions, and financial crises. But one bad year makes people swear off stocks forever.

Why Anchoring Bias Makes You Buy High and Sell Low

Want to know why you consistently mistimed the market? Anchoring bias.

Your brain latches onto the first piece of information it receives and uses that as a reference point for all subsequent decisions. In primitive environments, this helped you remember where you found food or water.

In investing, it makes you anchor to irrelevant price points.

If you first heard about Bitcoin when it hit $60,000 in 2021, that becomes your mental anchor. When it crashed to $15,000 in 2022, it felt “cheap” — even though it was still up 1,400% from where it started the previous decade.

I see this constantly. Investors anchor to their purchase price and hold losing positions forever, hoping to “get back to even.” They anchor to recent highs and think every 10% correction is “the big one.”

The market doesn’t care what price you paid. Your ancient brain doesn’t understand this.

The Dopamine Trap That Turns Investing Into Gambling

Here’s where it gets really ugly. Your brain’s reward system evolved to make you seek immediate gratification. Finding fruit gave you an instant dopamine hit. This kept you motivated to keep searching.

Modern investing hijacks this same system.

Day trading, options plays, crypto gambling — they all trigger the same dopamine pathways as slot machines. The intermittent variable rewards create addiction-level responses. Your brain mistakes the excitement of potential gains for actual investing skill.

A study by Barber and Odean found that the most active day traders — the ones getting the biggest dopamine hits — underperformed the market by 6.5% annually after transaction costs. They were paying for the privilege of entertainment while destroying their wealth.

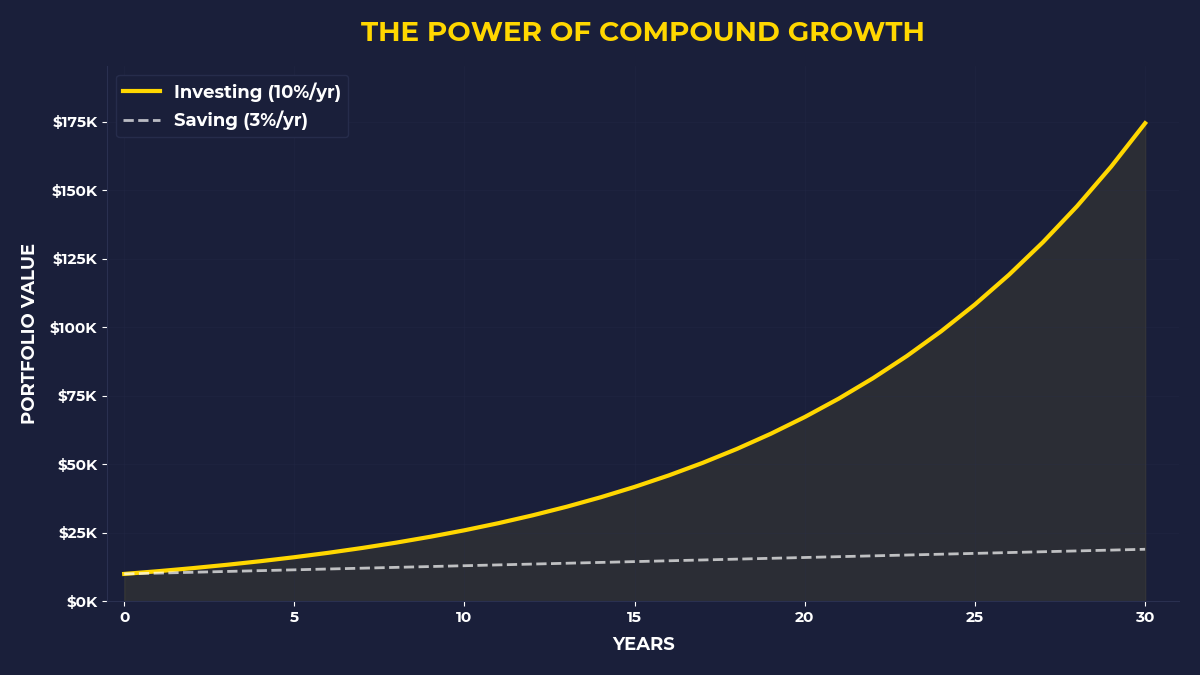

The investors who did best? The ones who bought and forgot. The ones who ignored their Stone Age programming and let compound returns do the work.

What The Primal Investor Takes Away

Your brain is not your friend when it comes to money. It’s running 50,000-year-old code in 21st-century markets. Here’s how to debug the system:

Automate your investing — Remove your brain from routine decisions. Set up automatic transfers to index funds so you can’t panic-sell or procrastinate-buy.

Write down your investment thesis — Before buying anything, document exactly why you’re investing and what would make you sell. Your future panicked self will thank you for the reminder.

Embrace boring — If your investments are exciting, you’re probably gambling. Wealth comes from owning boring, cash-generating assets for long periods.

Study market history — Your brain weights recent events too heavily. Counter this by obsessing over long-term data. Crashes feel permanent; they’re actually temporary.

Expect to feel wrong — Contrarian investing means your Stone Age brain will scream danger when you’re doing the right thing. Discomfort is the price of outperformance.

The best investors aren’t the smartest or most disciplined. They’re the ones who understand their own programming and build systems to work around it. Your brain evolved to keep you alive, not make you rich.

The sooner you accept this, the sooner you can start building actual wealth.

🎬 Prefer watching? Check out the video version on YouTube: